A fluid gas market

FOR decades now, Malaysia’s gas-fired power sector has been fuelled by Petroliam Nasional Bhd (PETRONAS) – but that is about to end next year.

After 2027, a new phase will begin with several legacy contractual frameworks expiring.

The old arrangement has been in place for very long now – since the development of Peninsular Malaysia’s gas-fired power sector and was designed to provide gas at a relatively controlled or discounted structure, supporting the country’s rapid industrialisation in its earlier years.

However, the environment that supported this model is changing rapidly.

Domestic gas fields are maturing, liquefied natural gas (LNG) imports are rising, power demand is growing and the downstream gas sector is gradually opening to broader participation.

With the framework nearing expiry, how will the domestic gas market evolve?

The question becomes even more relevant considering Malaysia is undergoing a new wave of power plants that need more gas, not to mention the existing ones some of which have been granted extensions so as to meet the country’s surge in energy demand.

Industry observers note that newer gas-fired power projects are being developed under different commercial arrangements, including shorter power purchase agreement (PPA) tenures and greater responsibility for developers to secure fuel supply.

The bulk of natural gas supply in Peninsular Malaysia comes from PETRONAS’ gas fields off the east coast which are processed at Kerteh, Terengganu and distributed through the massive Peninsular Gas Utilisation (PGU) pipeline network, which is owned and operated by the national oil company’s subsidiary PETRONAS Gas Bhd (PetGas).

As Peninsular Malaysia’s gas demand grew and domestic supply from mature fields tightened, PETRONAS increasingly supplemented supply through imported LNG cargoes sourced from the global market.

