Stepping on the gas

A REVERSAL of fortunes seems to be happening to Malaysia’s natural gas industry.

The days of building demand are over. Instead, it’s now about meeting the increasing demand.

In the early days, when Petroliam Nasional Bhd (PETRONAS) and its contracting partners were extracting natural gas, mostly from offshore fields in Malaysian waters, the plan was to make sure there was sufficient demand for those hydrocarbons, both domestically and in the export market.

To support exports, PETRONAS built one of the world’s largest liquified natural gas (LNG) facilities in Bintulu, Sarawak, with output largely sold under long-term contracts to key markets such as Japan, South Korea and Taiwan.

After gas was discovered and produced offshore Terengganu, Petronas built gas processing plants and petrochemical complexes but more importantly, piped the gas onshore for domestic and industrial use.

The Peninsular Gas Utilisation (PGU) system was developed to transport that gas across the peninsula, underpinning industrial growth and expanding the role of gas in the local energy mix.

In essence, the idea was to “create” demand to match rising supply from upstream developments.

Today, that dynamic is beginning to reverse.

Demand is set to accelerate, while supply becomes increasingly constrained and more geographically segmented – anchored in gas-rich Sarawak and Sabah, but with demand growth concentrated in the peninsula.

Two key factors are in play. One, there is a new wave of gas-fired power plant developments, the first in over a decade, driven by rising electricity demand from data centres (DCs) and electrification trends such as electric vehicles.

The Energy Transition and Water Transformation Ministry targets DC electricity demand to reach 20.9GW by 2040, from around 7.7GW by 2030, positioning Malaysia as the largest data centre hub in Asean.

Two, the recent disruptions in global LNG markets, including temporary supply interruptions and force majeure declarations from major exporters such as QatarEnergy, have further underscored the fragility of global gas supply chains.

Qatar is widely regarded as one of the world’s lowest-cost LNG producers but, with heightened market volatility, cost competitiveness alone may no longer be the only consideration in long-term supply planning, say industry observers.

Since the Middle East conflict, LNG prices have moved higher in tandem with crude oil.

“Energy security has become a central concern for many economies, as reliable and competitively priced electricity is a key enabler of economic growth and investment,” says the chief executive officer of a notable Malaysian-based oil and gas firm.

Singapore, for example, relies heavily on imported natural gas for power generation.

The country’s imported gas comprised about 45% piped natural gas (PNG) from Malaysia and Indonesia with the remaining 55% being LNG from the United States, Australia, Europe and Middle East.

Of this, the Middle East accounts for around 40% of LNG imports, meaning regional disruptions could materially affect supply costs despite its diversified LNG sources, analysts say.

In Malaysia, gas is expected to play a larger role in the power generation mix over time as coal capacity, which remains the dominant source of electricity at 59% in 2025, is progressively phased down between 2029 and 2033, with the remaining fleet retiring between 2040 and 2044 under the energy transition agenda.

In 2025, gas accounted for 34% of the generation mix and this is expected to climb toward 50% by 2030.

“For years, the local gas industry focused on growing demand. That has now flipped, with attention shifting to whether supply can keep pace with rising consumption from new gas-fired capacity and DC-driven load growth,” an industry veteran in the gas sector tells StarBiz 7.

He says the country’s power sector remains relatively insulated, supported by a high share of domestic gas supply and a regulated pricing structure.

However, LNG imports are expected to gradually increase as domestic gas fields mature and installed gas-fired power capacity expands, which may expose the power system more to global LNG market dynamics.

Around 85% of Peninsular Malaysia’s gas supply is sourced domestically, including around 5% to 10% from the Malaysia–Thailand Joint Development Area.

The balance is made up of LNG imports, which are regasified through two regasification terminals, namely the Sungai Udang Regasification Terminal (RGTSU) in Melaka and Pengerang Regasification Terminal (RGTP) in Johor, commissioned in 2013 and 2017, respectively.

Together, these facilities, which are operated by PETRONAS’ subsidiary PETRONAS Gas Bhd (PetGas), form the backbone of the LNG import infrastructure.

RGTSU has a throughput capacity of 3.8 million metric tonnes per annum (MTPA), while RGTP adds a further 3.5 million MTPA.

These regasification facilities feed into the PGU pipeline network, together providing a combined supply capacity of about 990 million standard cubic feet per day.

The RGTSU has historically operated at just 10% to 15% utilisation, but PetGas expects this to rise sharply to 65%-70% from 2026.

For LNG imports, Australia accounts for the bulk of inflows in recent years, alongside smaller volumes from Brunei and other suppliers.

However, PETRONAS signed a 20-year LNG supply agreement with QatarEnergy in early February prior to recent geopolitical escalation, with deliveries due to begin in 2028, as part of efforts to further diversify the country’s long-term LNG supply portfolio.

Malaysia’s LNG sourcing diversification also extends to the United States.

