NRW Holdings (ASX:NWH) Is Up 8.4% After Securing A$200m Tonkin Highway Upgrade Contract - What's Changed

- NRW Holdings has recently secured a major A$200,000,000 Tonkin Highway corridor upgrade contract, adding a sizeable infrastructure project to its existing operations across Australia.

- This win further broadens NRW’s mix of mining and civil work, which may influence how investors think about its future revenue profile and risk balance.

- We’ll now explore how this large Tonkin Highway contract win could influence NRW Holdings’ existing investment narrative and expectations.

Uncover the next big thing with 59 elite penny stocks that balance risk and reward.

NRW Holdings Investment Narrative Recap

To own NRW Holdings, you need to be comfortable with a contractor whose fortunes hinge on securing and delivering large mining and civil projects while managing slim margins, weather disruptions and client risk. The A$200,000,000 Tonkin Highway win supports the near term revenue pipeline and slightly tilts the story toward public infrastructure, but it does not remove the key short term risk around earnings volatility from project execution, pricing pressure and exposure to a handful of large counterparties.

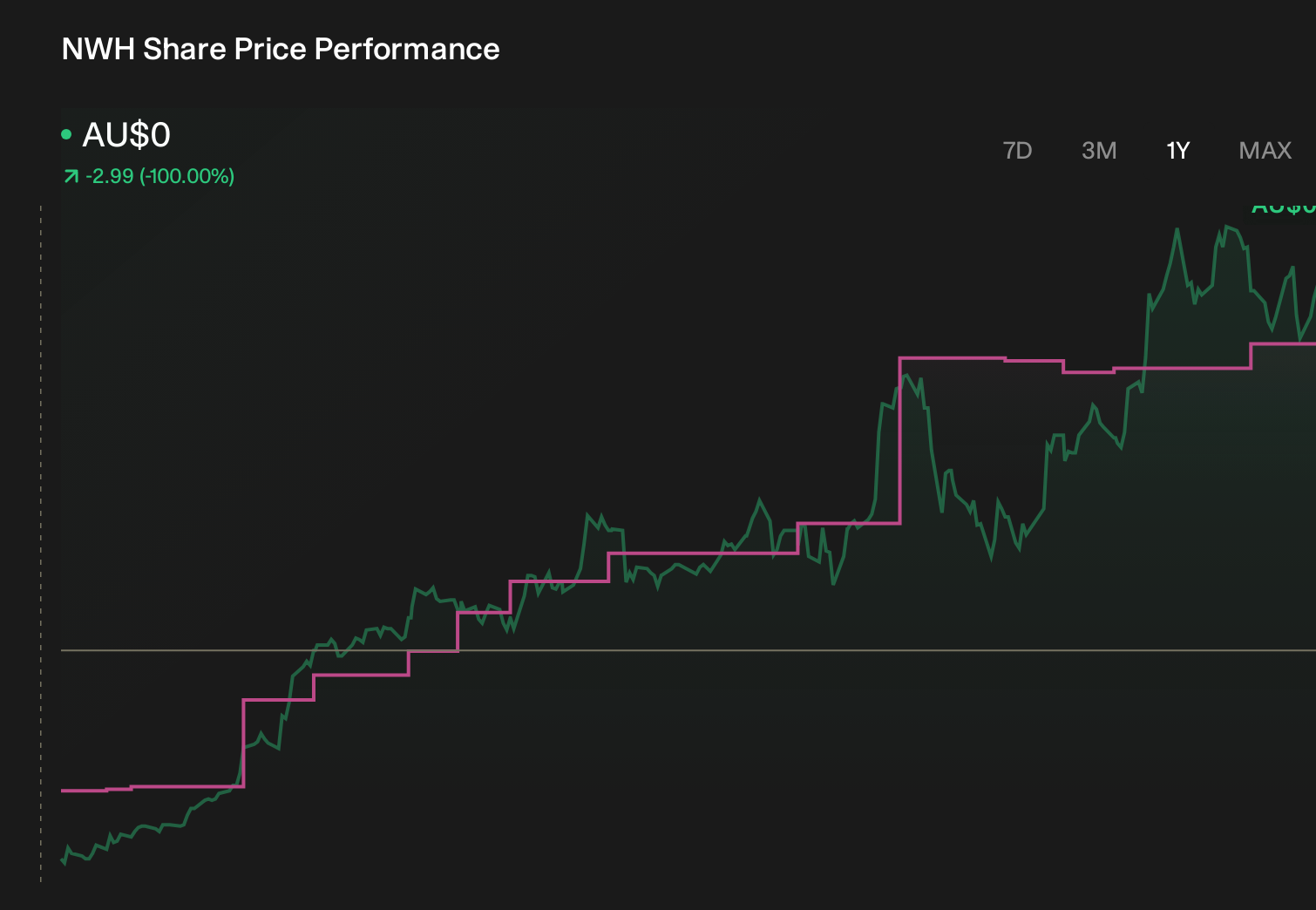

The Tonkin Highway contract lines up most clearly with NRW’s recent guidance that pointed to full year 2026 revenue of A$4.1 billion to A$4.2 billion and highlighted a strong civil and infrastructure workload. This new win sits within that broader order book story, reinforcing why earnings and cash conversion remain the main catalysts to watch, especially after the share price has already climbed sharply on expectations of better utilisation and margin stability.

Yet while the contract pipeline looks encouraging, investors should also be aware of how delays or cancellations in government backed infrastructure work could...

Read the full narrative on NRW Holdings (it's free!)

NRW Holdings' narrative projects A$4.7 billion revenue and A$209.0 million earnings by 2029. This requires 9.5% yearly revenue growth and an A$160.2 million earnings increase from A$48.8 million today.

Uncover how NRW Holdings' forecasts yield a A$6.59 fair value, a 14% downside to its current price.

Exploring Other Perspectives

The most pessimistic analysts were pencilling in only about 5.8 percent annual revenue growth to roughly A$4.3 billion by 2029, reminding you that opinions on NRW’s A$25.2 billion pipeline and contract conversion risk can differ sharply and that this Tonkin Highway win could yet shift both the bullish and bearish stories.

Explore 6 other fair value estimates on NRW Holdings - why the stock might be worth as much as 70% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your NRW Holdings research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free NRW Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate NRW Holdings' overall financial health at a glance.

Seeking Other Investments?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 30 companies in the world exploring or producing it. Find the list for free.

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com