Many IPOs, little depth

BEHIND Malaysia’s impressive initial public offering (IPO) figures lies a far less flattering reality.

The local stock exchange is not just producing many IPOs – it is also producing many small or micro IPOs.

Over the past several years, Bursa Malaysia has seen a wave of micro IPOs raising less than RM50mil.

Many companies come to market with fundraising exercises so small they resemble private placements more than meaningful public listings.

The conversation around Bursa Malaysia has long centred on the lack of mega or “blockbuster” IPOs.

That remains a serious issue. Malaysia has not consistently produced the kind of billion-ringgit listings that dominate regional exchanges such as Hong Kong, India or even Indonesia.

But the rise of micro IPOs deserves equal scrutiny because it points to something deeper about the state of Malaysia’s capital markets.

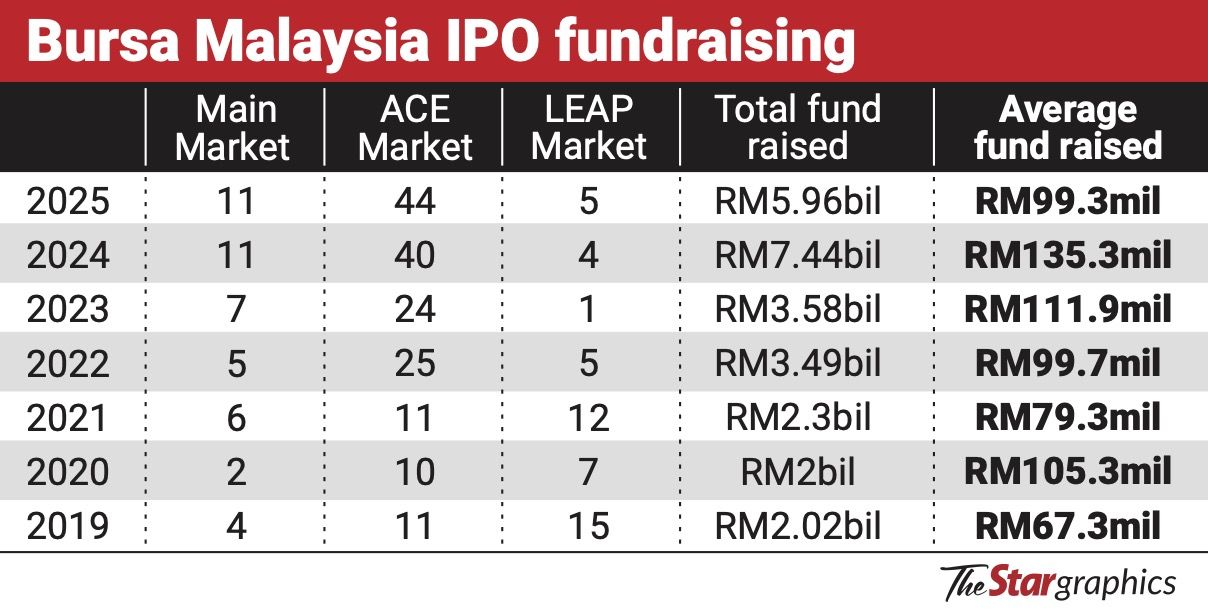

This partly explains the decline in total funds raised in the IPO space last year, despite an increase in the number of listings (see chart).

In 2025, while there were 60 IPOs on Bursa Malaysia, the total funds raised was RM5.96bil, compared to RM7.44bil in 2024 (55 IPOs).

This represents a decline of almost 20% in total funds raised.

Meanwhile, average funds raised dropped from RM135.3mil in 2024 to RM99.3mil in 2025.

BIMB Securities Research director of research Mohd Redza Abdul Rahman attributes the high number of micro-IPOs to two key factors.

One of them is Bursa Malaysia’s IPO key performance indicator or KPI, he tells StarBiz 7.

“The higher number of IPO target has been in place.

“This is also supported by Teraju’s (Unit Peneraju Agenda Bumiputra) aim of having more bumiputra companies going for listing.

“Another reason is the fact that the LEAP Market has been quiet, probably because of the lack of liquidity and only investors with selective profiles are allowed to invest.

“Hence, more and more companies resort to listing on the ACE Market,” according to Mohd Redza.

Tradeview Capital founder and chief executive officer Ng Zhu Hann says the high number of micro IPOs may also reflect the fact that Bursa Malaysia Bhd is the sole approving authority for the ACE Market.

“ACE Market listings only require Bursa Malaysia’s approval. There is no need for Securities Commission approval, which is required for the Main Market. So, the process of listing on the ACE Market is faster.”

Ng points out that more “mature” small and medium enterprises are opting for ACE Market IPOs as a fundraising avenue than in the past.

