The economics of rooftop solar power

THE idea of placing solar panels on rooftops is hardly new. Malaysia has spent more than a decade rolling out programmes to encourage households and businesses to generate their own electricity, making rooftop solar a key pillar of the country’s renewable energy (RE) initiatives.

In Europe, Australia and even some parts of China, rooftop solar is widespread, despite the sun’s irradiation being lesser than in Malaysia.

So, how is Malaysia faring with tapping the rooftop solar potential? This question comes into focus considering the increasing realisation that utilising large swathes of land for solar farms is not the most economic use of land after all.

On the face of it, the figures don’t look that bad.

One report quoting the Energy Commission’s (EC) statistics as of July 2025 notes that rooftop solar capacity has reached 1.72GW, accounting for roughly 40% of Malaysia’s total installed solar capacity.

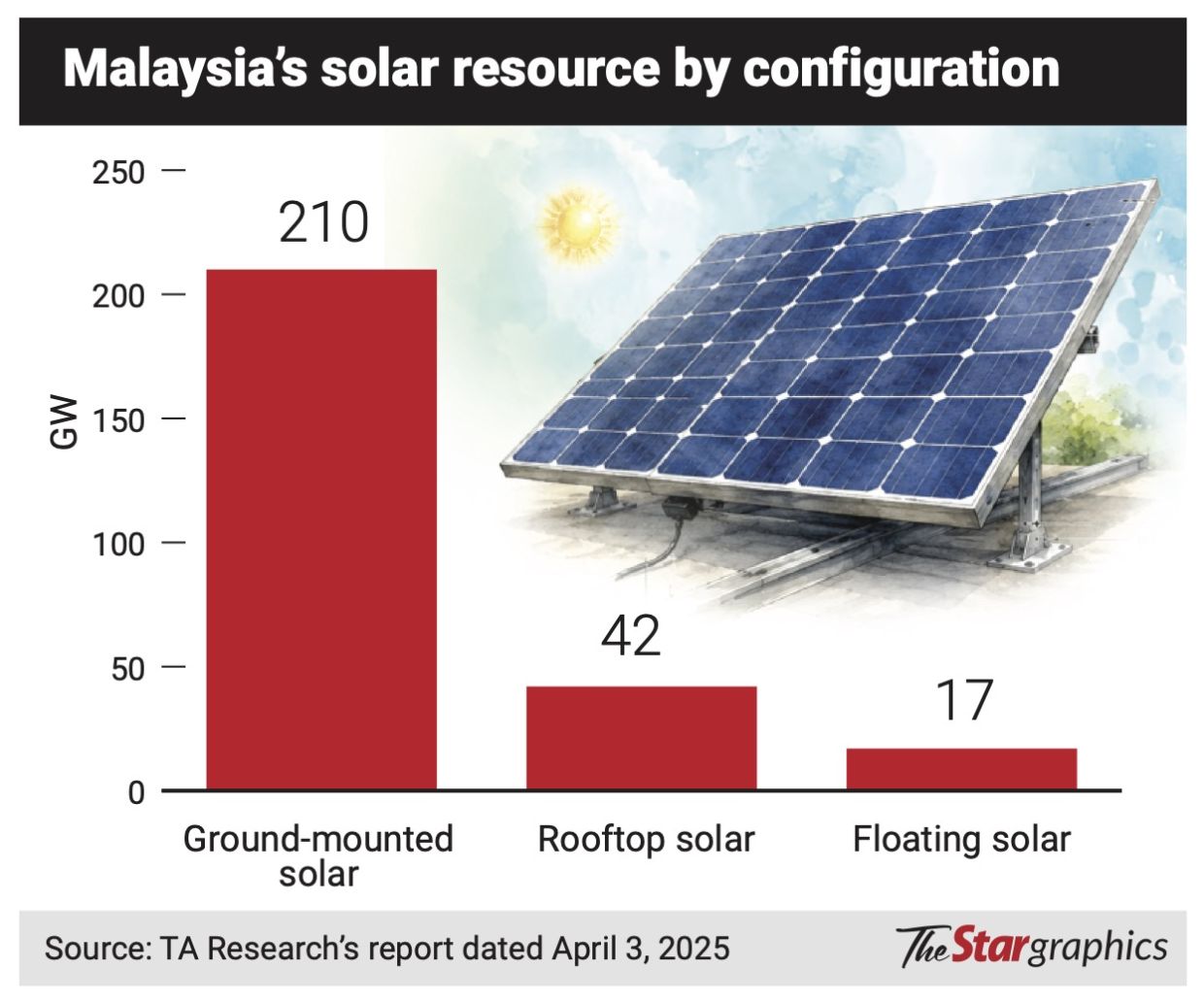

This represents a small percentage of Malaysia’s estimated 42GW rooftop solar potential. However, this figure aggregates rooftop solar installations across households, businesses and industrial facilities.

Industry players say the capacity reached so far is driven by the commercial and industrial sectors. Residential penetration remains relatively limited.

Malaysian Photovoltaic and Sustainable Energy Industry Association (MPSEA) president Justin Sim says residential rooftop solar has been installed on only about 2% of Malaysia’s estimated five million landed homes.

Part of this can be traced to the way the country’s rooftop solar policies have evolved over time, influencing both access and economics for residential users.

The country has introduced a series of rooftop solar programmes over the years, beginning in 2011. The earlier programmes provided financial incentives for those who had installed solar panels on their rooftops. Subsequent programmes have reduced those incentives, but still make it feasible for house owners, especially if electricity usage is high.

The feed-in tariff (FiT) ran from 2011 to 2016 before being replaced by a programme called net energy metering (NEM), which ended last year.

More recently, Solar Atap was introduced, which halved the financial incentive in terms of energy bills.

Of more interest is a new programme called community renewable energy aggregation mechanism (Cream), which allows homeowners, instead of investing in solar panels on their roofs, lease that real estate to a third party who then spends all the capital required to put together a sort of virtual solar farm on a group of homes in a particular residential area.

