Does FTAI Aviation’s (FTAI) 737-800 Freighter Push Quietly Redefine Its Core Growth Engine?

- In early July 2026, FTAI Aviation Ltd. announced a collaboration with Aeronautical Engineers, Inc. to offer more cost-effective Boeing 737-800 freighter aircraft by combining FTAI’s CFM56 engine maintenance capabilities with AEI’s passenger-to-freighter conversion expertise for airline customers worldwide.

- This tie-up directly links FTAI’s legacy engine strength with the extensive 737-800 fleet, potentially deepening its role in the global freighter ecosystem.

- We’ll now explore how this 737-800 freighter collaboration with AEI could reshape FTAI Aviation’s investment narrative and growth balance.

Find 44 companies with promising cash flow potential yet trading below their fair value.

FTAI Aviation Investment Narrative Recap

To own FTAI Aviation, you need to believe its focus on mid life engines and capital light partnerships can keep generating attractive, recurring cash flows despite industry change. The new 737 800 freighter collaboration with AEI reinforces that engine centric thesis, but it does not remove the key short term risk that weaker flight activity or higher fuel costs could dampen engine service demand and undercut expectations for near term shop visit and parts volumes.

The AEI freighter deal also fits neatly alongside FTAI’s expanded US$2,025,000,000 revolving credit facility, which was upsized and extended to 2031 in April 2026. That added funding flexibility could matter if the company seeks to scale this 737 800 program or similar engine backed opportunities, but it equally magnifies the importance of managing balance sheet risk should engine demand or SCI style capital partnerships fall short of expectations.

Yet against this constructive story, investors should still weigh how concentrated exposure to legacy CFM56 engines could become a problem if...

Read the full narrative on FTAI Aviation (it's free!)

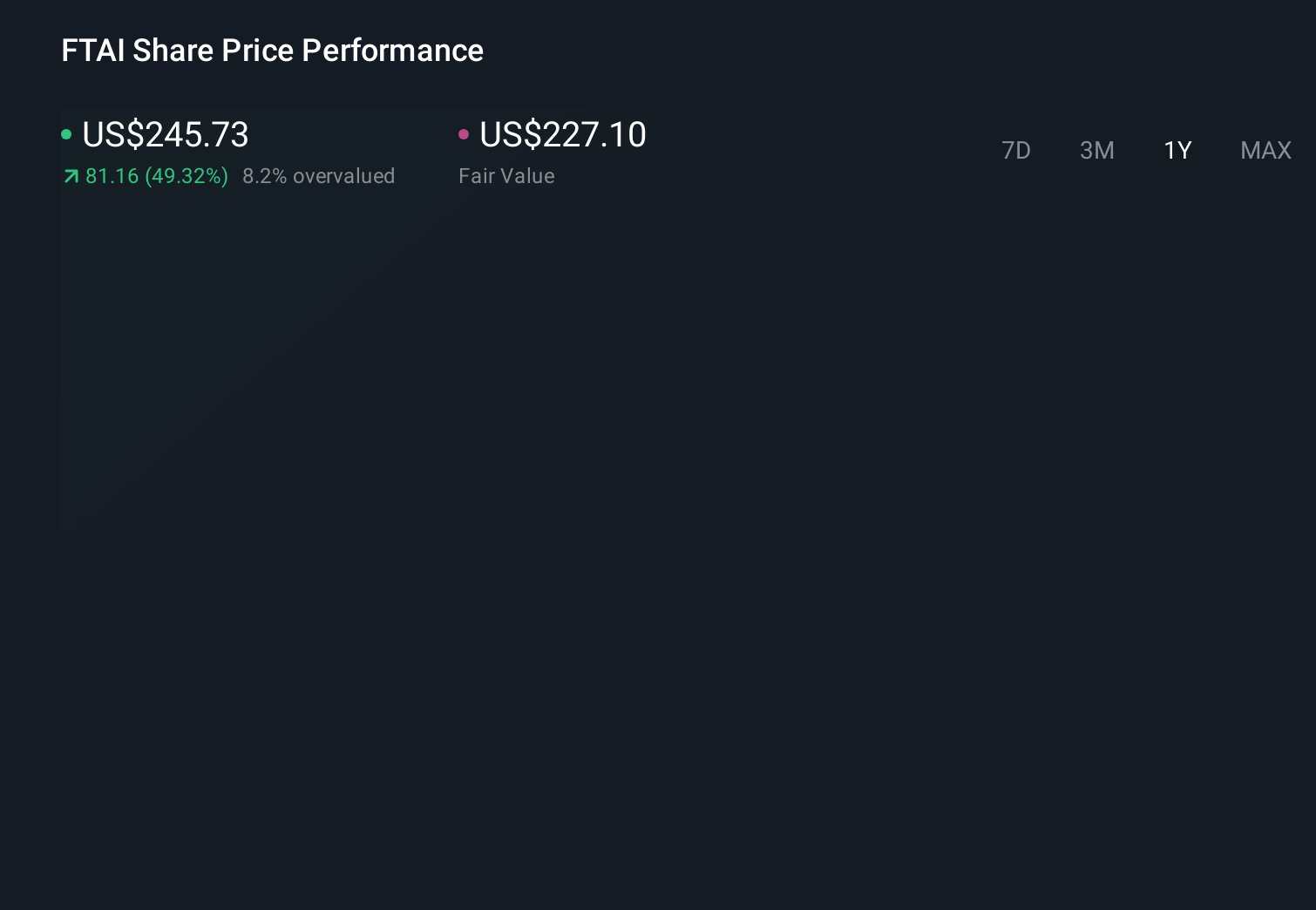

FTAI Aviation's narrative projects $6.6 billion revenue and $1.7 billion earnings by 2029.

Uncover how FTAI Aviation's forecasts yield a $350.60 fair value, a 54% upside to its current price.

Exploring Other Perspectives

While consensus treats the AEI deal as another incremental catalyst, the most optimistic analysts already expected revenue near US$8.9 billion and earnings of about US$2.6 billion by 2029, so you can see how their much bolder narrative around engine led growth and the chosen risk of OEM competition might shift meaningfully as this new freighter partnership plays out.

Explore 4 other fair value estimates on FTAI Aviation - why the stock might be worth just $319.00!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your FTAI Aviation research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free FTAI Aviation research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate FTAI Aviation's overall financial health at a glance.

Looking For Alternative Opportunities?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com