Michael Burry Has Soured on Palantir and Is Betting on This Other Beaten-Down Artificial Intelligence (AI) Software Stock Instead

Key Points

Burry is an outspoken investor best known for predicting the subprime mortgage crisis.

Recently, he soured on Palantir stock and is instead opting to buy shares of Salesforce.

Both stocks have struggled as growth investors have rotated away from the software industry.

Michael Burry is once again grabbing headlines after posting some polarizing content on his Substack blog. The investor who famously bet against the U.S. housing market ahead of its 2008 crash is now openly souring on Palantir Technologies (NASDAQ: PLTR) while signaling optimism about Salesforce (NYSE: CRM) by opening a fresh stake in it.

In a market obsessed with artificial intelligence (AI) hype, Burry's contrarian trading decisions bring a deeper narrative to light: When every software-as-a-service (SaaS) company claims to be "AI-native," which ones are actually delivering durable value, and at what price?

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

The answer lies in how two very different enterprise platforms are navigating the same storm -- the so-called "SaaSpocalypse" that's being triggered by the debut of new agentic AI tools.

Image source: Getty Images.

Who is Michael Burry, and why should investors pay attention to him?

Burry is not your ordinary money manager. A former physician turned self-taught investor, he is best known for founding the hedge fund Scion Asset Management (which he recently shut down). During his tenure running Scion, Burry delivered spectacular returns following an early call on the subprime mortgage collapse. His story was later dramatized in the book and feature film The Big Short.

Burry's outspoken rhetoric and forensic approach to stock picking have garnered him a loyal following. He is known to spend countless hours poring over balance sheets, modeling cash-flow scenarios, and assessing competitive moats. In other words, he dives into the details rather than chasing narratives.

This is why, when he publicly critiques one AI sector darling and pivots toward another, it is not just a casual rotation. It is a signal that he thinks valuations are aggressively diverging from underlying economics.

Two software platforms with two very different philosophies

At first glance, Palantir and Salesforce look like cousins in the enterprise software industry. Both companies develop cloud-based platforms that help large organizations make sense of vast amounts of data. Over the last few years, each has poured billions of dollars into new generative AI features. And yet underneath the surface, Palantir and Salesforce have strikingly different DNA.

Palantir's strength is rooted in deep, ontology-driven data integrations. The company's Foundry and Gotham platforms act as digital command centers, fusing disparate data sources into real-time, operational intelligence. Throughout the AI revolution, the company has won massive deals with the U.S. government and Fortune 500 companies precisely because its systems are designed to thrive in high-stakes, messy environments where off-the-shelf tools often fall short.

By contrast, Salesforce is the undisputed market leader in customer relationship management. Its core platform unifies sales, professional services, marketing, and commerce into a single customer view that's supercharged by Einstein AI. Where Palantir excels at bespoke, mission-critical analytics, Salesforce dominates in standardizing high-volume commercial workflows.

The similarity between Palantir and Salesforce is obvious: Both companies sell recurring software subscriptions and are racing to embed large language models into their ecosystems.

The difference is in application. Palantir's edge lies in its depth, whereas Salesforce's advantage stems from ease of adoption. In other words, one platform feels like a custom-built supercomputer designed to conquer sophisticated problems, while the other feels like an indispensable operating system for facilitating everyday customer operations.

Valuation discipline in the "Age of AI" disruption

Both stocks have been punished lately, but for subtly different reasons, indexing on the same phenomenon.

The introduction of Claude CoWork and its peers has accelerated an idea that many growth investors were subconsciously fearing: AI agents that can draft emails, analyze pipelines, orchestrate campaigns, and even simulate entire sales cycles or business processes with minimal human oversight and input could render legacy enterprise software tools useless. Companies that once needed several specialized SaaS tools suddenly have a path to consolidation. In turn, subscription fatigue could swiftly result in IT budget cuts.

Palantir's lofty valuation multiples reflect sky-high expectations for the growth of its commercial Artificial Intelligence Platform (AIP). The selling pressure seen in Palantir stock over the last couple of months suggests that investors are entertaining the idea that growth could fail to accelerate as dramatically as Wall Street expects.

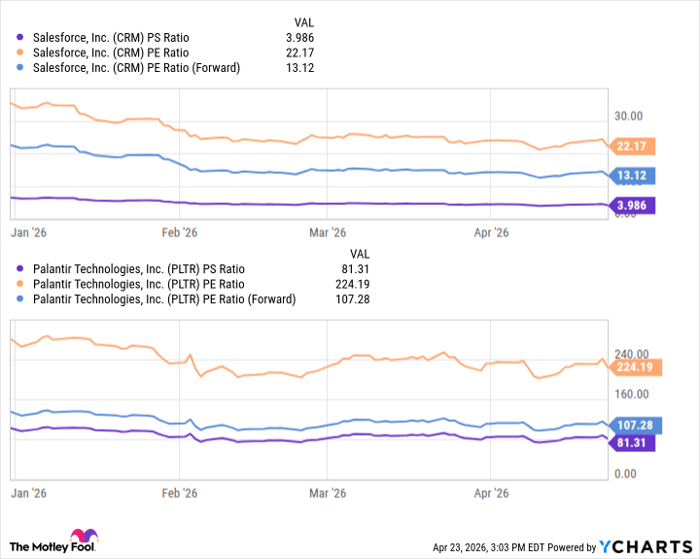

On the other hand, Salesforce was already trading at a more reasonable valuation compared to Palantir, despite years of steady execution. Salesforce, with its massive installed base and proven ability to cross-sell AI modules into existing customer contracts, potentially offers a more visible near-term path to earnings growth. Against this backdrop, Burry might think Salesforce looks like a bargain.

CRM PS Ratio data by YCharts.

For now, Burry has voted with his capital. Between the two software giants, Salesforce looks like the better value. His moves serve as a reminder to smart investors that in the SaaSpocalypse, the companies with the strongest economic moats and the most durable pricing power will endure.

While Salesforce's strength is in administrative tasks, Palantir's competitive edge is its ability to serve as the foundational data layer that will power the next decade of AI infrastructure, regardless of industry. Its ontology-first approach is better suited for an unstructured, multimodal data world that autonomous agents may never fully prosper in, despite their ubiquity. For this reason, I differ from Burry -- I see Palantir as the superior opportunity in the long run.

Adam Spatacco has positions in Palantir Technologies. The Motley Fool has positions in and recommends Palantir Technologies and Salesforce. The Motley Fool has a disclosure policy.