3 High Yield Dividend Stocks With Strong Cash Payouts and Balance Sheet Support

Global growth and inflation are moving at different speeds, services and manufacturing are pulling in opposite directions, and energy and food costs are sending mixed signals. In this kind of push and pull, many income investors are looking for ballast, not thrills. That is where the Dividend Fortresses screener comes in. It focuses on stocks with dividend yields above 5% that aim to combine robust cash payouts with balance sheet strength. In this article, three of the strongest candidates from the Dividend Fortresses list are highlighted, along with what makes each one stand out for dividend focused portfolios.

Halyk Bank of Kazakhstan (LSE:HSBK)

Overview: Halyk Bank of Kazakhstan is a universal bank headquartered in Almaty that offers a full suite of corporate, SME, retail and investment banking services across Kazakhstan, Kyrgyzstan, Georgia and Uzbekistan, from everyday accounts and cards to mortgages, business loans and trade finance.

Operations: The bank generates most of its revenue from Corporate Banking at KZT 751,429 million, followed by Investment Banking at KZT 329,650 million, SME Banking at KZT 194,145 million, Retail Banking at KZT 154,131 million and Unallocated activities at KZT 378,037 million. By geography, Kazakhstan contributes KZT 3,386,075 million of revenue, compared with KZT 97,563 million from OECD and KZT 108,933 million from Non OECD markets.

Market Cap: US$8.3b

For income investors, Halyk Bank of Kazakhstan brings together a low P/E multiple, high reported net profit margins around the mid 50% range and return on equity above 25%, all underpinned by sector leading positions in Kazakh retail, SME and corporate banking. At the same time, credit quality and provisioning need close attention, with bad loans at 8.3% and allowances covering only 60%, and earnings momentum in the latest quarter showing lower net income even as net interest income stayed solid. In addition, the bank combines a high dividend payout policy and active buybacks with higher regulatory burdens and a still concentrated footprint in Kazakhstan, giving dividend focused investors several factors to consider.

High margins, a low P/E and sector leading positions make Halyk Bank of Kazakhstan look stronger than many expect. However, the real story sits in how those strengths stack up against credit quality and capital pressures in the analysis report for Halyk Bank of Kazakhstan

Admiral Group (LSE:ADM)

Overview: Admiral Group is a Cardiff based financial services company that focuses on motor, home and other personal insurance, as well as personal lending, across the UK, France, Italy and Spain under brands such as Admiral, ConTe.it, L’olivier and Qualitas Auto.

Operations: Admiral Group generates most of its revenue from UK Insurance at £4.5b, alongside £656.7m from European Insurance, £25.8m from Admiral Money, £87.5m from Other activities and £17.7m from unallocated investment and interest income, partially offset by £1.1m of eliminations.

Market Cap: £11.2b

Admiral Group may appeal to income-focused investors because it combines a 5.59% dividend yield with insurance profitability supported by the use of data, machine learning and generative AI to manage costs and claims. The company’s growth profile is more nuanced, with revenue and earnings expectations described as relatively modest and a funding model that relies on external borrowing, which increases financial risk and contributes to a very high forecast ROE. Investors evaluating the balance between technology-driven efficiency, dividend commitments and a leveraged balance sheet may wish to look beyond headline figures in analyst forecasts and risk metrics.

Admiral Group’s high dividend and data driven insurance model could be masking a more complex story around funding, capital and future payouts, and the full 3 key rewards and 2 important warning signs (1 is major!) might reveal the twist most investors are missing

