Assessing Costco Wholesale (COST) Valuation As Shares Ease Off Recent Highs

With no single headline event driving attention today, Costco Wholesale (COST) is back in focus as investors weigh its recent share performance against the company’s scale, profitability, and membership warehouse model.

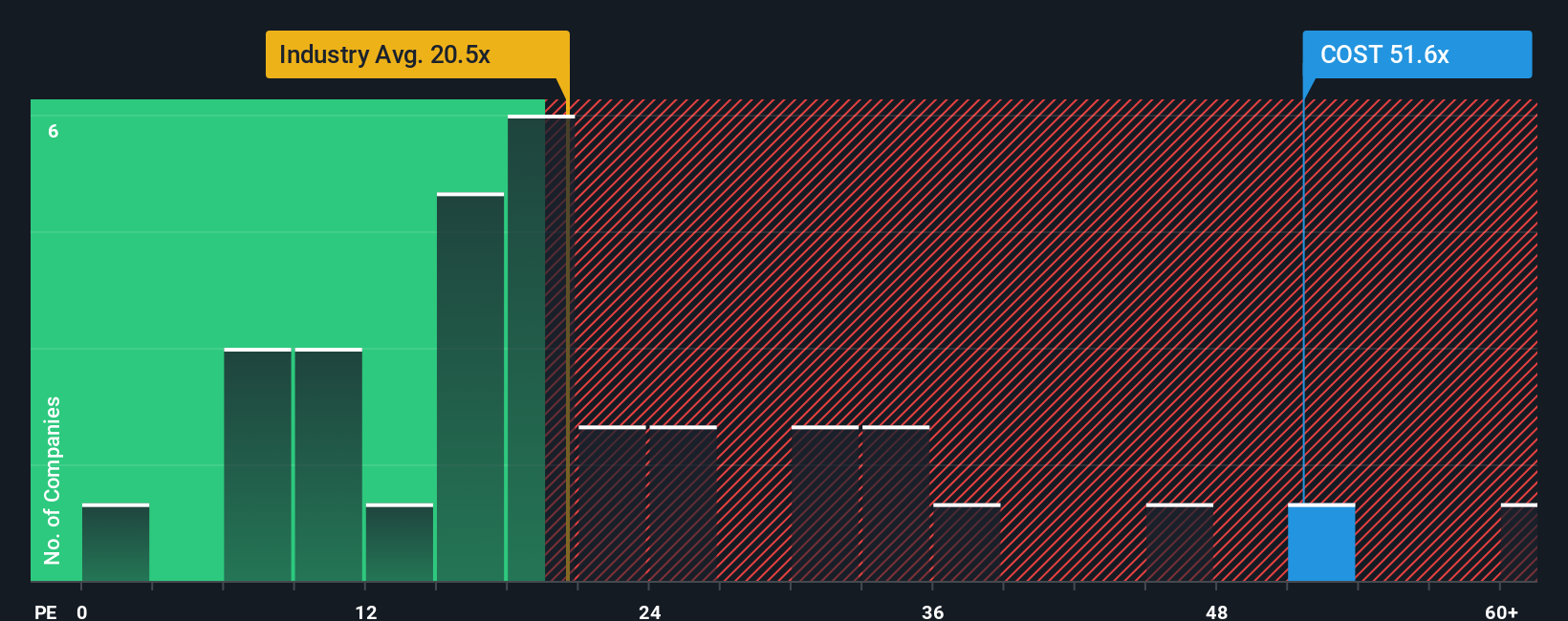

See our latest analysis for Costco Wholesale.

The share price has eased back from recent highs, with a 7 day share price return of 2.35% set against a 90 day share price return decline of 6.40%, while the 5 year total shareholder return of 154.20% points to a very different long term picture.

If Costco’s size and consistency appeal to you, it can also be useful to see what else is on the move by checking out fast growing stocks with high insider ownership.

With the stock easing off recent highs and trading at an intrinsic premium, yet sitting below the average analyst price target, you have to ask yourself: is Costco still a buying opportunity, or is future growth already priced in?

Most Popular Narrative Narrative: 16.4% Undervalued

Costco Wholesale’s most followed narrative sees fair value above the last close of US$882.58, framing today’s premium price as tied closely to future execution.

Analysts are assuming Costco Wholesale's revenue will grow by 7.0% annually over the next 3 years. In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 55.6x on those 2028 earnings, up from 55.4x today.

Want to see what justifies a warehouse retailer carrying a multiple usually reserved for faster growing sectors? The narrative leans on steady expansion, margin uplift, and a richer earnings base. Curious which revenue and profit assumptions have to line up to support that valuation path? The full narrative lays out the step by step financial blueprint behind that view.

Result: Fair Value of $1,055.97 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that blueprint relies on assumptions that could be challenged if higher labor costs squeeze margins or foreign exchange swings unsettle Costco’s sizeable international earnings base.

Find out about the key risks to this Costco Wholesale narrative.

Another Angle on Valuation

That 16.4% undervaluation call sits awkwardly next to what the market is paying today. Costco trades on a P/E of 47.2x, roughly double the US Consumer Retailing average of 23.5x and above a fair ratio of 35.7x, which points to meaningful valuation risk if sentiment cools.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Costco Wholesale Narrative

If you interpret the numbers differently or simply like to test ideas against your own assumptions, you can build a Costco view in minutes with Do it your way.

A great starting point for your Costco Wholesale research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Costco is already on your radar, do not stop there. Broaden your watchlist with fresh ideas that match the kind of opportunities you want to focus on.

- Target potential mispricings by scanning these 882 undervalued stocks based on cash flows that align with your preferred quality, growth, and risk profile.

- Ride powerful technology shifts by checking out these 27 AI penny stocks that tie real business models to artificial intelligence themes.

- Boost your income focus by reviewing these 12 dividend stocks with yields > 3% that combine cash returns with the potential for capital movement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com