ASX Growth Stocks With High Insider Ownership To Watch

As the Australian market navigates a cautious start to 2026, with the ASX hovering just above the 8,700 level and mixed sector performances, investors are closely watching global events such as America's actions in Venezuela for potential impacts. In this environment of uncertainty and selective gains across sectors like materials, identifying growth companies with high insider ownership can be a strategic move, as these stocks often benefit from aligned interests between management and shareholders.

Top 10 Growth Companies With High Insider Ownership In Australia

| Name | Insider Ownership | Earnings Growth |

| Wisr (ASX:WZR) | 10.2% | 96.3% |

| Titomic (ASX:TTT) | 15% | 74.9% |

| Sea Forest (ASX:SEA) | 15.1% | 92.6% |

| Polymetals Resources (ASX:POL) | 32.9% | 108% |

| Pointerra (ASX:3DP) | 19.8% | 110.3% |

| Newfield Resources (ASX:NWF) | 31.5% | 72.1% |

| Lunnon Metals (ASX:LM8) | 11% | 31.4% |

| Echo IQ (ASX:EIQ) | 19% | 51.4% |

| BlinkLab (ASX:BB1) | 32.1% | 101.4% |

| Adveritas (ASX:AV1) | 18.4% | 96.8% |

We'll examine a selection from our screener results.

Alpha HPA (ASX:A4N)

Simply Wall St Growth Rating: ★★★★★★

Overview: Alpha HPA Limited is a specialty materials and technology company engaged in the delivery and operation of the HPA First and Alpha Sapphire projects in Queensland, with a market cap of A$884.49 million.

Operations: The company's revenue is derived from the HPA First Project, contributing A$0.26 million, and the Alpha Sapphire Project, which adds A$0.06 million.

Insider Ownership: 10.5%

Earnings Growth Forecast: 103.1% p.a.

Alpha HPA is poised for significant growth, with earnings projected to increase over 100% annually and revenue expected to grow nearly 98% per year, outpacing the broader Australian market. Despite generating less than A$318K in revenue currently, it is forecasted to become profitable within three years. The company's Return on Equity is anticipated to be very high at 44.3%. Trading significantly below its estimated fair value suggests potential undervaluation.

- Click here and access our complete growth analysis report to understand the dynamics of Alpha HPA.

- The valuation report we've compiled suggests that Alpha HPA's current price could be inflated.

Artrya (ASX:AYA)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Artrya Limited is a medical technology company focused on developing and commercializing an artificial intelligence platform for detecting, diagnosing, and addressing coronary artery disease in Australia, with a market cap of A$792.00 million.

Operations: The company's revenue segment includes A$0.03 million from the development of AI-driven CCTA image analysis technology.