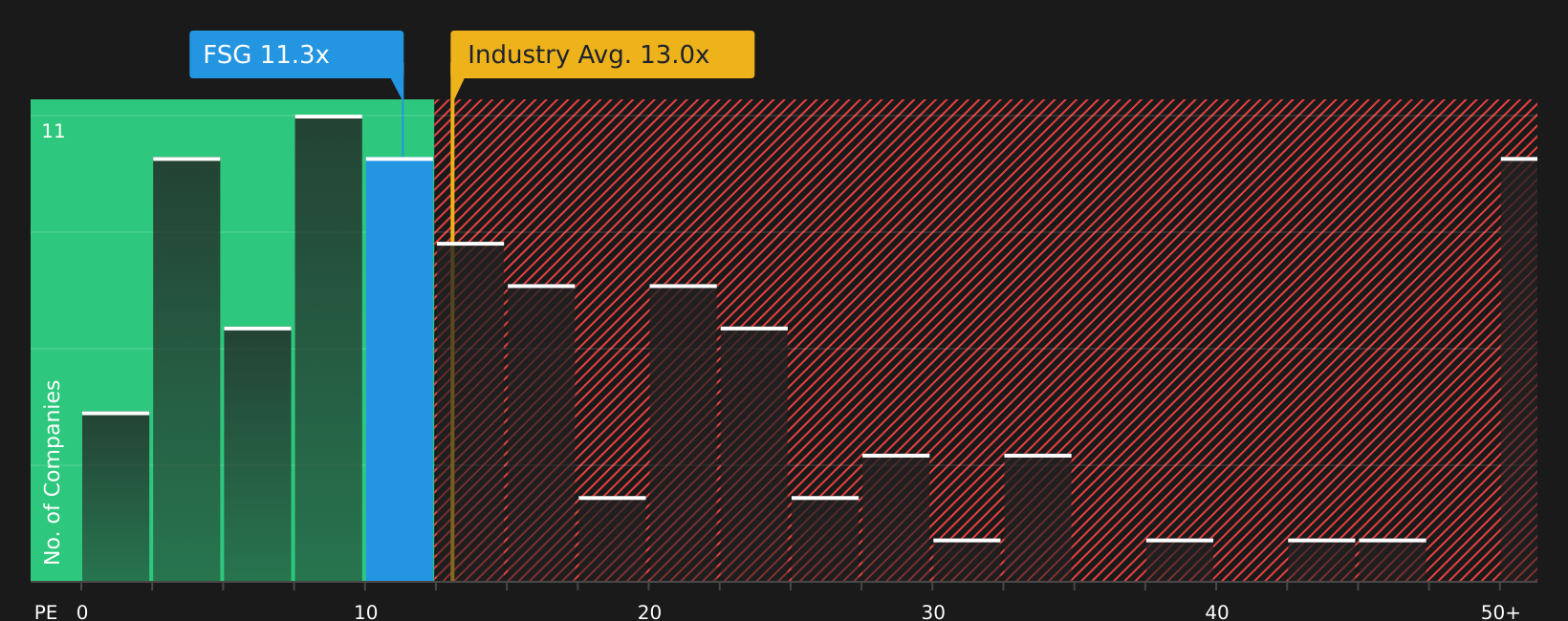

Foresight Group Holdings (LSE:FSG)

Overview: Foresight Group Holdings is a London based asset manager that runs infrastructure, private equity and venture capital funds, with a strong focus on renewable energy projects, real assets and smaller growth companies across the UK, Europe and Australia for both institutional and retail investors.

Operations: Foresight Group Holdings generates most of its revenue from Real Assets at £114.8m, alongside £50.1m from Private Equity, with activity spread mainly across the United Kingdom at £126.4m and Australia at £25.7m.

Market Cap: £513.7m

Foresight Group Holdings offers a mix of high quality, recurring fee income from long term infrastructure funds and exposure to energy transition themes, paired with a 60% dividend payout policy and ongoing share buybacks that support income focused investors. At the same time, the business leans on higher risk external borrowing, faces tighter ESG regulations and fee pressure from larger asset managers, and is expanding across several countries where policy shifts can affect fund flows. With earnings growing faster than its own 5 year average, a P/E below peers and analysts expecting higher future returns, the key consideration is how these factors may influence dividend strength and overall return outcomes over time.

Foresight Group Holdings already blends recurring infrastructure fees, energy transition exposure and a 60% payout policy. However, the biggest surprise may sit in how earnings and valuation line up in the analyst forecasts for Foresight Group Holdings

The three stocks covered here are just a starting point, and the full Dividend Fortresses screener has surfaced 0 more companies with equally compelling income focused stories that may not yet be on your radar, all captured inside the Dividend Fortresses screener. Identify the specific catalysts and dividend narratives that matter to you, and use Simply Wall St to filter, compare and analyze potential high conviction income ideas side by side.

Take Control of Your Investment Journey

If Foresight Group Holdings or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before The Crowd?

Fresh opportunities do not wait. While attention lingers on today’s dividend ideas, other themes may be building breakout momentum under the radar for now, so consider taking a closer look.

- Spot early movers in cash rich companies before the story is widely talked about by screening a curated list of solid balance sheet and fundamentals (19 results).

- Target resilient potential compounders by scanning a hand picked set of 8 resilient stocks with low risk scores designed to prioritize stability when markets feel restless.

- Explore structural trends in automation and productivity by reviewing carefully curated 30 robotics and automation stocks for ideas linked to real world adoption.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com