Digital banks at turning point

MALAYSIA’S digital banking sector entered 2026 with a level of scrutiny it has not faced before. Once hailed as catalysts for financial transformation, the five digital bank licensees find themselves defending their relevance amid leadership reshuffles, measured customer growth and a tightly regulated environment that prioritises prudential safeguards over rapid experimentation.

The departure of several senior executives such as those from AEON Bank, Ryt Bank and KAF Digital Bank in recent months has done more than just raise eyebrows.

The other two digital banks are GXBank and Boost Bank.

The exit of senior leaders reignited a fundamental question: Is Malaysia’s digital banking model structurally capable of delivering the scale, revenue and innovation expected from it?

Interviews with industry executives, consultants and investors suggest the sector is not experiencing a temporary adjustment.

Instead, it is confronting the reality that its early assumptions – market size, customer behaviour, regulatory flexibility and the economics of financial inclusion – were more optimistic than justified.

Ravi Kittane, Malaysia deputy financial services consulting leader and partner at Ernst & Young Consulting Sdn Bhd, says the current stage should also be viewed through the lens of digital-bank maturity curves globally.

He notes that all five Malaysian digital banks were launched within roughly the first 2.5 years after the licence award in April 2022 and are still stabilising their platforms, with the next two years likely to be decisive as they move beyond the foundational phase.

Some critics attribute it to a mismatch between the growth trajectories projected in early business plans and the slower, highly regulated reality that followed.

Some also say that the departures happened due to rising pressure from shareholders who expected faster scaling or clearer milestones on lending, deposits and fee-based income.

That broader shift in expectations is echoed by Ravi, who says the focus needs to move from deposit-led customer acquisition towards sharper differentiation and more disciplined execution, as investors increasingly demand clearer paths to sustainable scale and profitability.

“We are seeing some of this with digital banks launching propositions such as SME deposits and lending, micro-financing and embedded insurance, as they look to capitalise on their early traction and build on their foundation,” says Ravi.

To be fair, management changes are common in new ventures. Singapore, for instance, also saw in 2024 chief executive officers (CEOs) of its GXS Bank and Maribank leaving after leading the digital banks for four to five years.

A consultant who advises several fintech and traditional banks says the sector is “moving into a phase where boards want less experimentation and more predictability”.

Meanwhile, Boost Bank’s former head of product David Tay tells StarBiz 7 that Malaysian digital banks are still in the “startup stage” and are moving towards a more maturing phase.

“It is common to see leaders come and go in startups. Some leaders are brought in to set up the digital banks and handle the regulatory needs. These are their skills.

“As the digital banks grow, then a new set of leaders will come in based on current needs,” he says.

That shift has forced some digital banks to rethink the profiles of leaders they need, including via a pivot toward executives with traditional banking backgrounds.

Take KAF Digital Bank for example. After its CEO Rafiza Ghazali left, Suzaini Mukhtar took on the role. Suzaini was formerly senior vice-president and head of deposit and payment at Bank Simpanan Nasional. He has also held senior roles at HSBC, Standard Chartered Bank and Alliance Bank Malaysia in the past.

Not keeping up with expectations

Malaysia’s digital banks are gaining customers and attracting deposits, but the bigger issue is whether that traction is translating into a sustainable business model fast enough.

The challenge is not just growth, but the quality of growth: strong promo-led deposit gathering early on, but retention and profitable lending conversion are harder.

Lending books are expanding, but not yet at the scale or margin needed to absorb high operating, technology and customer acquisition costs – especially in a market where early growth is also shaped by regulatory limits during the foundational phase.

The economics of serving low-income households, a central goal outlined by Bank Negara Malaysia, has proven more constrained than projected.

Nearly 60% of Malaysian digital banking customers are those with limited access to traditional financial services, such as gig workers, retail users and small business owners.

These segments tend to borrow in small amounts, carry higher risk and often rely on irregular income streams.

