Bayer (XTRA:BAYN) Valuation Check As AI Antibody Collaboration With Cradle Gains Attention

Bayer (XTRA:BAYN) has agreed to a three-year collaboration with Cradle to bring generative AI tools into its therapeutic antibody research, aiming to speed up molecule design, refine antibody properties, and streamline clinical development workflows.

See our latest analysis for Bayer.

The collaboration with Cradle comes at a time when Bayer’s share price has a 30 day share price return of 9.98% and a 90 day share price return of 35.99%, while the 1 year total shareholder return of 95.94% contrasts with negative total shareholder returns over three and five years. This suggests recent momentum after a weaker long term journey.

If this kind of AI driven drug research interests you, it could be a good moment to scan other opportunities across healthcare stocks as well.

With the share price up sharply over 90 days but still carrying an intrinsic discount of about 80%, is Bayer quietly trading at a bargain, or is the market already factoring in years of future growth?

Most Popular Narrative: 14.8% Overvalued

Against Bayer's last close at €38.35, the most followed narrative anchors fair value closer to €33 per share, framing the recent share price strength in a different light.

Fair Value Estimate has risen moderately from approximately €29.57 to about €33.42 per share, reflecting a higher intrinsic valuation for Bayer.

Curious how a life science group with modest revenue assumptions, improving margins and a richer future P/E multiple still screens as overvalued here? The full narrative lays out the earnings path, the profit reset and the valuation hurdle Bayer is expected to clear. It joins the dots between slower top line growth and a higher earnings base. If you want to see exactly which future cash flows are doing the heavy lifting in that €33 fair value, the next step is to read the complete story.

Result: Fair Value of €33.42 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there is still plenty that could upset this picture, with unresolved glyphosate and PCB litigation as well as pressure on key crop protection and pharma products, both potential setbacks.

Find out about the key risks to this Bayer narrative.

Another View: Multiples Point To Deep Value

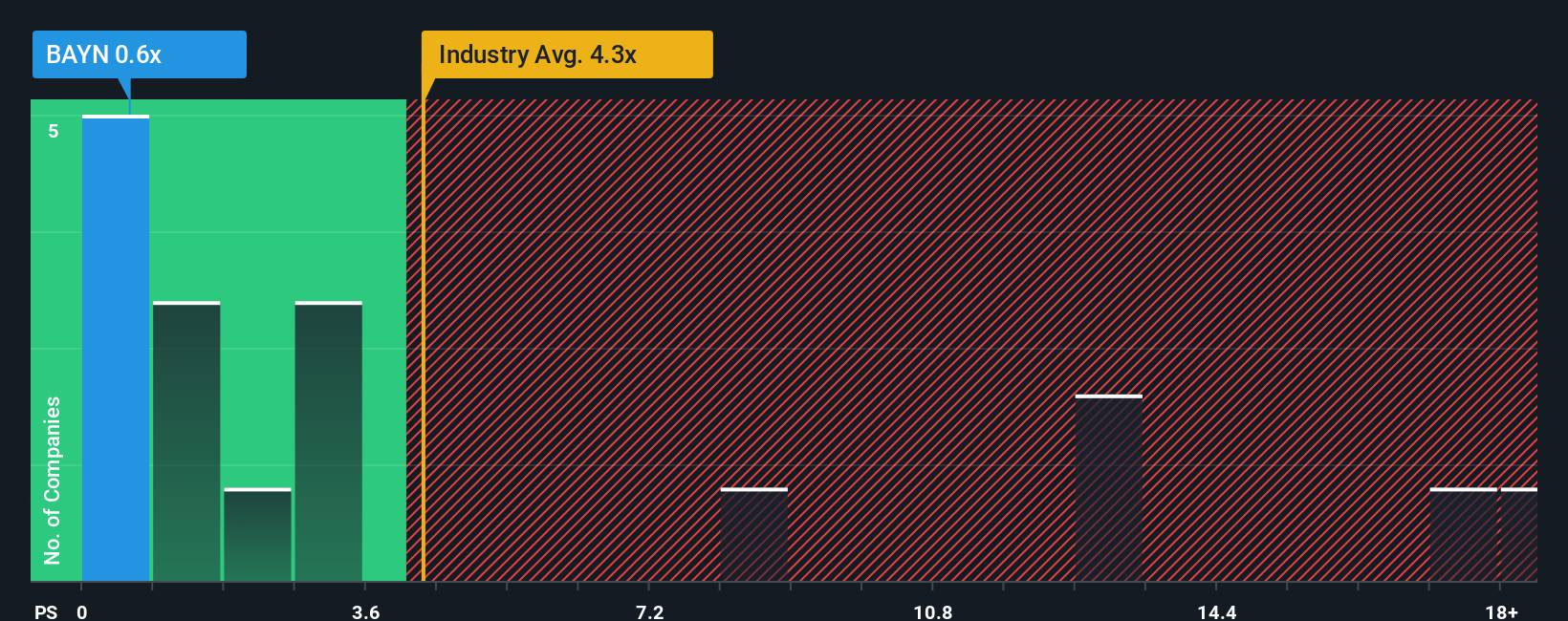

The narrative fair value of about €33 per share paints Bayer as 14.8% overvalued. Yet on simple sales based pricing, the picture flips. Bayer trades on a P/S of 0.8x, while the European pharma group sits around 3.8x and close peers average 2.7x. Our fair ratio for Bayer is 2x, so the current discount is wide even against that more conservative yardstick. For you, the question is whether this pricing gap reflects real business risk or a potential opportunity if sentiment shifts.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Bayer Narrative

If you see the numbers differently or prefer to test your own assumptions, you can build a complete Bayer view yourself in just a few minutes, starting with Do it your way.

A great starting point for your Bayer research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Bayer has caught your attention, do not stop here. The real edge often comes from comparing a few different angles before you commit capital.

- Spot potential turnaround candidates early by scanning these 876 undervalued stocks based on cash flows that may be pricing in more pessimism than their cash flows suggest.

- Follow the next wave of automation by checking out these 26 AI penny stocks that are building real businesses around artificial intelligence, not just headlines.

- Lock in income ideas by reviewing these 11 dividend stocks with yields > 3% that offer yields above 3% and could help balance out more growth focused positions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com