Prediction: Broadcom Stock Is Going to $1,000 by 2028

Key Points

Broadcom's growth accelerated impressively last quarter, and the good part is that it is poised to deliver even stronger growth going forward.

The phenomenal earnings growth Broadcom can deliver could make it a multibagger within the next three years.

Shares of Broadcom (NASDAQ: AVGO) received a big jolt following the release of the company's fiscal 2026 second-quarter results (for the three months ended May 3) on June 3. The chip designer missed Wall Street's revenue expectations, and investors weren't happy about the fact that it didn't raise its guidance for next year.

Broadcom stock was down nearly 8% the following day. However, savvy investors can consider this pullback as a buying opportunity, especially considering that Broadcom is benefiting big time from the growing demand for custom artificial intelligence (AI) processors and networking chips.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Let's look at the reasons why it makes sense to buy Broadcom stock following its latest slide.

Image source: The Motley Fool.

Broadcom couldn't meet the market's ambitious targets, but the bigger picture remains intact

Broadcom's fiscal Q2 revenue increased 48% year over year to $22.2 billion. Its non-GAAP earnings per share increased at a stronger pace of 54% year over year to $2.44 per share. Analysts, however, were expecting $22.27 billion in revenue from Broadcom. What's more, Broadcom's forecast of $16 billion in AI chip revenue for the current quarter was also lower than the $16.36 billion consensus estimate.

Additionally, Broadcom stuck to its fiscal 2027 AI revenue forecast of $100 billion, and that didn't sit well with investors, who were expecting it to increase that number. However, a closer look at Broadcom's performance and guidance will make it clear the stock's slide isn't justified. After all, its growth more than doubled from the 20% year-over-year revenue jump it clocked in the same period last year. The bottom-line growth was also better than the 44% increase seen a year ago.

Broadcom's AI business was the primary driver of its growth. The company reported a 143% year-over-year increase in AI revenue to $10.8 billion, exceeding its $10.7 billion forecast. In fact, Broadcom's revenue and adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) margin exceeded the company's forecasts.

Still, the market's heightened growth expectations for AI infrastructure stocks explain the knee-jerk reaction to Broadcom's earnings report. Investors, however, shouldn't miss the fact that Broadcom delivered impressive revenue and earnings growth last quarter. More importantly, its guidance for $29.4 billion in revenue for the current quarter points to a stronger year-over-year jump of 84% in its top line.

This should pave the way for another big increase in Broadcom's earnings in the current quarter. Looking ahead, Broadcom anticipates $56 billion in AI chip revenue in fiscal 2026, which would be an increase of 180% over the prior year. This will be followed by another impressive increase in fiscal 2027 to at least $100 billion.

So, while management may not have increased its fiscal 2027 revenue guidance, it continues to point out that its AI revenue will "be in excess of $100 billion" next year. The open-ended nature of that guidance suggests Broadcom's AI revenue could indeed exceed $100 billion.

It won't be surprising to see the company's AI revenue indeed exceed that mark, as it is poised to ramp up the deployment of its custom AI processors and networking components for multiple customers, such as Anthropic, Google, OpenAI, Meta Platforms, and others. Broadcom management notes that it has six core customers who will ensure that its AI semiconductor continues to grow into fiscal 2028 as well.

It has added two new customers to whom it will start shipping later this year, and expects to accelerate shipments to them next year. Moreover, the health of the custom AI processor and networking markets suggests that Broadcom's solid growth will last well beyond the next couple of years.

According to Bloomberg, the custom AI processor market could clock an annual growth rate of 27% through 2033. Meanwhile, Gartner projects that demand for AI networking components could increase at an annual rate of 38% through 2029. So, it is easy to see why analysts have become more bullish about Broadcom's earnings growth prospects.

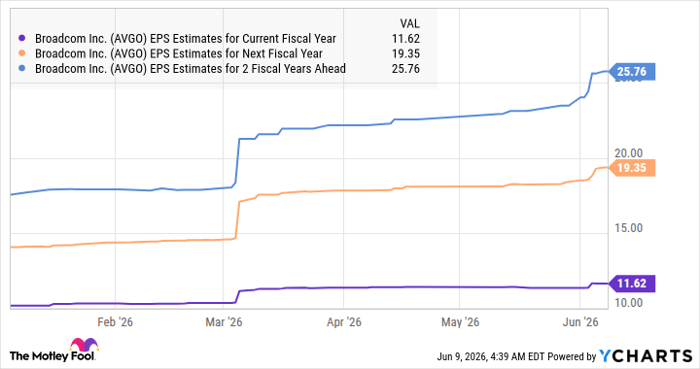

Data by YCharts

The stock's earnings trajectory suggests that a $1,000 stock price is indeed possible

One reason investors were expecting more from Broadcom was its expensive valuation. The stock trades at 64 times earnings. However, the forward earnings multiple of 34 is significantly lower, indicating that its bottom line is on track to grow significantly this year.

Broadcom's earnings per share increased by 40% in fiscal 2025 to $6.82. The consensus estimate of $11.62 per share points to a potential jump of 70% in the current fiscal year, followed by substantial increases over the next couple of years, as shown in the previous chart. Assuming its earnings indeed increase to $25.76 per share in fiscal 2028 and it trades at a significantly discounted 40 times earnings at that time (almost in line with the Nasdaq Composite index's average earnings multiple of 40), Broadcom could jump to just over $1,000 within the next three years.

That suggests potential upside of 2.5x, which is why the recent slide in this AI stock should be treated as a buying opportunity.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Broadcom and Meta Platforms. The Motley Fool recommends Gartner. The Motley Fool has a disclosure policy.