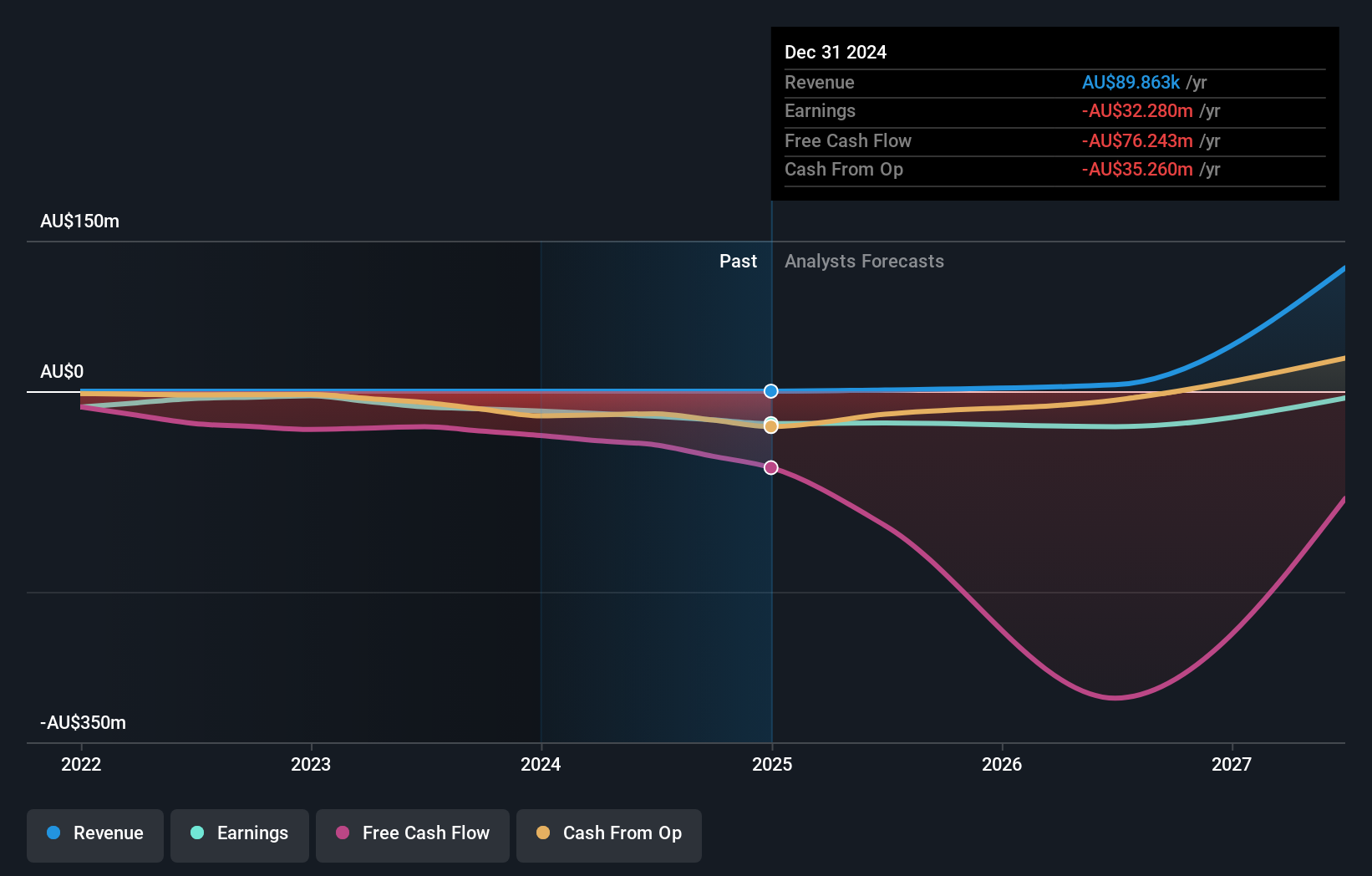

Insider Ownership: 13.4%

Earnings Growth Forecast: 61.3% p.a.

Artrya's revenue is projected to grow at 50.5% annually, significantly outpacing the Australian market's 6.1% growth rate, with earnings expected to increase by 61.25% per year, leading to profitability within three years. Despite generating less than A$28K in revenue currently and experiencing substantial shareholder dilution last year, there has been no significant insider trading activity recently. The company actively engages in industry forums, highlighting its strategic focus on expansion and innovation.

- Get an in-depth perspective on Artrya's performance by reading our analyst estimates report here.

- Our comprehensive valuation report raises the possibility that Artrya is priced higher than what may be justified by its financials.

Develop Global (ASX:DVP)

