Wal Mart De México Stock and 2 Consumer Names Worth Watching On Lower Inflation

Mexico’s inflation rate easing to 3.37% and interest rates holding steady at 6.5% has shifted the backdrop for domestic stocks that rely on consumer demand. With price pressures closer to the central bank’s target range and no immediate push for higher borrowing costs, investors are reassessing which Mexican Consumer Discretionary stocks might be better positioned if confidence and spending stabilize. This article focuses on a selection from our Mexican Consumer Discretionary Stocks screener and reveals 3 stocks that appear positively exposed to the latest inflation and rate signals, helping you decide which opportunities may deserve a closer look.

Grupo Comercial Chedraui. de (BMV:CHDRAUI B)

Overview: Grupo Comercial Chedraui operates supermarket and self service store formats in Mexico and the United States, offering everything from fresh food and household essentials to electronics, fashion, pharmacy and real estate services, giving it broad exposure to everyday consumer spending.

Operations: The company generates its revenue from two main segments, Chedraui Mexico at MX$142.7b and Chedraui USA at MX$148.0b.

Market Cap: MX$86.4b

Grupo Comercial Chedraui is a large food and general merchandise retailer that could be influenced by easing inflation and steady rates as Mexican shoppers feel less pressure on household budgets. Analysts expect earnings to grow faster than the wider market, yet the stock trades below some estimates of fair value and carries a modest 2.56% dividend yield, which may appeal to income focused investors. At the same time, thin net margins around 2.3%, dependence on expansion in Mexico and the U.S., and a balance sheet funded entirely by external borrowing mean investors may wish to monitor profitability and funding costs closely. The full picture lies in how these growth plans, risks and valuation signals are weighed over the long term.

Grupo Comercial Chedraui’s mix of broad everyday spending exposure, thin margins and a fully externally funded balance sheet makes valuation signals especially important right now. It is therefore worth reviewing the DCF valuation analysis for Grupo Comercial Chedraui. de to see what the current share price might be missing.

Alsea. de (BMV:ALSEA *)

Overview: Alsea operates a wide portfolio of restaurant and coffee brands across Latin America and Europe, including Domino’s Pizza, Starbucks, Burger King, Chili’s and Vips, giving it broad exposure to everyday eating out and coffee habits in multiple markets.

Operations: Alsea generates most of its revenue from food and beverage operations in Mexico at MX$46.9b, followed by Europe at MX$26.1b and the rest of Latin America at MX$12.7b.

Market Cap: MX$35.6b

Alsea stands out in the Mexican Consumer Discretionary space because it links easing inflation and stable rates directly to how often people eat out and order in. The company has posted strong recent earnings growth, with a higher forecast growth rate than the wider market and a share price that sits below some estimates of fair value. At the same time, it carries elevated debt and interest coverage risk that could matter if conditions tighten again or traffic softens. With brands like Starbucks and Domino’s benefiting from digital ordering, loyalty programs and remodelled stores, investors watching Mexico’s inflation backdrop may want to consider how much of that potential, and how much of the funding risk, is already reflected in Alsea’s valuation and earnings profile.

Alsea’s growing global brands and digital ordering might be masking a crucial tension between earnings momentum and funding risk, so it is worth reading the 4 key rewards and 1 important major warning sign to see what could tip the balance next.

