Peloton Interactive (PTON) On Strong Quarterly Results But Mixed Guidance And A Discount To Fair Value

Peloton Interactive (PTON) recently reported quarterly revenue of $630.9 million, which was ahead of analyst expectations, and exceeded adjusted operating income estimates, while its updated full-year EBITDA guidance fell short of forecasts.

See our latest analysis for Peloton Interactive.

Peloton Interactive’s better than expected quarterly results came after a period where the share price has been volatile, with a 90 day share price return of 25.55% but a 1 year total shareholder return that is down 13.40%. This suggests short term momentum has improved while longer term holders remain under water.

If you are rethinking your exposure after Peloton’s recent move, it can be useful to broaden your watchlist and look at 20 top founder-led companies

So with Peloton Interactive trading at a discount to analyst price targets and screens that suggest a large intrinsic discount, is the recent rebound an early entry point, or is the market already pricing in any future recovery?

Most Popular Narrative: 27% Undervalued

Peloton Interactive’s latest fair value narrative of $7.88 sits meaningfully above the last close at $5.75, which frames the current debate around the stock.

Peloton is leveraging advanced technologies, including AI-powered personalized coaching and human-driven community features, to broaden its offerings from cardio into holistic wellness (strength, sleep, stress, nutrition). This aligns with growing global health consciousness and may support future subscription revenue growth and higher engagement and churn reduction.

Want to see what this wellness push needs to deliver? The narrative rests on modest revenue gains, a sizeable margin lift, and a premium earnings multiple. The full set of assumptions is where the story gets interesting.

Result: Fair Value of $7.88 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Peloton Interactive still faces risks around softer hardware and subscription demand, as well as fiercer competition that could pressure pricing and delay any margin improvement investors are watching for.

Find out about the key risks to this Peloton Interactive narrative.

Another View on Peloton Interactive’s Valuation

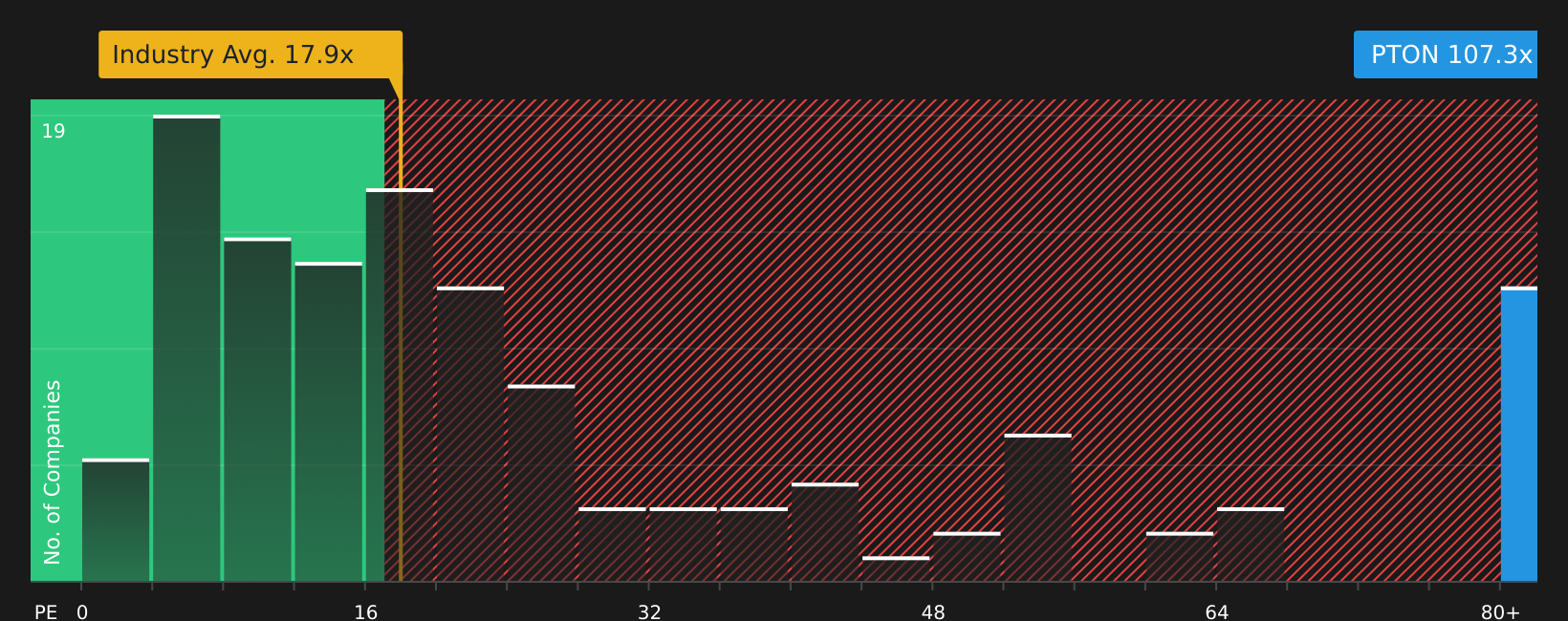

While the fair value narrative suggests Peloton Interactive is 27% undervalued at $7.88 per share, the current P/E of 107.3x tells a very different story. It is far above the Global Leisure industry at 17.5x, peers at 34.3x, and even the fair ratio of 30.9x. This points to considerable valuation risk if sentiment or growth expectations soften. Which signal do you trust more right now?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Conflicted about whether Peloton Interactive’s story leans more positive or negative right now? Take a closer look at both sides of the ledger with 3 key rewards and 3 important warning signs

Looking for more investment ideas beyond Peloton Interactive?

If Peloton Interactive has you reassessing your next move, do not stop here. Broaden your opportunity set with focused stock ideas built from clear, transparent data.

- Target dependable income by reviewing companies in the 7 dividend fortresses that may appeal if you want yields supported by robust fundamentals.

- Hunt for potential bargains by scanning the screener containing 18 high quality undiscovered gems that could sit off most radars yet still align with disciplined criteria.

- Prioritize resilience by zeroing in on the 75 resilient stocks with low risk scores so you are not the one who misses sturdier options when markets turn.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com