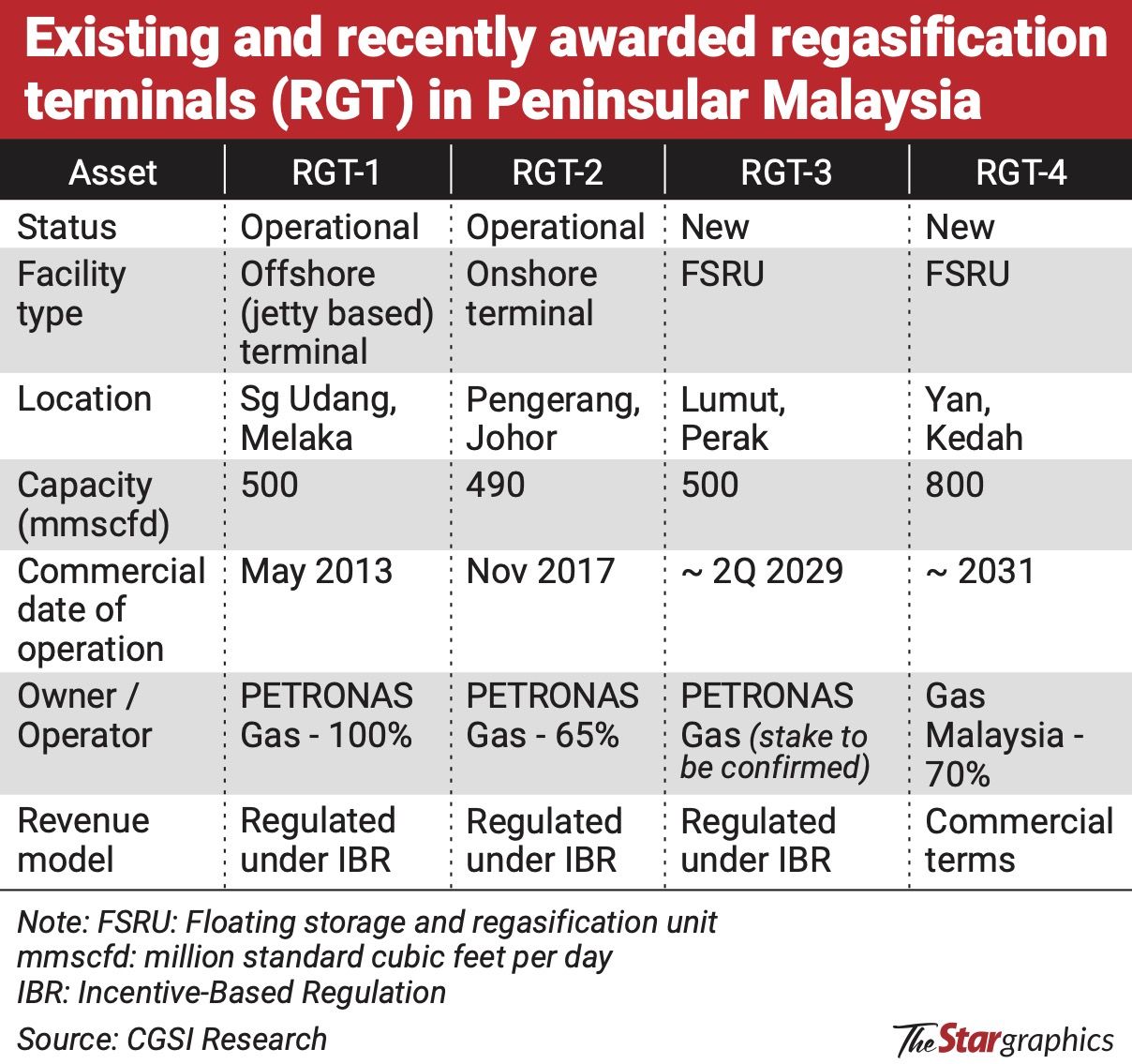

To support this, PETRONAS developed two regasification terminals (RGTs), one in Sungai Udang, Melaka and another in Pengerang, Johor.

The imported LNG is then converted into natural gas at those facilities and pumped into the PGU for local needs.

In March, Gas Malaysia Bhd secured the Energy Commission (EC)’s approval to proceed with a LNG RGT project in Yan, Kedah (RGT-Yan).

Early this month, PetGas announced plans to develop RGT-3 in Lumut, Perak, adding to its existing RGT-1 and RGT-2 assets.

Both new RGTs will be developed under the floating storage and regasification unit concept, which allows for faster deployment and lower capital requirements compared to traditional onshore terminals.

The entry of Gas Malaysia into LNG regasification infrastructure is viewed by industry observers as a significant step toward broader downstream participation in the gas sector, as it is the first non-PETRONAS-linked listed entity to be involved in developing such a facility.

PETRONAS owns close to 15% in Gas Malaysia, a downstream gas distributor.

MMC Corp Bhd, with 31%, is Gas Malaysia’s major shareholder followed by Tokyo Gas Co Ltd (18.5%).

EC study signals potential reforms

A sign that the gas market could be evolving came earlier this month when the EC issued a Request for Proposal to appoint a consultant to develop a “Competitive Gas Market Structure for Peninsular Malaysia” study.

Industry observers say the key word is not just “competition” but “structure,” pointing to a possible review of how gas is procured, transported and priced across the peninsula.

First, some context. The sector is typically divided into three segments: the power sector; the large industrial users such as petrochemical plants and other energy-intensive facilities, including steel plants, which are directly connected to the PGU network; and the non-power sector, which is the supply of gas to industries.

Within the gas value chain, the upstream sector remains heavily dominated by PETRONAS in its various roles.

It is resource owner under the production sharing contract framework, the national oil company, upstream operator, LNG exporter and gas aggregator.

PETRONAS carried out the Gas Masterplan Study in 1981, which laid the foundation for the long-term development and integrated planning of Malaysia’s gas industry, including the recommendation to develop the PGU pipeline network.

Gradual liberalisation of the sector followed through the Gas Supply (Amendment) Act 2016 and the introduction of Third-Party Access (TPA) in 2017.

These reforms allowed licensed third parties to access regasification terminals, transmission pipelines and distribution networks under regulated terms. The intention was to create a framework for broader downstream participation and future competition in gas supply and services.

However, while infrastructure access was liberalised, gas molecule supply into the peninsula system remains largely coordinated through PETRONAS’ gas aggregation structure.

“The government introduced TPA as the first step toward liberalisation, with the broader goal of moving from regulated or subsidised pricing toward more market-based pricing.

“At that time, our gas liberalisation was at an early stage, with not all legal and regulatory components fully in place,” an industry player familiar with the sector tells StarBiz 7.

The TPA, he says, was intended to allow multiple entities to access gas facilities on the same terms and to promote healthy competition and reliable gas supply.

However, the market remains only partially competitive in practice, he says.

“A competitive market structure goes beyond infrastructure access. It raises broader questions about how gas should be procured, priced, transported, balanced, contracted and traded in a market with potentially multiple buyers and sellers,” the industry player explains.

He notes that earlier reforms were introduced cautiously.

This, he says, should not be seen as a criticism of the existing system, which was designed to prioritise supply security, affordability, coordinated infrastructure development, industrial growth and broader national strategic interests during a period when domestic gas resources were relatively abundant.

He adds that the EC’s study is likely part of preparations for the next phase of gas market reform.

Industry players say changes to the gas market structure will need to take into account the central role of the power sector.

This is because gas is a commodity which is closely linked to electricity tariffs, industrial competitiveness and national energy security.