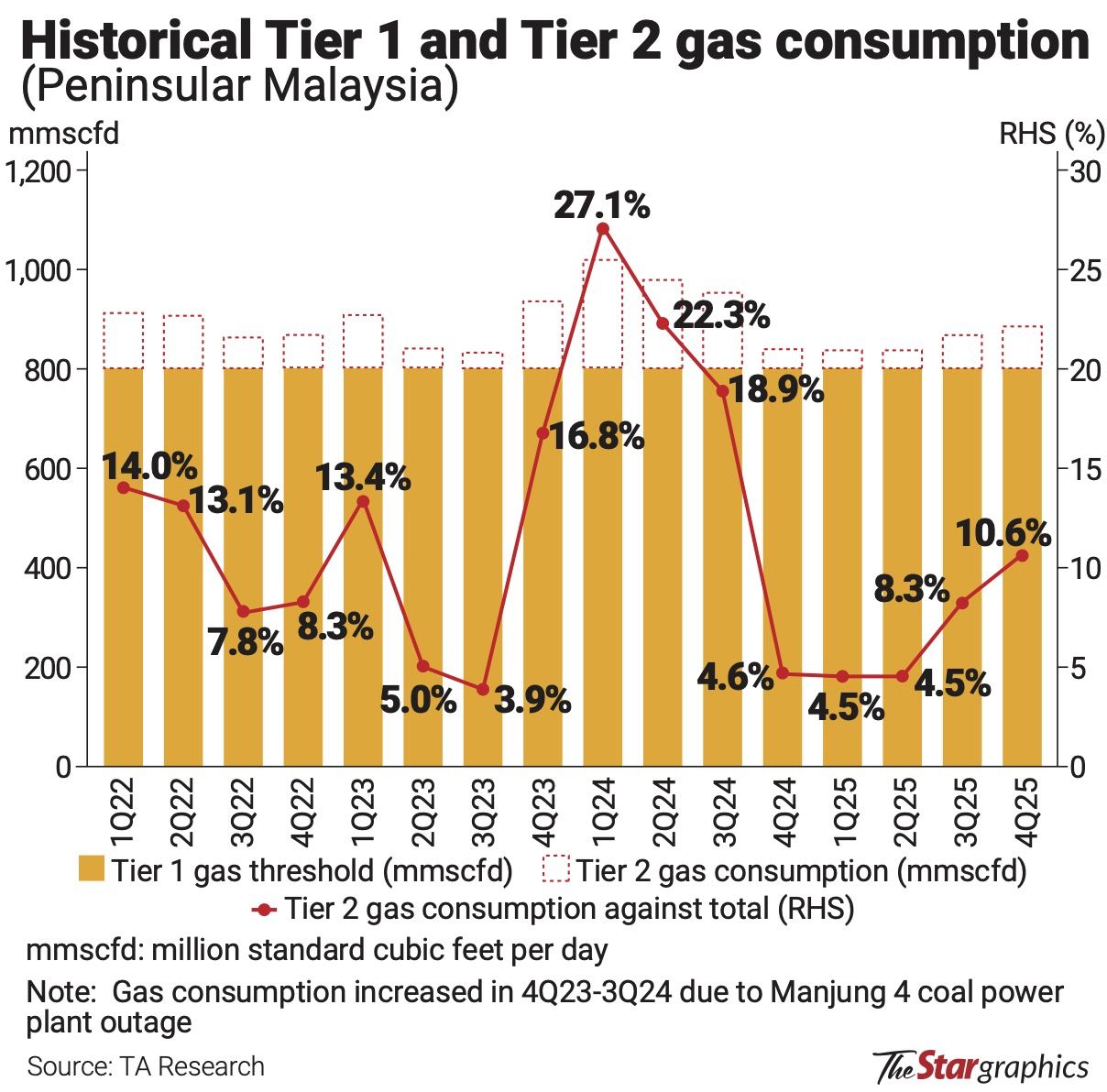

Gas supplied to the power sector follows a tiered pricing structure, with around 90% of volumes subject to a Tier-1 ceiling price of RM35 per MMBtu (a standard energy unit for natural gas pricing), while the remaining is exposed to market-based Tier-2 pricing.