Digital banks anticipated that alternative data – such as payment histories, ride-hailing activities or utility patterns – would improve credit scoring. But these models remain unproven at the scale required to build large, stable loan books.

Another key challenge faced by the digital lenders is the small market they operate in, where they have to compete with already established traditional banks.

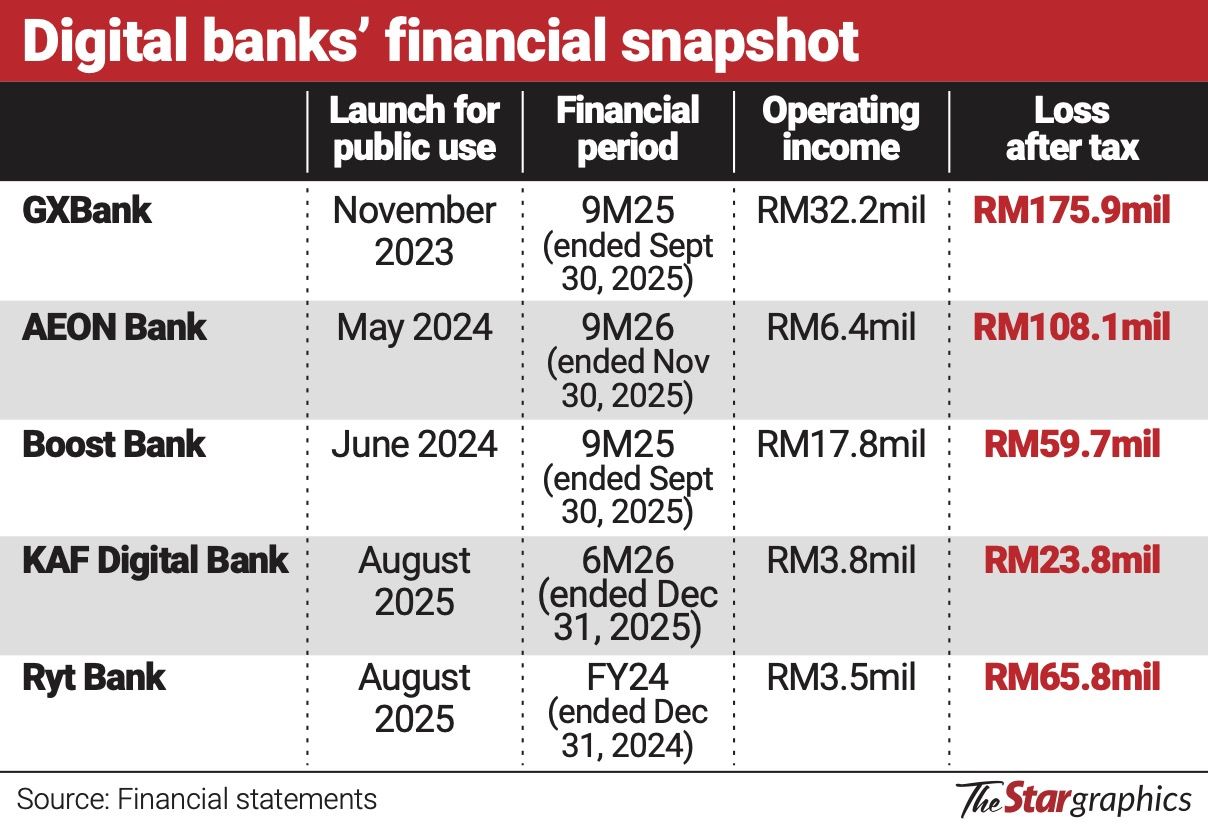

According to the Finance Ministry, as of September 2025, the five digital banks collectively served 1.97 million customers, with RM3.1bil in deposits.

The numbers are truly positive, considering that the first of the five digital banks – GXBank – was only launched for public use in November 2023 and the last – Ryt Bank – was launched in August 2025.

Ravi says this early traction broadly tracks the global maturity curve for digital banks, where many players take several years to reach profitability, with outcomes depending heavily on strategic focus and execution quality rather than launch momentum alone.

