The energy quagmire

ENERGY security has always been a serious matter. And it just got more serious.

The Middle East conflict has pushed the matter into the limelight and made it a top priority for governments, including Malaysia.

One issue is natural gas. While Malaysia is a net exporter of liquefied natural gas (LNG) mostly from Bintulu’s world class LNG facilities, it is also in need of more gas today as the country is in the midst of a significant increase in power plants. (Its sale of LNG has long-term contracts with foreign buyers such as Japan that are limiting its ability to redirect supply for domestic use).

But can Malaysia find this additional LNG that it needs in time? With Qatar’s supply in jeopardy, it is becoming an increasingly challenging task.

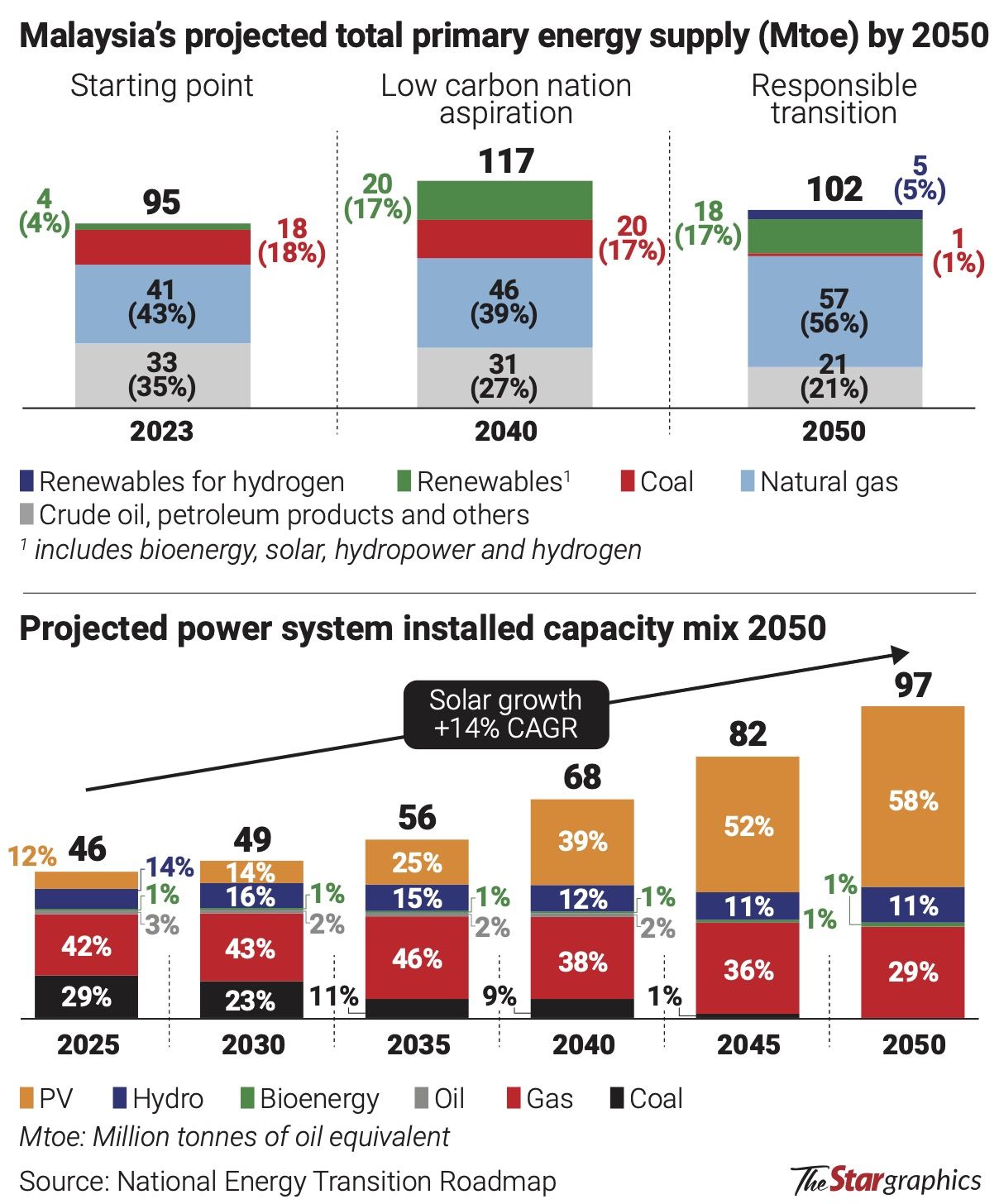

Malaysia needs the additional LNG supply primarily to feed the new generation of power plants being rolled out in the country. The surge in power demand is largely driven by structural shifts in the domestic economy.

Indeed, the data centre (DC)boom, coupled with a rise in the charging of electric vehicles at night is leading to another issue – can the national electricity grid handle all that new demand?

Compounding these challenges is the issue of financing.

Banks in Malaysia have significant exposure to Tenaga Nasional Bhd (TNB), the national energy utility company.

This is why financing new power plants (and expansion or extensions of existing power plants) is becoming tricky.

Going by the single customer limit regulations, banks will be hard-pressed to fund new power plants who have TNB as the offtaker.

There is also the whole renewable energy (RE) part.

One point that is being discussed more these days is the difference between installed capacity and actual energy generation.

The NETR projects that by 2050, approximately 58% of installed capacity will come from solar power.

Yet, the NETR acknowledges that by 2050, only 17% of energy supply will come from RE (led by solar).

The difference between installed capacity and actual supply, as explained by the NETR document itself is this: “The contribution of RE to the total generation mix will be comparatively lower than fossil fuels, particularly natural gas. This reflects the inherent low-capacity factor associated with solar, compared against the high-capacity factor of gas.”

While this would not have been a big issue three years ago, things are now looking different. Should we be questioning whether the billions being spent to roll out all those large scale solar power plants is the best use of our capital, when this energy source is only going to give us, at best, 17% of our energy supply by 2050?

Could the money be better spent, say, in building mini gas fired power plants to cater to the needs of residences (that are increasingly charging up their EVs at night), as well as for the DCs and industrial sectors?

That would also require more investment into upgrading of the peninsular gas utilisation facilities, as well as securing the supply of sufficient LNG.

It would also require more liberalisation to take place in Malaysia’s electricity supply landscape, facilitating more private enterprises to generate and supply electricity using the country’s grid, which remains firmly in the hands of TNB.

Meanwhile, in all the desperation to ensure sufficient energy supply in the country, is there a possibility that our coal-fired power plants are going to get extended?

Note that many countries including Malaysia have committed to wind down their coal-fired power plants.

Recent reports, however, indicate that TNB is seeking to secure a new supply of coal.

This is leading to some speculation that the coal-fired power plants in Malaysia could be extended. More than half of our electricity is generated today by burning coal.

Meanwhile, Sarawak is fine-tuning its hydrogen ambitions. Recent reports indicate the two major proposed hydrogen projects in the state, H2ornbill and H2biscus, are being adjusted in response to softer market demand and shifting economic realities.

This follows the fact that hydrogen projects worldwide are hitting a demand gap issue.

Buyers made up of parties in the shipping and other industries are not committing yet. This is resulting in hydrogen projects being scaled down globally.

Taken together, these developments underscore a sector in transition. Malaysia’s energy landscape is changing rapidly, shaped by geopolitical uncertainties, structural demand shifts, financing constraints and the complexities of the energy transition.

Ensuring long-term energy security will require not only careful policy recaliberation but also more integrated and forward-looking planning across the entire energy value chain.