1 Hot Industrial Stock Riding the AI Infrastructure Boom

Key Points

Comfort Systems USA's revenue and profit margins benefit from AI data center demand.

Growth in its modular systems drives margin expansion and efficiency.

Mechanical and electrical contracting services company Comfort Systems USA (NYSE: FIX) is a major winner from surging artificial intelligence (AI) data center investment. A high proportion of a data center's cost is in mechanical, electrical, and plumbing (MEP) systems, not least to ensure adequate cooling for heat-intensive IT racks. That's led to booming demand for the company's services and an incredible 1,160% return for investors over the last three years.

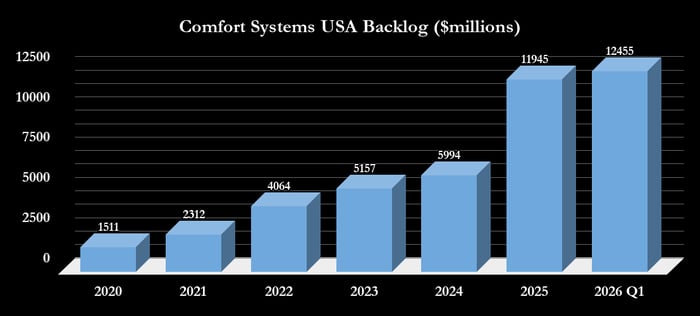

Comfort Systems revenue growth and margin expansion

The increase comes down to surging orders driving backlog and revenue growth, along with margin expansion. The growth in its backlog (shown below) leads to highly predictable revenue growth in the future.

Missed Nvidia in 2009? This Rare Signal Is Flashing Again. In 2009, a "Double Down" signal flashed for a little-known chipmaker called Nvidia. For the first time in years, that same "Total Conviction" signal is flashing for a company 1/100th the size of Nvidia. Continue »

Data source: Comfort Systems presentations. Chart by the author.

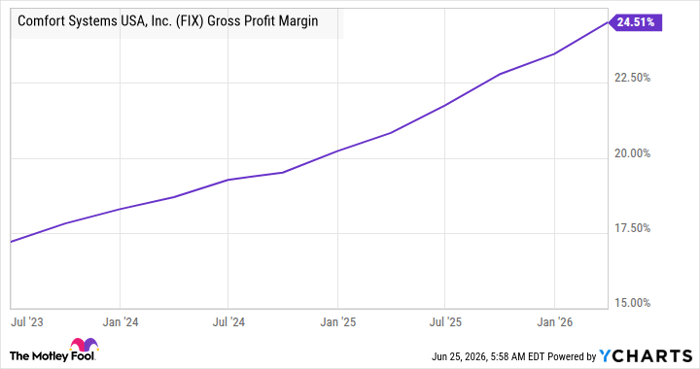

Permanent margin expansion?

Turning to the question of margin expansion, it comes from a combination of being able to selectively bid on complex and higher-margin AI data center projects, a natural leverage opportunity, as the marginal increase in revenue isn't accompanied by a significant increase in overhead costs, and the increase in its modular revenue, which represented 17% of its revenue in the first quarter of 2026.

Modular systems are manufactured at Comfort Systems locations (rather than onsite by tradespeople) and then transported and fitted onsite. It's a solution that confers several benefits for Comfort Systems and facility owners, such as optimizing MEP labor, improving quality control, and ensuring no disruption to the critical path of construction.

Although management doesn't break out modular revenue margins, it acknowledges its role as a contributor to the company's profit margin expansion in recent years. Moreover, management is expanding its modular capacity by 3 million square feet in 2025 to 4 million square feet by the end of 2026.

Data by YCharts.

Trading at 45 times expected 2026 earnings, the stock's valuation is arguably up with events. Still, if you think the AI data center spending boom is in its early innings, the momentum in orders and backlog growth could take the stock higher.

Lee Samaha has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Comfort Systems USA. The Motley Fool has a disclosure policy.