But first, looking at NEM and Solar Atap, Sim says one of the reasons households have been less encouraged to adopt rooftop solar is because of Malaysia’s relatively low electricity tariffs.

This reduces the financial incentive for homeowners to invest in solar systems compared with markets where power prices are significantly higher.

As a general rule of thumb, households with monthly electricity bills of RM400 to RM700 are considered to be in a viable range for rooftop solar returns, while those paying above RM700 stand to gain the strongest financial benefits.

However, earlier statements by Tenaga Nasional Bhd suggest that only around 83,000 households, or about 1% of domestic electricity users, fall into this higher-consumption category.

Then, there is the changing economics of rooftop solar.

“Under the Solar Atap, homeowners can no longer offset their electricity bills on a one-to-one basis as they could under earlier NEM schemes.

“As most households consume less electricity during the day when solar generation peaks, a large share of the power generated is exported to the grid, reducing the overall financial benefit,” Sim tells StarBiz 7.

Industry players echo this view.

Pekat Group Bhd group managing director Chin Soo Mau says consumers have found it difficult to plan with confidence because of frequent changes to rooftop solar policies. While the economics remains positive, it is less compelling than it was a year ago, he adds.

“The market has moved from NEM 1.0 to NEM 2.0 to NEM 3.0, followed by a six-month gap after NEM 3.0 ended in June 2025 before Solar Atap was introduced in January 2026.

“Each transition brought different rules on export credits, system sizing and quotas.”

Pekat is one of the companies active in this space via wholly-owned Solaroo Systems Sdn Bhd. A typical residential system of 5kWp to 8kWp costs between RM18,000 and RM35,000 to install, according to Chin.

He says under the previous NEM 3.0 framework, payback periods ranged from three to six years. However, lower export credits under Solar Atap have extended this to about six to 10 years, particularly for households with lower daytime electricity consumption when solar generation is at the highest.

According to him, the shift to Solar Atap appears to favour greater self-consumption of solar power, rather than reliance on exporting excess electricity to the grid.

One key piece of the adoption puzzle is financing. Solaroo’s executive director Johann Sze says the financing market is “reasonably developed”.

“Credit card installment plans of up to 60 months are widely available. There are also rent-to-own offerings but their rates remain relatively high, and take-up has been limited,” he says, adding that while rebates have helped ease upfront costs to some extent, affordability remains an important factor for many households.

