Assessing Vita Coco (COCO) Valuation After Strong Multi‑Year Returns And Rich P/E Multiple

Recent performance snapshot

Vita Coco Company (COCO) has drawn fresh attention after a strong past 3 months, with a total return of about 31.9% and a 1 year total return of roughly 35.3%.

That share move sits alongside reported annual revenue of US$609.3 million and net income of US$69.2 million, with both revenue and net income growth figures reported at 10.2% and 20.0% respectively.

See our latest analysis for Vita Coco Company.

Vita Coco’s share price has been choppy in the short term, with a 7 day share price return showing a 2.3% decline and a 30 day share price return showing a 2.1% decline. However, the 90 day share price return of 31.9% and the very large 3 year total shareholder return of just over 3x suggest that momentum has been building over longer horizons from a lower base.

If Vita Coco’s story has caught your eye, this can also be a good moment to broaden your search and check out fast growing stocks with high insider ownership.

With COCO trading around US$52.30 and sitting at roughly a 26% intrinsic discount and a smaller 11% gap to the US$58.00 analyst target, the key question is whether this represents a buying opportunity or whether the market is already pricing in future growth.

Most Popular Narrative: 9.8% Undervalued

At a last close of $52.30 against a narrative fair value of $58.00, the current setup reflects modest undervaluation built on detailed long term forecasts.

Heightened investment in international markets (notably Europe) is resulting in accelerating sales growth and market share gains, with management expecting international revenues to ultimately rival the Americas business. This is expected to significantly impact consolidated revenues and earnings power.

Want to see what kind of revenue mix and margin profile supports that view, and how long it is expected to take? The narrative spells out growth, profitability and valuation assumptions in plain numbers, and shows how they tie back to that $58 fair value target.

Result: Fair Value of $58 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, tariff or freight cost setbacks, along with weaker private label demand, could quickly pressure margins and challenge the assumptions behind that US$58 fair value.

Find out about the key risks to this Vita Coco Company narrative.

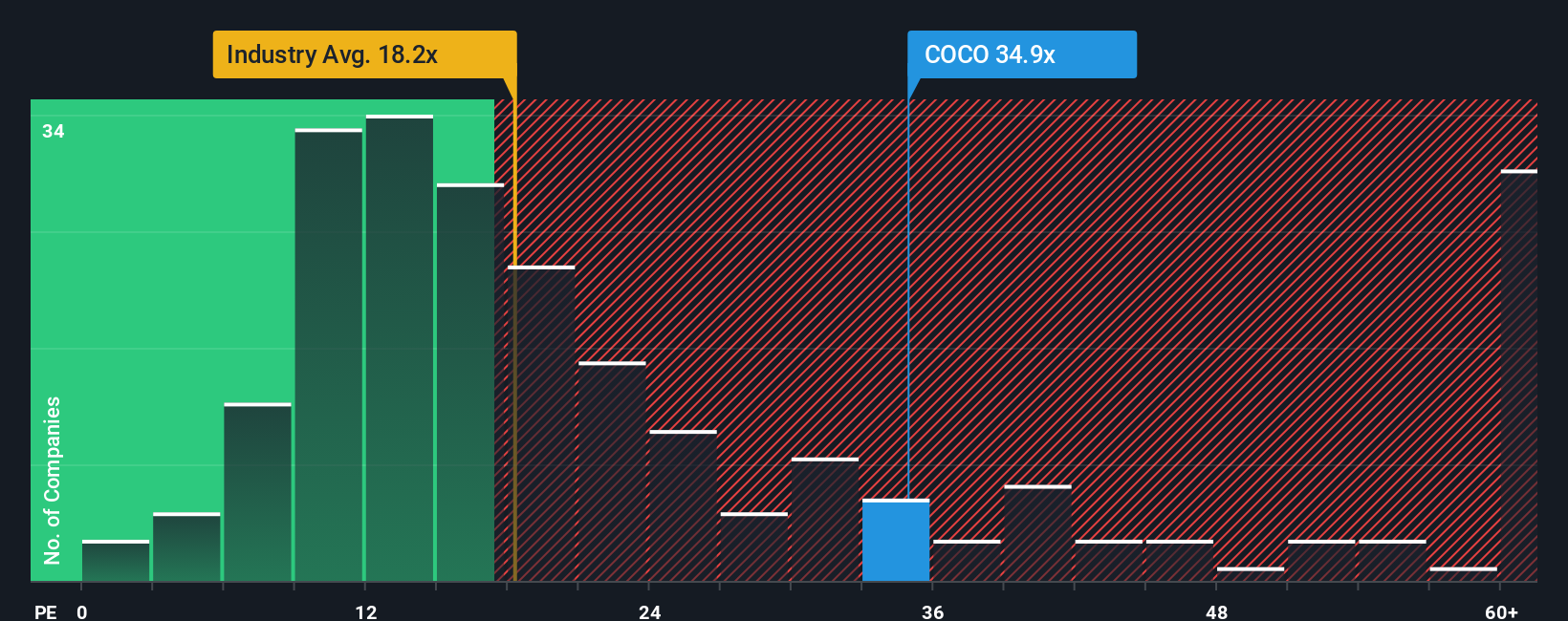

Another View: Rich P/E Puts Pressure On Execution

While the SWS DCF model suggests COCO is trading about 25.7% below an estimated fair value of $70.41, the current P/E of 43.1x tells a different story. That is more than double the 21.1x fair ratio and well above the 17.7x global Beverage average and 19.6x peer average, which points to less room for error if growth or margins disappoint.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Vita Coco Company Narrative

If you see the story differently or simply want to test your own assumptions against the numbers, you can build a custom view in minutes with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Vita Coco Company.

Looking for more investment ideas?

If Vita Coco has sparked your interest, do not stop here. Use this momentum to widen your watchlist and spot other opportunities before the crowd does.

- Target potential mispricing by scanning these 874 undervalued stocks based on cash flows that may be trading below what their cash flows suggest.

- Capture growth themes early by filtering for these 24 AI penny stocks that are tying their business models to artificial intelligence.

- Strengthen your income focus by reviewing these 13 dividend stocks with yields > 3% that offer yields above 3% alongside equity exposure.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com