“Most digital banks in the world reach profitability in years three to five, with outliers at both ends – OakNorth reported profitability in 11 months, while Revolut took about six years.”

That said, the Malaysian digital lenders are competing in a space where more than 90% of Malaysian adults already hold accounts in traditional banks.

London-based digital bank Revolut, which is widely seen as one of the major digital-banking success stories, has over 65 million customers across over 40 countries. Without room to scale, growth would be largely limited.

Also, in Malaysia, savings behaviour tends to be conservative, with deposits concentrated in institutions with long-standing reputations.

Many Malaysians still doubt the security of saving money in digital banks with no physical operations. While they may transfer some money into their digital accounts, the bulk of cash is still kept with the traditional banks.

GXBank, for example, pays an interest rate of 2% per annum on a daily basis, with no lock-in period.

In contrast, the interest rates typically paid by traditional banks in Malaysia for basic savings accounts are well below 1%.

Another reason behind the hesitation to shift to digital banks is that existing mobile banking applications from incumbents such as Malayan Banking Bhd (Maybank), CIMB Group Holdings Bhd and RHB Bank Bhd already provide stable, reliable services.

Consumer dissatisfaction with traditional banks is lower than in many markets that experienced rapid digital disruption.

Tay says that traditional banks are also keeping up with digital banks in terms of product offerings, making the space more competitive.

“The digital banks are still largely in the deposit-taking stage and building their customer base. As they enter more into lending, you will see more products from the digital banks,” he adds.

In short, digital banks are not entering a market defined by unmet needs. They are attempting to reposition consumers who already have functioning banking relationships – a far more difficult and expensive exercise.

Fintech expert Wong Wai Ken says retail customers are likely experiencing some fatigue from multiple digital-bank launches, with only a smaller group of enthusiastic users actively opening accounts mainly to enjoy promotional rates on cash.

This makes it harder for digital banks to build deep, primary banking relationships at scale early on, according to Wong, who is also StashAway Malaysia’s country manager.

Regulation creates stability — and limits expansion

Malaysia’s regulatory framework has been consistent, transparent and cautious. For the broader financial system, this is largely positive.

But for digital banks, the question is whether the regulatory framework is diluting innovation.

Ravi takes a more calibrated view, arguing that Malaysia’s framework is designed to support the under-served mandate while mitigating system risk.

He notes that it is more permissive in some areas but more prudent in others, particularly the RM3bil asset cap during the foundational phase, which is intended to preserve stability while digital banks build their risk models, technology stacks and governance.

Some fintech advocates argue that regulations designed to prevent excessive risk-taking are inadvertently preventing digital banks from testing the very models that could differentiate them.

Others counter that given the experiences in markets like the United Kingdom, Hong Kong and Singapore – where several digital banks have struggled financially – cautious regulation is not only prudent but necessary.

Bank Negara Malaysia’s position is clear: innovation cannot compromise stability. The question is whether digital banks can thrive under such constraints.

Regulations aside, one of the digital banking sector’s biggest challenges is that traditional banks have not remained static.

Instead, they have accelerated digital adoption, streamlined contactless payment infrastructure, invested in cybersecurity and expanded online credit products.

Maybank continues to strengthen the MAE ecosystem. CIMB is pushing further into digital investment tools. RHB Bank has broadened SME digital onboarding and automation.

Instead of digital banks disrupting incumbents, incumbents have absorbed digital innovations into their existing ecosystems – reducing the differentiation digital banks hoped to claim.

Consumers often see little incentive to switch to a new institution when their current bank app already meets their daily needs.

This leaves digital banks competing for a narrow segment of early adopters or customers seeking rewards rather than long-term banking relationships.

Industry experts point out that product overlap across digital banks is growing, making it harder for any single player to stand out.

Without a clear, distinctive value proposition, the sector risks becoming a collection of near-identical offerings targeting the same group of digitally comfortable consumers.