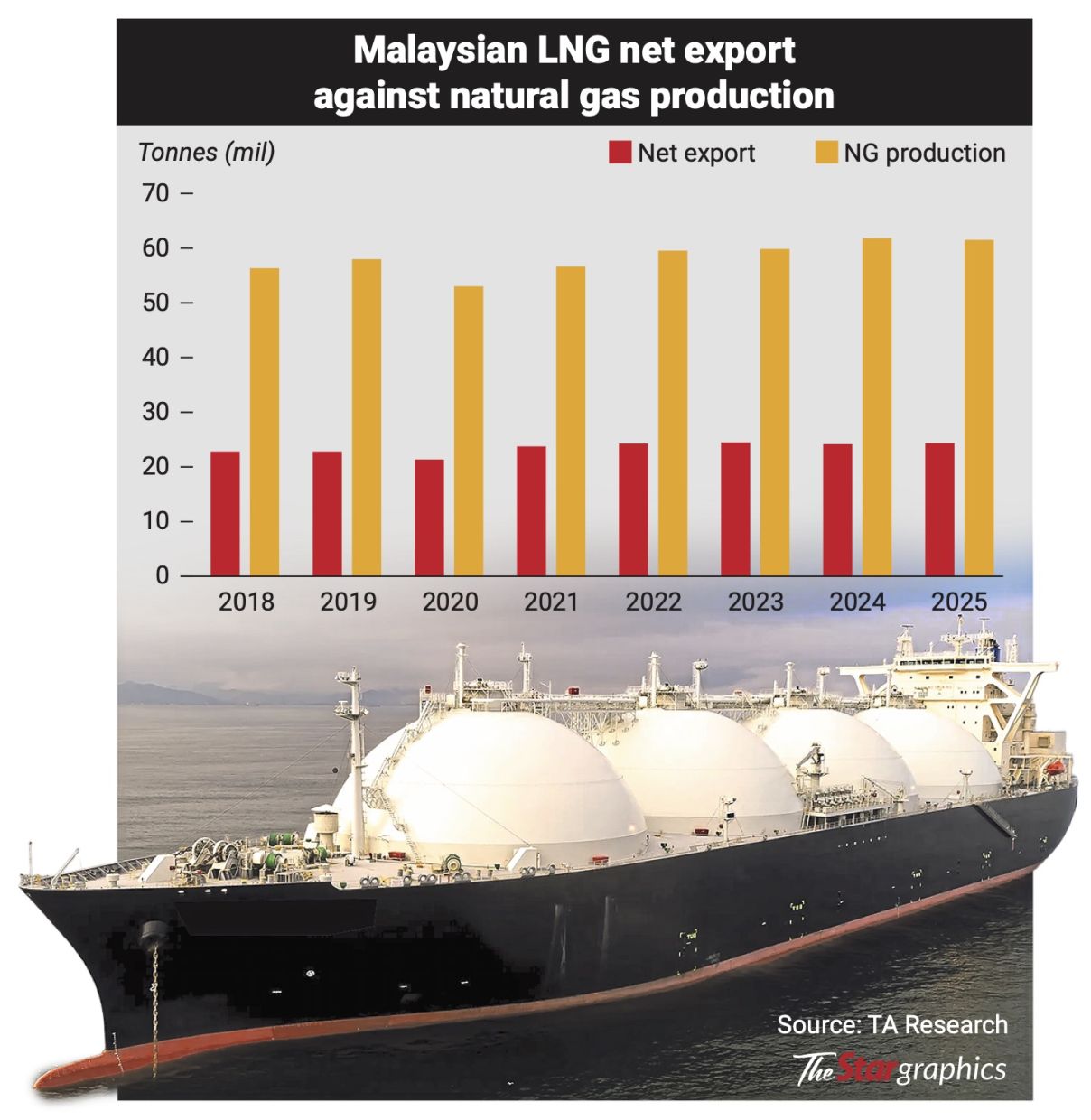

Malaysia is currently a net gas exporter. Global gas price movements also typically take six to seven months to feed through to Malaysian gas prices under the Malaysia Reference Price framework.

In contrast, coal price movements tend to flow through more quickly as coal is fully imported.

Industry players say the LNG import system largely operates on a just-in-time basis, with cargoes delivered directly into regasification terminals before being temporarily stored in ultra-cold temperatures and then converted back into gas for pipeline distribution.

“We need to reassess buffering capacity and storage flexibility in the event of supply shocks, especially as imported gas demand could exceed the combined capacity of existing regasification terminals to receive and process LNG as early as 2029,” the gas industry veteran adds.

With competition to secure essential resources like LNG expected to intensify as disruption of critical infrastructure is likely to take years to rebuild, he believes “the days of cheap gas are over”.

To address potential import needs, two more regasification terminals are being developed.

One will be in Lumut by PetGas, which is expected to have the capacity at least on par with the two existing regasification terminals.

The second, in Yan, Kedah, involves Gas Malaysia Bhd which recently received approval to develop a regasification terminal with capacity of up to six MTPA.

Together, these upcoming regastification terminals signal that beyond securing supply, Malaysia is investing in the infrastructure needed to move that gas to where it is needed, whether to power plants, industrial or commercial users, industry players say.

However, execution risks and timing remain a key concern.

While the space is gradually being opened to new participants like Gas Malaysia, it remains tightly coordinated, with approvals contingent on proven demand, the industry player says.

The last-mile segment of the gas value chain has been gradually opened up, with Gas Malaysia now facing additional competition.

On the whole, developments point to a structural shift in Malaysia’s gas market, from a supply-led system in its early development phase to a more demand-anchored framework.

The upcoming National Gas Roadmap is also likely to offer long-awaited visibility on market liberalisation, pricing structure and long-term demand planning.

Industry observers say these factors will shape the cost, availability and role of gas as Malaysia’s transition baseload fuel.