Independent power producers secure fuel through long-term gas supply agreements in line with their PPAs with Tenaga Nasional Bhd, the country’s main electricity utility and single buyer in the power sector.

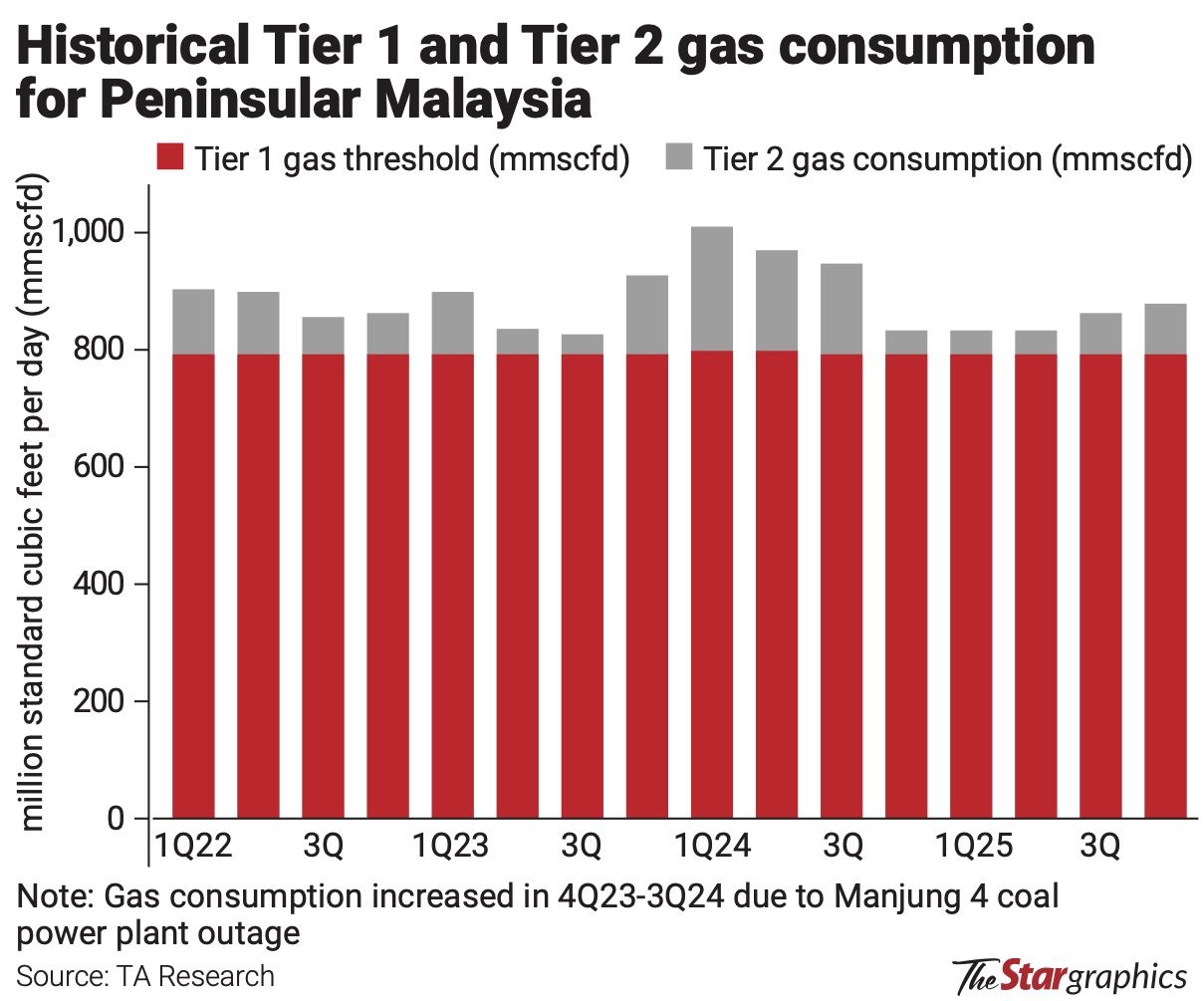

The power sector currently operates under a two-tier gas pricing structure.

A certain volume of gas supply (Tier 1) is provided at a regulated or capped price, while additional gas requirements beyond that threshold (Tier 2) are priced based on market-linked LNG prices.

This structure was designed to balance electricity affordability with the gradual transition towards more market-reflective gas pricing, while helping to ensure relatively stable and predictable fuel costs for power generation.

According to industry players, this is also one reason market dynamics have evolved only gradually despite the introduction of TPA.