Wong says digital banks could widen their product suite through partnerships in areas such as wealth management and stockbroking to capture more wallet share and reduce the need for customers to maintain multiple accounts across platforms.

He also says Ryt Bank deserves mention for taking a bolder route with its AI interface, which he views as a novel approach to solving awkward pain points such as bill splitting.

This is not merely an issue of marketing. It is a structural challenge: bold financial innovation often carries risk, and Malaysia’s regulations prohibit products that push those boundaries too far.

As a result, digital banks are trapped in a narrow corridor. They are expected to innovate, but not permitted to take the kinds of risks that typically underpin breakthrough products.

Ravi says the foundational-phase structure may also channel innovation toward lower-risk use cases first, including micro-lending and fee-based propositions suited to under-served segments, before broader balance-sheet expansion is unlocked.

Several digital banks are backed by deep-pocketed shareholders, including conglomerates, regional tech firms and established corporate groups.

Boost Bank is owned by Axiata and RHB Bank. GXBank is backed by Grab Holdings Ltd and Singapore Telecommunications Ltd, along with a consortium of other Malaysian investors, including Kuok Group. Ryt Bank is owned by a consortium led by Sea Ltd and YTL Digital Capital Sdn Bhd.

Where the two Islamic digital banks are concerned, AEON Bank is owned by a consortium of AEON Financial Service Co Ltd, AEON Credit Service (M) Bhd and MoneyLion Inc; and KAF Digital Bank by a consortium led by KAF Investment Bank Sdn Bhd.

But even these investors would tighten expectations as global fintech sentiment becomes more cautious.

The era of funding based on user numbers or app downloads is over. Investors now expect clear revenue generation, manageable burn rates, credible paths to profitability and distinct market positioning.

The digital banks are still loss-making. GXBank, which has a customer base of over one million, recorded a loss after tax of RM176mil for the first nine months of 2025. Its net interest income for the nine months stood at RM32.9mil, against total operating expenses of RM177.4mil.

Of the operating expenses, staff costs represent RM78.2mil and other costs – excluding depreciation and amortisation – were recorded at nearly RM94mil.

Can Malaysia sustain five digital banks?

The issue that industry watchers are increasingly discussing, albeit discreetly, is whether Malaysia can support five digital banks in the long term.

Malaysia’s population, income levels and financial behaviour suggest a market that may support two or three strong digital players.

Consolidation by 2028 is seen by many analysts as a realistic scenario, whether through mergers, acquisitions or strategic partnerships.

Wong says he expects only two to three digital banks to achieve financial sustainability by year five, reinforcing the view that the market may ultimately favour a smaller number of viable players.

Even if consolidation does not occur formally, the sector may split into highly specialised entities that share little overlap in target markets.

Malaysia’s digital banks are not failing. They are stabilising in a more constrained, disciplined and pragmatic form than many had projected.

The ambitious narratives of 2022 have given way to a more sober understanding of the market’s realities.

Still, the sector is not without opportunities. SMEs remain under-served. New forms of alternative credit could eventually prove viable. Embedded finance is gaining traction regionally. And Malaysia’s broader fintech ecosystem is still expanding.

Also, as Tay points out, digital banks have data points that are not available to traditional banks such as e-wallet transaction patterns like frequency of top-ups and spending consistency; gig-platform income or activity data; and eCommerce seller data.

This alternative data offers an edge for the digital lenders in assessing borrowers’ credit capacity.

Digital banks will likely play a meaningful role in Malaysia’s financial future, but not in the sweeping, transformative manner they once promised.

The coming years will test whether they can adapt to these constraints – and whether the Malaysian market can produce a digital banking model that is both commercially viable and aligned with its inclusion goals.

Ravi says the banks that pull ahead will likely be those with clear differentiation and disciplined, tech-first execution, including stronger day-to-day customer engagement, better underwriting and product ecosystems that deepen usage beyond promotional deposits.

For now, the sector stands at a turning point defined not by crisis, but by a necessary recalibration of expectations, strategy and leadership.