The number of ACE Market IPOs has increased tremendously in less than a decade.

From just six listings in 2017,

a total of 44 IPOs were recorded on the ACE Market in 2025.

This represents nearly three-quarters of total IPOs on Bursa Malaysia – across the Main, ACE and LEAP Markets combined. With this, Malaysia’s IPO market also topped South-East-Asia by volume. The 2025 performance was notably the highest since 2006.

In 2025, the domestic equity market also saw a first secondary listing – UMS Integrated Ltd – as well as the listing of a subsidiary of a South Korea Exchange-listed company in Malaysia, Cuckoo International (MAL) Bhd.

Deloitte Southeast Asia Ltd, in its Southeast Asia IPO Capital Market 2025 report, said the largest IPO of 2025 – Eco-Shop Marketing Bhd – came from the consumer industry.

In 2024, the largest IPO – 99 Speed Mart Retail Holdings Bhd – was also from the same sector.

While Malaysia led the region in terms of listing volume, Deloitte noted that none of South-East-Asia’s four “blockbuster” IPOs originated from the country.

The four IPOs, each raising more than US$500mil, came from Singapore, Vietnam and the Philippines.

A stock exchange cannot thrive on listing volume alone.

It needs depth. It needs scale.

It needs companies large enough to attract institutional participation, analyst coverage, foreign interest and sustained liquidity.

Without these, the market risks becoming crowded with small counters that generate excitement for a few trading sessions before fading into illiquidity.

The worrying part is not merely the existence of micro IPOs.

Smaller companies should have access to public capital markets, and many successful global firms began as small listings.

The issue lies in the concentration of such offerings.

When too many listings raise only modest sums, it raises uncomfortable questions about the overall quality and maturity of the pipeline.

Are Malaysian companies scaling aggressively enough before going public? Or are businesses listing too early because private funding avenues remain shallow and fragmented?

More importantly, what does it say about investor appetite when the market increasingly absorbs smaller and smaller deals while larger offerings struggle to emerge?

Mohd Redza says that more listings on the stock exchange do not necessarily result in market vibrancy as a whole.

“These IPO counters are generally active on the day of listing and maybe one to two days after, following which the volume generally dies off.

“Also, with the small listings, we don’t really gain much in terms of foreign fund inflows.

“I believe that’s why the government is now relooking at big listings, considering we don’t see many of the small listings becoming big behemoths,” he adds.

Institutional investors often cannot meaningfully participate in micro IPOs because of liquidity constraints. Foreign funds typically avoid them altogether.

This puts pressure on market liquidity. The fact that retail investor participation remains cyclical and sentiment-driven also does not help.

As a result, this weighs down the average daily trading volumes.

There is also the issue of capital efficiency.

Running a public-listed company is not cheap. Compliance costs, governance requirements, quarterly reporting obligations and investor relations commitments require significant resources.

For very small businesses, these costs can become disproportionately high relative to the capital raised.

This raises a difficult question. Are some companies genuinely listing because public markets are the best avenue for growth, or because listing itself has become an end goal?

In some cases, IPO exercises appear driven more by branding, shareholder exits or short-term valuation gains rather than long-term expansion strategies.

The danger is a gradual dilution of market quality.

Investors begin viewing IPOs less as opportunities to participate in future corporate champions and more as short-term trading vehicles.

Market confidence becomes increasingly dependent on listing pops instead of long-term value creation.

Malaysia cannot afford that outcome. It risks being trapped in an uncomfortable middle ground where it produces many IPOs, but too few that genuinely move the needle.

The irony is that Malaysia does have companies capable of scaling into larger listings.

The country has strong ecosystems in semiconductors, healthcare, industrial technology, digital infrastructure and consumer brands.

Johor’s data centre boom

alone could eventually produce sizeable listing candidates.

Private companies in logistics, renewable energy and manufacturing are also expanding aggressively.

But the market needs to encourage these firms to grow bigger before going public.

This may require stronger private capital ecosystems, deeper venture funding pools and policies that incentivise scale rather than speed to listing.

Beyond this, regulators may also need to actively scout high-quality regional companies for listing in Malaysia.

This would require more proactive “door-knocking” efforts, rather than waiting for firms to approach the exchange.

At the same time, Bursa Malaysia and regulators may eventually need to rethink what success truly looks like.

Mohd Redza recommends a two-pronged strategy for Bursa Malaysia.

First, he says, the exchange should encourage more listings and prevent the loss of Malaysian companies to other markets.

Second, there should also be a focus on attracting large-cap listings.

“This is important so that we could increase our weightage in MSCI regional indices.

“We need to get Malaysia on the map of global investors – firstly through passive investors via index or exchange-traded fund investing, and gradually building the trust of active investors,” says Mohd Redza.