Assessing Zalando (XTRA:ZAL) Valuation As A German Warehouse Closure Reshapes Its Logistics Network

Zalando’s warehouse closure puts its logistics model in focus

Zalando (XTRA:ZAL) has drawn fresh attention after announcing plans to close a warehouse in Germany. The move reshapes part of its logistics network and raises practical questions about costs, delivery reliability, and long term capacity planning.

See our latest analysis for Zalando.

The warehouse closure headline lands against a mixed price history, with a 10.64% 1 month share price return and a 3.69% year to date share price return contrasting with a 17.60% 1 year total shareholder return decline. This suggests recent momentum after a tougher stretch.

If Zalando’s logistics shake up has you rethinking e commerce, it might be a good moment to scan other fast growing stocks with high insider ownership that could be setting up their next move.

With the shares showing recent gains but a 1 year total return decline and trading at a discount to analyst targets and some intrinsic estimates, you have to ask yourself: is there real upside here, or is future growth already priced in?

Most Popular Narrative: 31% Undervalued

Compared with the last close of €25.57, the most followed narrative points to a higher fair value, built on a specific growth and margin story.

The rollout of Zalando's new AI-powered discovery feed and continued investment in personalized, curated shopping experiences are expected to increase user engagement, shopping frequency, and ultimately drive higher average order value and revenue per customer, leveraging broader consumer migration to mobile/online and personalization.

Curious what kind of revenue lift and margin profile justify that gap to fair value? The narrative focuses on faster top line growth and higher profits than today. It also uses a future earnings multiple that is set above the broader specialty retail group. If you want to see how all those pieces add up, the full narrative spells it out.

Result: Fair Value of €36.85 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this depends on European consumers increasing their spending and competitors not forcing steeper discounts. Otherwise, revenue growth and margin ambitions could quickly appear optimistic.

Find out about the key risks to this Zalando narrative.

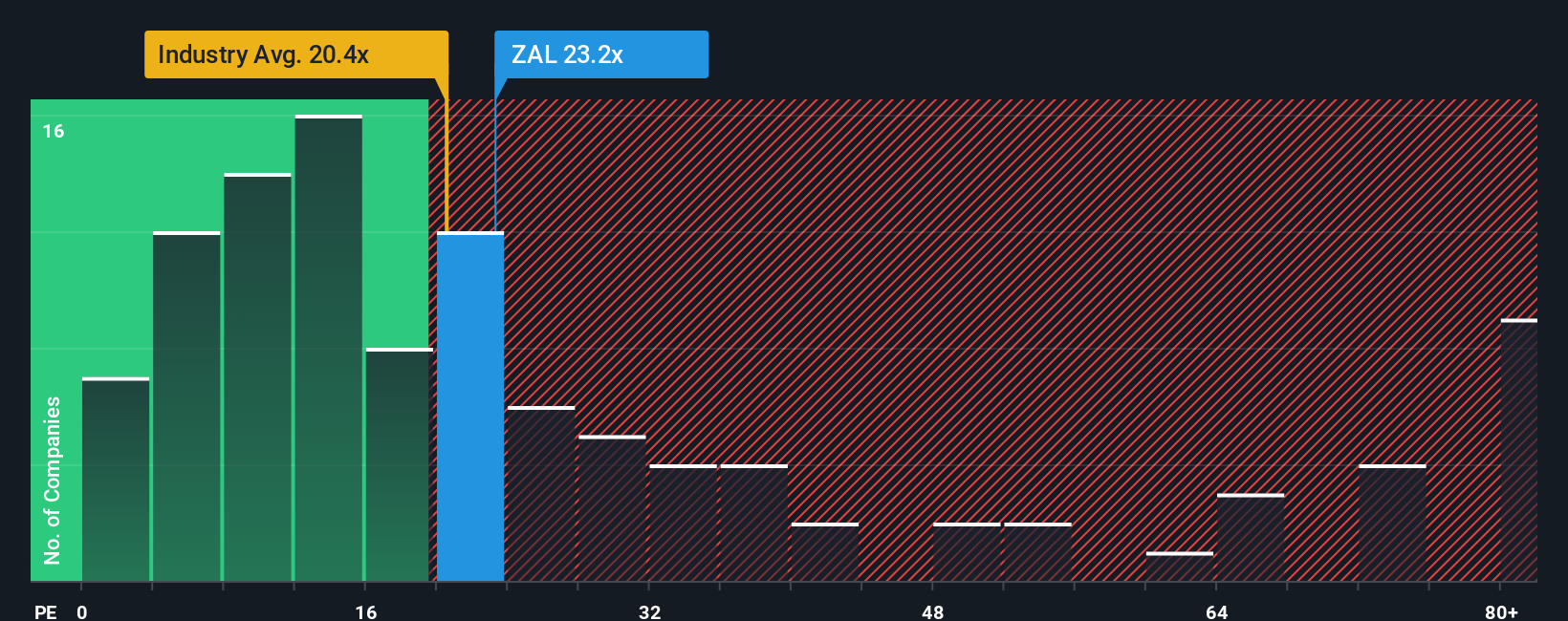

Another View: What The P/E Says

Our DCF model points to strong undervaluation, but the P/E ratio tells a tighter story. At 27.2x earnings, Zalando trades above the European Specialty Retail average of 18.3x and above its own fair ratio estimate of 23.1x. This suggests there is less room for error if growth stumbles.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Zalando Narrative

If parts of this view do not sit right with you, or you prefer to lean on your own assumptions and inputs, you can build a full Zalando story in just a few minutes. To begin, start with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Zalando.

Looking for more investment ideas?

If you are serious about putting fresh ideas on your radar, do not stop at one stock. Use targeted screeners to quickly surface opportunities that actually fit your approach.

- Zero in on potential high reward opportunities by scanning these 3545 penny stocks with strong financials that combine small size with solid financial underpinnings.

- Position yourself early in major technology shifts by reviewing these 26 AI penny stocks shaping how artificial intelligence filters into real world businesses.

- Focus your time on price tags that look more attractive by checking these 884 undervalued stocks based on cash flows using discounted cash flow signals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com