Adobe and Salesforce: Consistent Growth vs. Larger Scale in Revenue

Key Points

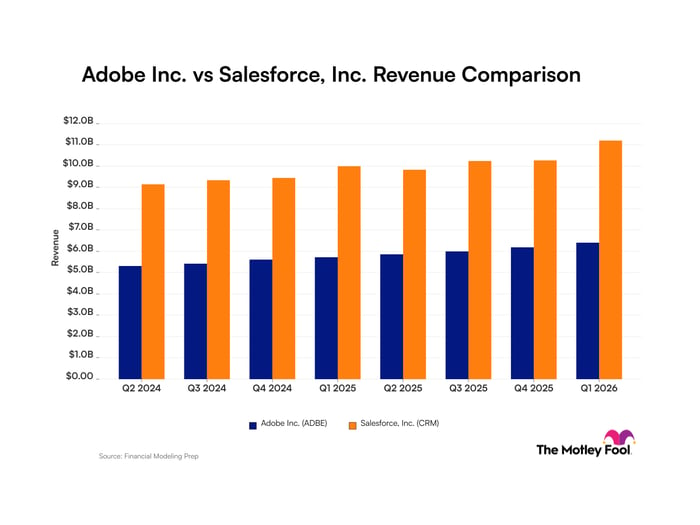

Salesforce currently generates a larger amount of total revenue than Adobe across recent tracking periods.

Over the last eight quarters, the two companies have largely maintained continuous quarter-over-quarter revenue growth, though Salesforce experienced one slight sequential decline in the middle of this time frame.

Investors should monitor whether the absolute revenue gap between the two companies continues to slowly widen or if the growth trajectories begin to converge in upcoming quarters.

Adobe: Consistent Growth in Revenue

Adobe (NASDAQ:ADBE) primarily generates revenue through software subscriptions across its digital media and digital experience divisions, enabling creators and enterprise marketers to design, manage, and optimize digital content.

It announced the acquisition of Semrush and the upcoming transition of its chief executive officer, while reporting an approximately 30% net income margin for the quarter ended Feb. 27, 2026.

Salesforce: Larger Scale in Revenue

Salesforce (NYSE:CRM) primarily earns revenue by offering cloud-based customer relationship management software, enterprise analytics tools, and workplace communication platforms that connect businesses with their end customers.

It executed an organizational restructuring that included workforce reductions and leadership changes, and it posted a net income margin of about 17% for the quarter ended Jan. 31, 2026.

Why Revenue Matters for Retail Investors

Revenue here refers to the data provider's standardized income statement revenue line item and serves as the foundational indicator of how much total money a business brings in from its core operations before any expenses, taxes, or operating costs are deducted.

Quarterly Revenue for Adobe and Salesforce

| Quarter (Period End) | Adobe Revenue | Salesforce Revenue |

|---|---|---|

| Q2 2024 | $5.3 billion (period ended May 2024) | $9.1 billion (period ended April 2024) |

| Q3 2024 | $5.4 billion (period ended Aug. 2024) | $9.3 billion (period ended July 2024) |

| Q4 2024 | $5.6 billion (period ended Nov. 2024) | $9.4 billion (period ended Oct. 2024) |

| Q1 2025 | $5.7 billion (period ended Feb. 2025) | $10.0 billion (period ended Jan. 2025) |

| Q2 2025 | $5.9 billion (period ended May 2025) | $9.8 billion (period ended April 2025) |

| Q3 2025 | $6.0 billion (period ended Aug. 2025) | $10.2 billion (period ended July 2025) |

| Q4 2025 | $6.2 billion (period ended Nov. 2025) | $10.3 billion (period ended Oct. 2025) |

| Q1 2026 | $6.4 billion (period ended Feb. 2026) | $11.2 billion (period ended Jan. 2026) |

Data source: Company filings.

Foolish Take

Adobe and Salesforce are two very well-known software stocks. Therefore, it should come as no real surprise that these two stocks have suffered over the last year, as the market has turned bearish on the software-as-a-service (SaaS) model. Both stocks have declined by about 34% over the last year.

That’s a tremendous departure for these two stocks, which have consistently delivered solid returns. Indeed, Adobe’s 20-year compound annual growth rate (CAGR) is 9.6%, while Salesforce’s is 16.2%.

Zooming in on each stock’s valuation, there does appear to be an opportunity. Adobe’s price-to-sales (P/S) ratio now stands at 4.2x — its lowest ratio in more than a decade. Similarly, Salesforce now sports a P/S ratio of 4.1x — its lowest value since the 2008/2009 financial crash.

Granted, there are concerns about the strength of SaaS business models amid rapidly advancing artificial intelligence (AI) capabilities. However, Adobe and Salesforce continue to deliver solid revenue growth, and both companies are aggressively integrating AI-powered features into their software offerings.

Growth-oriented investors with an eye for value may want to take a closer look at these two stocks.

Jake Lerch has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Adobe and Salesforce. The Motley Fool recommends the following options: long January 2028 $330 calls on Adobe and short January 2028 $340 calls on Adobe. The Motley Fool has a disclosure policy.