Emerging new realities

However, Peninsular Malaysia is soon set to face a more complex gas landscape.

The declining domestic gas supply from mature fields may lead to higher reliance on LNG imports as demand grows from the power and industrial sectors, like data centres.

“Many of Peninsular Malaysia’s legacy producing fields are maturing, so production growth is slowing.

“As development shifts toward smaller and more technically challenging fields, costs are likely to rise, making long-term domestic supply more challenging to sustain,” says a retired gas official.

According to him, PETRONAS’ recent long-term LNG import deal with QatarEnergy points to the growing need for external gas supply.

“This does not mean we are running out of gas. Rather, the era of relatively cheap and easily accessible domestic gas is gradually giving way to a more complex and costlier supply,” the former official says.

To be sure, Malaysia remains one of the world’s important LNG exporters, with a major LNG complex in Bintulu, Sarawak operated by PETRONAS.

However, most of this output is exported under long-term contracts to Japan, South Korea and China.

“Historically, the domestic gas framework was built around relatively stable indigenous supply economics.

“However, greater reliance on imported LNG introduces exposure to global price volatility, geopolitical risks, shipping disruptions and international market dynamics,” he says, adding that gas pricing mechanisms for the power sector may eventually need to evolve to remain sustainable.

New LNG entry points and supply flexibility

Peninsular Malaysia is set to see an increase in LNG entry points, with both RGT-Yan in Kedah and the planned RGT-3 in Lumut, Perak, adding regasification capacity across the northern and central corridors.

“The entry points for LNG imports are currently RGT-1 and RGT-2, which are located in the south. A new LNG entry point in the north of the peninsula could enhance supply routing flexibility,” an analyst who covers the power sector says.

He says northern Malaysia is continuing to develop as a hub for manufacturing, industrial parks, data centres, energy-intensive industries and cross-border integration with Thailand.

Notably, RGT-Yan is being developed under a more commercially driven structure compared with traditional regulated gas infrastructure assets, which industry players say could represent an early step toward a more decentralised and flexible gas infrastructure system.

Under this model, Gas Malaysia and its partners (Tokyo Gas and Netherlands-based VTTI) will assume greater market risk in the RGT-Yan project.

Such developments typically require large-volume customers, stable and predictable demand, as well as long-term anchor off-takers backed by commercially negotiated contracts.

While risks are higher, so are potential returns, the analyst says.

“For example, if LNG demand weakens, or the terminal is underutilised, or competing supply routes become cheaper, earnings from the project could be affected,” the analyst says.

This is in contrast to RGT-3, which is structured under an incentive-based regulation (IBR) framework, similar to RGT-1 and RGT-2, and aligned with centrally coordinated national gas supply planning.

Under IBR framework used for RGT-3, tariffs and returns are regulated by the EC, resulting in more predictable returns and lower market exposure.

On the other hand, RGT-Yan’s commercial structure places greater emphasis on utilisation levels, customer demand and commercially negotiated agreements.

Neither model is necessarily better than the other, according to industry players.

“In reality, both can have their space – regulated infrastructure for stability, and commercial models for flexibility and market response,” one player involved in oil and gas believes. RGT-Yan may thus represent an interesting transitional case, he adds.

However, some say the single-aggregator structure could limit the ability of projects like RGT-Yan to independently source LNG and participate in a more open gas market.

Despite the TPA, they note that the number of truly active and significant competing gas suppliers remains relatively limited.

So could more than one gas aggregator eventually coexist within the system with PETRONAS remaining the national anchor?

“Perhaps then we could have a second consortium of aggregators, operating under regulated rules, serving defined market segments such as large industrial users and data centres where future demand is expected to emerge.”

According to the industry player, such an arrangement could introduce greater flexibility, while preserving overall systems stability, infrastructure coordination and energy security with PETRONAS continuing to play its strategic national role as the market evolves.

The middle path

The retired gas official says Peninsular Malaysia’s gas sector is now entering a transitional phase – moving gradually from a historically centralised and domestically anchored system toward a more flexible, LNG-linked and commercially dynamic market structure.

“Currently, we are neither a fully regulated monopoly in the traditional sense nor a fully open and competitive system comparable to those in parts of Europe, the United Kingdom or North America,” he says.

According to him, this “middle path” position is what makes the EC study important, although it remains an early-stage exercise.

Any reform is expected to be implemented in a phased and managed manner, similar to previous market adjustments.

“The question is no longer whether gas will remain important – it clearly will for the foreseeable future.

“The real challenge is how the market should evolve to remain secure, investable, competitive and transition-ready in a far more complex energy landscape,” the retired gas official adds.