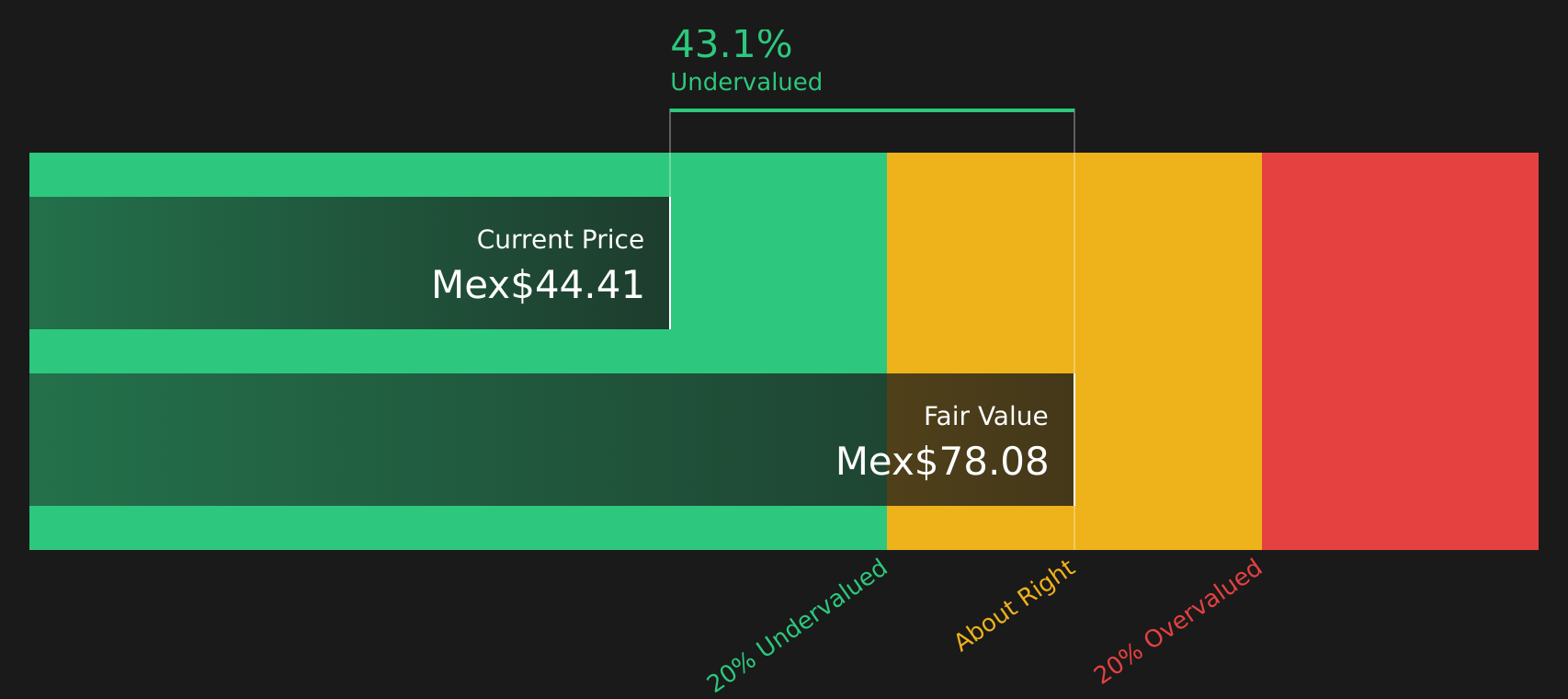

Wal-Mart de México. de (BMV:WALMEX *)

Overview: Wal-Mart de México operates a wide range of discount stores, supermarkets, hypermarkets and Sam’s Club wholesale outlets across Mexico and Central America, supplemented by digital wallet, telecom, financial and advertising services that tie customers more closely into its retail ecosystem.

Operations: The company generates most of its revenue in Mexico at MX$845.1b, with an additional MX$170.6b from Central America.

Market Cap: MX$856.4b

Wal-Mart de México provides direct exposure to Mexican consumer spending at a time when inflation is closer to target and interest rates are stable, which can help household budgets stretch further. Recent quarterly results show steady revenue and earnings, while management continues to invest in omnichannel retail, automation and private label to maintain its value proposition. At the same time, softer traffic in some regions, rising labor costs and heavy capital spending, alongside all liabilities being externally funded, mean profitability could come under pressure if conditions become less supportive. How these factors balance against analysts’ expectations and valuation assumptions is where the main opportunity or risk may lie for this retail company.

Wal-Mart de México’s scale, omnichannel push and externally funded balance sheet could be pulling in different directions for long term investors, so it is worth reading the analysis report for Wal-Mart de México. de to see what might be quietly shifting beneath the headline numbers

The three Mexican Consumer Discretionary stocks covered here are only a starting point, with the full Mexican Consumer Discretionary Stocks screener uncovering 5 more companies that share similarly compelling financial profiles and business narratives. Use Simply Wall St to identify and analyze the specific catalysts, financial health factors and growth narratives that matter most to you, so you can focus on the highest conviction ideas in this theme.

Take Control of Your Investment Journey

If Grupo Comercial Chedraui. de or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives For Your Curiosity?

New stock ideas can move from quiet to flying fast, and the cleanest entry points often vanish before the crowd notices. Scan fresh opportunities now and review them early.

- Identify companies where strong balance sheets and fundamentals may support resilient momentum by checking the curated list of solid balance sheet and fundamentals (419 results) before they are fully noticed by the crowd.

- Explore potential income and price momentum together as you review hand picked high yield opportunities inside the 471 dividend fortresses while payout stories may still be under the radar.

- Review the focused 34 power grid technology and infrastructure stocks to look for potential next steps in infrastructure-related ideas while they may still be appearing in only a few portfolios.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com