Simply Wall St Growth Rating: ★★★★★☆

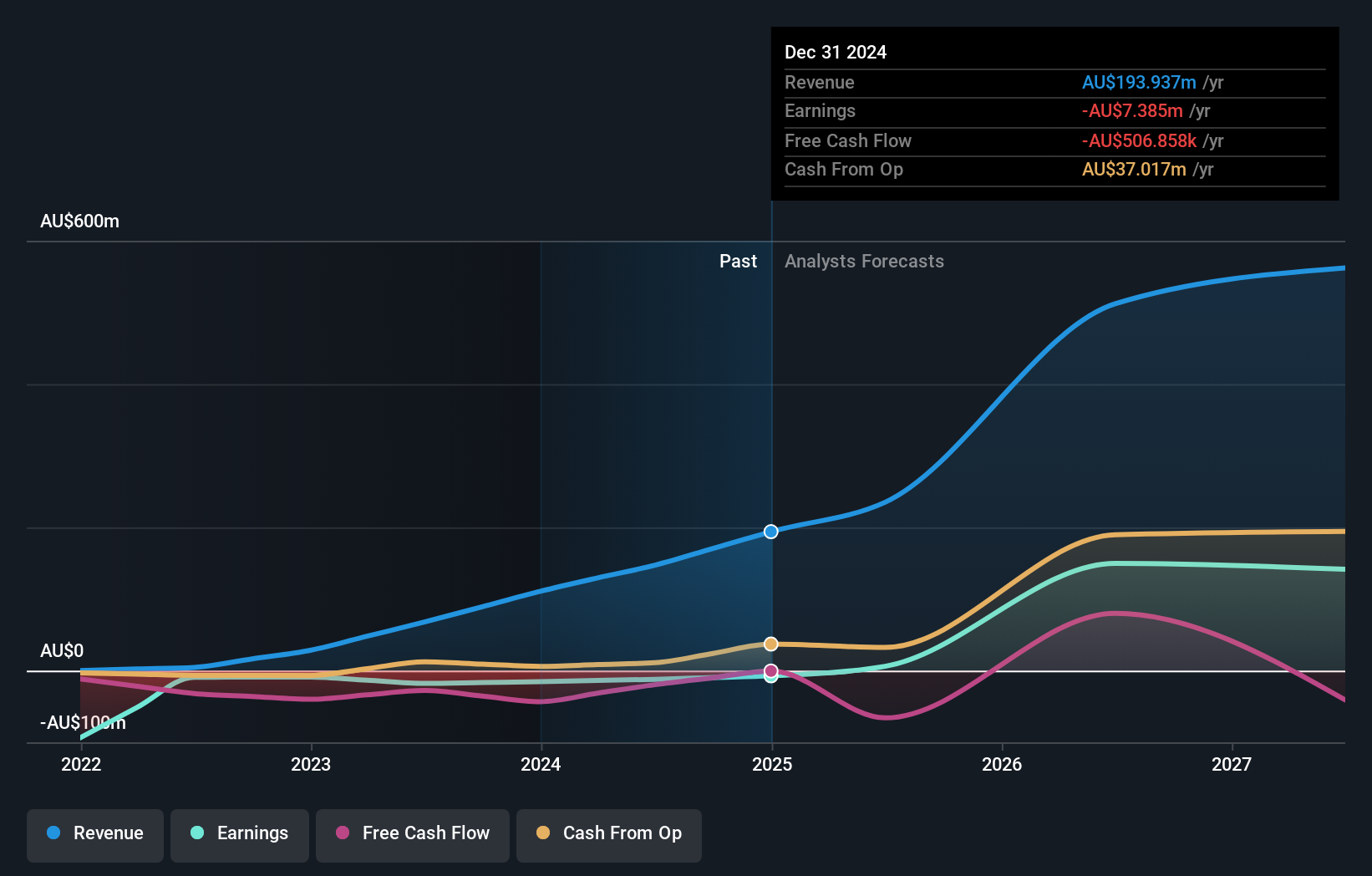

Overview: Develop Global Limited, with a market cap of A$1.55 billion, is involved in the exploration and development of mineral resource properties in Australia.

Operations: Revenue segments for Develop Global include Mining Services generating A$240.65 million and Mining and Exploration contributing A$14.63 million.

Insider Ownership: 20.2%

Earnings Growth Forecast: 32.8% p.a.

Develop Global's revenue is forecast to grow at 36.3% annually, surpassing the Australian market's 6.1% growth rate, with earnings expected to rise by 32.8% per year. Recent substantial insider buying reflects confidence in its growth trajectory. The company trades significantly below its estimated fair value and has become profitable this year despite past shareholder dilution. Strategic appointments, including Duncan Bradford and Nathan Stoitis, aim to bolster its accelerated growth strategy through extensive industry expertise.

- Take a closer look at Develop Global's potential here in our earnings growth report.

- In light of our recent valuation report, it seems possible that Develop Global is trading behind its estimated value.

Seize The Opportunity

- Click this link to deep-dive into the 108 companies within our Fast Growing ASX Companies With High Insider Ownership screener.

- Looking For Alternative Opportunities? The end of cancer? These 29 emerging AI stocks are developing tech that will allow early idenification of life changing disesaes like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com