CSC Financial (SEHK:6066) Approves Final Dividend, Is The 8x P E Too Cheap?

Dividend approval puts upcoming dates in focus for CSC Financial

CSC Financial (SEHK:6066) has drawn fresh attention after approving a final dividend of CN¥1.75 per 10 shares for 2025, with ex dividend on 2 July 2026 and payment scheduled for 20 August 2026.

See our latest analysis for CSC Financial.

The dividend decision comes after a period where CSC Financial's share price return has been mixed in the short term, with a 10.44% 90 day share price return alongside a decline of 6.55% year to date, while longer term total shareholder returns of 16.88% over 1 year and 69.37% over 5 years point to momentum that has been stronger over time.

If you are weighing this dividend news against other opportunities in the market, it can help to see how different themes are trading right now, starting with 108 top founder-led companies

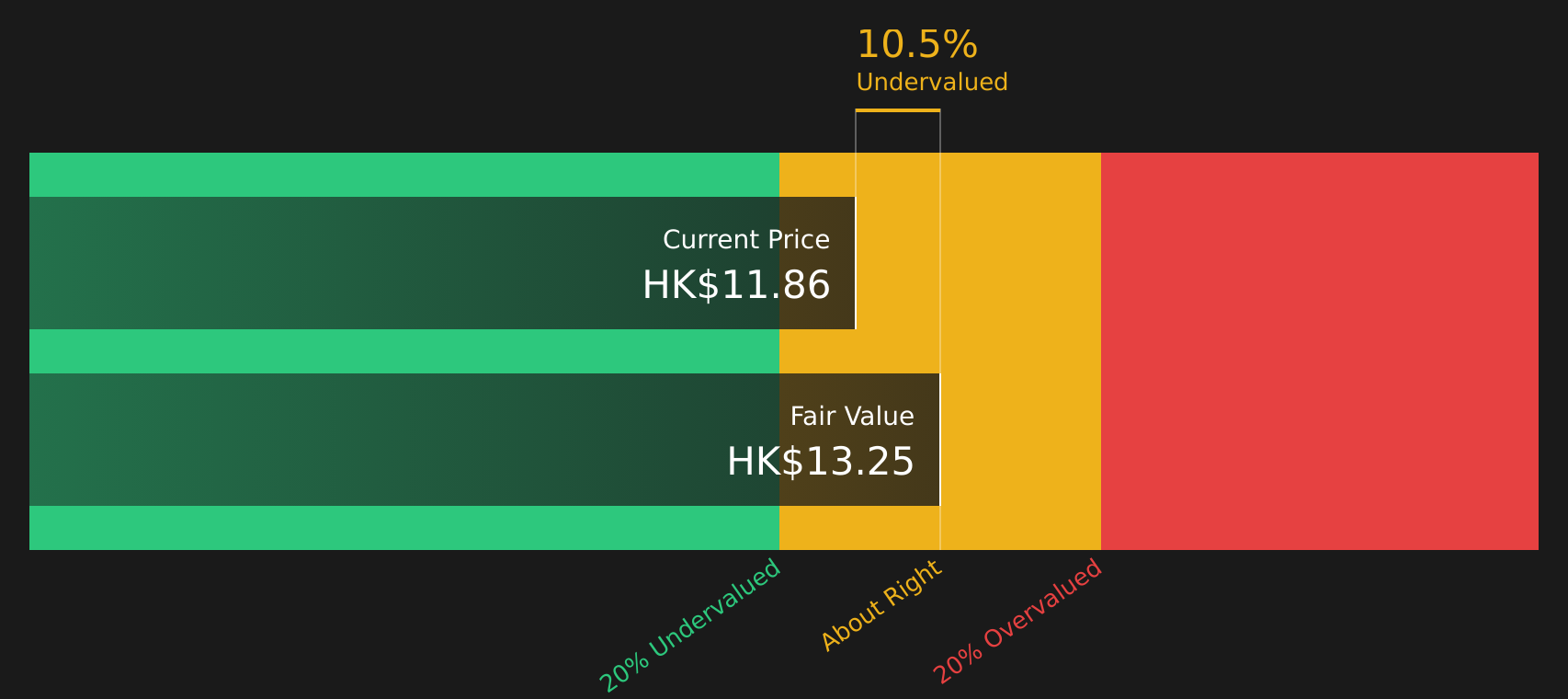

Bulls point to CSC Financial's recent dividend approval and long term shareholder returns, while bears question how much is already reflected in the HK$12.27 share price. So what does the current valuation really suggest?

Price to earnings of 8x for CSC Financial: Is it justified?

On the numbers available, CSC Financial appears undervalued on earnings, with the stock trading on a P/E of 8x while several benchmarks point to higher levels.

The P/E ratio compares the current share price to earnings per share and is a common way to see what the market is paying for current profits. For CSC Financial, the 8x P/E sits below the peer average of 9.2x and the Hong Kong Capital Markets industry average of 13.2x. It is also below the estimated fair P/E of 10.1x, which suggests the market is applying a relatively low earnings multiple.

Given that analysts expect earnings and revenue to grow each year, even if not at very high rates, a lower P/E can indicate the market is cautious about how durable that growth will be or about sector specific risks. At the same time, the stock is trading at 7.1% below one internal fair value estimate and at a discount to an estimated future cash flow value of HK$13.21 per share. This reinforces the picture of a market price that is not fully reflecting those earnings and cash flow projections.

Compared with the wider Hong Kong Capital Markets industry, where the average P/E is 13.2x, CSC Financial's 8x multiple is sharply lower. Even the peer group average of 9.2x sits meaningfully higher. The estimated fair P/E of 10.1x suggests a level the market could move towards if sentiment or expectations around earnings were to align more closely with these benchmarks.

Explore the SWS fair ratio for CSC Financial

Result: Price-to-earnings of 8x (UNDERVALUED).

However, the current CSC Financial story could be challenged if sector wide sentiment weakens, or if earnings trends behind that 8x P/E start to disappoint.

Find out about the key risks to this CSC Financial narrative.

Another view on CSC Financial: cash flows versus earnings

The P/E of 8x points to CSC Financial looking inexpensive on earnings, but our DCF model offers a different lens by focusing on estimated future cash flows. On that basis, the stock at HK$12.27 sits below an internal cash flow value estimate of HK$13.21, which also suggests undervaluation. The question is whether you put more weight on current earnings or on those projected cash flows.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out CSC Financial for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 213 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this CSC Financial story seems to balance both potential and risk, consider looking more closely at the details now so you can shape your own view with 4 key rewards and 1 important warning sign

Looking for more CSC Financial investment ideas?

If the CSC Financial valuation story has your attention, now is a good time to broaden your watchlist with a few focused screens tailored to different goals.

- Target potential bargains with solid fundamentals by scanning the market for companies trading below estimated value using the 213 high quality undervalued stocks.

- Prioritise stability and capital protection by reviewing companies that score strongly for resilience through the 292 resilient stocks with low risk scores.

- Stay ahead of the crowd by searching for quality businesses that are flying under most investors' radar via the screener containing 499 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com