“The single biggest unlock for middle-income adoption is low-cost, long-tenor financing.

“A solar system that costs RM25,000 upfront is a fundamentally different proposition from one that costs RM300 a month over 84 months with immediate bill savings,” he says.

Sze adds that a coordinated push with commercial banks and development financial institutions on green home financing, ideally linked to home purchases or refinancing so the cost is built into the mortgage, would improve affordability for the middle 40% income group.

Tapping idle residential roof space

However, this still leaves a segment of lower-usage or more cost-sensitive households that may not fully benefit from traditional models, prompting efforts to “socialise” access through new approaches such as Cream, introduced in February last year under the third-party access framework.

Under this model, house owners act as “roof landlords”, leasing the space to developers who finance, install and operate the solar systems. In return, they receive a leasing fee.

The electricity generated is then aggregated and sold to nearby consumers (typically commercial and industrial users) located within a 5km radius of the township ecosystem.

However, its rollout has been slower than initially expected, as the model faces operational and technical constraints.

Arjun Arasu, chief executive officer (CEO) of Time Energy Sdn Bhd, a unit of Time dotCom Bhd, points out that the access charges are a challenge for Cream.

Recall that, on the one hand, the government lowered the grid access charges for Cream participants, which on the face of it looked like it would boost take up.

However, the government then imposed additional charges on offtakers under the Regulatory Period 4 tariff structure, as part of a broader tariff reform aimed at strengthening cost recovery.

The net result is that total capacity and pass-through costs have risen to 33 sen per kWh from 15 sen previously.

This reflects a lower producer charge of nine sen per kWh (down from 15 sen per kWh), offset by a nine sen per kWh capacity charge and a 15 sen per kWh network charge payable by offtakers. The network charge did not exist under the previous tariff framework.

As a result, the economics of Cream projects may become less attractive. It is understood that the scheme is undergoing regulatory review to fine-tune it.

One early Cream project is Sime Darby Property Bhd’s Elmina development.

However, the potential to aggregate rooftop solar from more than 6,000 homes in Elmina has been scaled down to about 1,000 homes in the first phase, its group managing director and CEO Datuk Seri Azmir Merican tells StarBiz 7.

As with any emerging energy model, he says broader adoption at scale will require further evolution. “But we believe rooftop solar is one of the fastest and most practical pathways to accelerate RE adoption in Malaysia, and we are encouraged by the continued collaboration between industry and regulators to make community-based models more viable over time,” he says.

Time dotCom, through Time Energy, is also exploring Cream participation and is looking to leverage rooftops near AIMS’ Cyberjaya data centre for leased solar installations, with generated power aggregated and supplied to AIMS.

But how much is a rooftop worth when it becomes an energy asset for lease?

Industry players reckon rental income is likely to be “modest” as developers still need to recover capital investment, generate returns, and cover operations and maintenance over the system’s lifespan.

“After these costs, what remains for the homeowner is useful but not transformative for household finances,” says Sze. Some say the five-km radius requirement could narrow Cream’s participation due to a potential geographical mismatch between rooftops and offtakers.

They note that residential rooftops are largely concentrated in suburban townships, while commercial and industrial demand is centred in business parks, industrial estates and city centres, which are often outside the eligible radius.

Touching on this, Sim says MPSEA has highlighted the limitation and is proposing a shift from a blanket radius rule to a more flexible set of criteria.

In practice, some think Cream is likely to work best in townships near data centres, hospitals, hotels and large office complexes, which act as key demand anchors. They say it is also likely better suited to greenfield township developments, where rooftop aggregation, infrastructure and offtaker demand can be planned from the outset.

Even with Cream’s introduction, Sze believes the largest pool of untapped rooftop solar capacity lies with ordinary landed households, and that the most effective path to unlocking it remains the simpler self-consumption route, supported by the right policies and incentives.

“Countries that achieved mass residential solar adoption did so through sustained, simple incentives and access to financing.

“More sophisticated mechanisms such as virtual power plants and community energy schemes came later, built on a mature base,” Sze says.

He says the issue is no longer a lack of programmes. The challenge now lies in expanding participation through accessible financing, predictable incentives and policy stability.