COMPASS Pathways (CMPS) Is Up 13.9% After Swinging From Loss To Q1 2026 Profit - What's Changed

- In the first quarter of 2026, COMPASS Pathways plc reported net income of US$91.2 million, reversing a prior-year net loss and posting basic earnings per share from continuing operations of US$0.71 versus a loss per share of US$0.20.

- The simultaneous reporting of positive basic earnings per share and a diluted loss per share from continuing operations highlights how capital structure and potential share issuance still weigh on fully diluted profitability.

- With COMPASS Pathways moving from a net loss to meaningful net income, we’ll now explore how this shifts its longer‑term investment narrative.

We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

COMPASS Pathways Investment Narrative Recap

To own COMPASS Pathways, you need to believe that COMP360 can clear Phase III, secure FDA approval in treatment resistant depression and be adopted across existing interventional psychiatry centers. The sudden swing to US$91.2 million in quarterly net income does not materially change that near term catalyst, and the biggest risk remains any delay or setback in the TRD Phase III and approval path that could extend cash use and increase pressure for further dilution.

The recent FDA decision to grant a rolling review for COMP360 and include it in the CNPV program for treatment resistant depression is the announcement that most closely aligns with this earnings release. Together, they frame a company that is still pre revenue but now pairing clearer regulatory visibility with a temporarily improved bottom line, which could influence how you think about the timing and scale of future funding needs versus the potential commercial opportunity if TRD approval is achieved.

Yet despite the eye catching Q1 profit, investors should be aware of how dilution risk could still affect long term ownership...

Read the full narrative on COMPASS Pathways (it's free!)

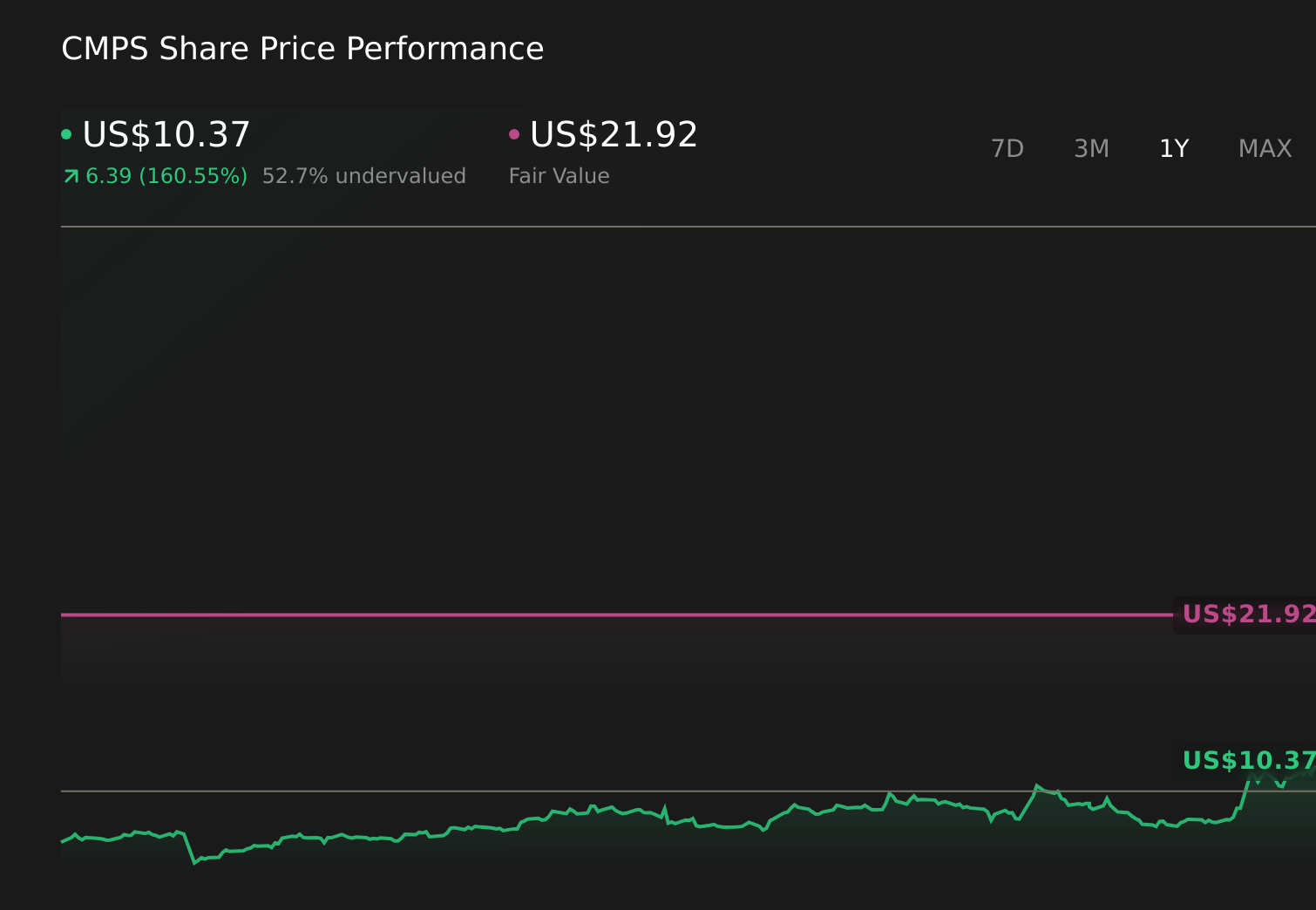

COMPASS Pathways' narrative projects $193.1 million revenue and $24.2 million earnings by 2029. This implies an earnings increase of about $261.5 million from -$237.3 million today.

Uncover how COMPASS Pathways' forecasts yield a $21.92 fair value, a 86% upside to its current price.

Exploring Other Perspectives

Before this earnings surprise, the most optimistic analysts were assuming COMPASS might reach about US$670.7 million in revenue and US$242.9 million in earnings by 2029, so if you agreed with that far more bullish view compared with consensus, this quarter’s profit and the evolving regulatory story might either reinforce your conviction or prompt you to revisit how quickly those targets could realistically be achieved.

Explore 5 other fair value estimates on COMPASS Pathways - why the stock might be worth just $14.56!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your COMPASS Pathways research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

- Our free COMPASS Pathways research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate COMPASS Pathways' overall financial health at a glance.

Interested In Other Possibilities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Capitalize on the AI infrastructure supercycle with our selection of the 46 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 14 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com