ASX Penny Stocks To Watch In July 2026

The Australian stock market is experiencing a flat open, with modest movements not quite enough to propel the ASX 200 into positive territory, despite recoveries in the U.S. and Europe. Penny stocks, often associated with smaller or newer companies, continue to offer intriguing opportunities for investors seeking growth at lower price points. By focusing on those with strong financials and a clear growth trajectory, these stocks can present valuable prospects for those looking to explore this unique segment of the market.

We're going to check out a few of the best picks from our screener tool.

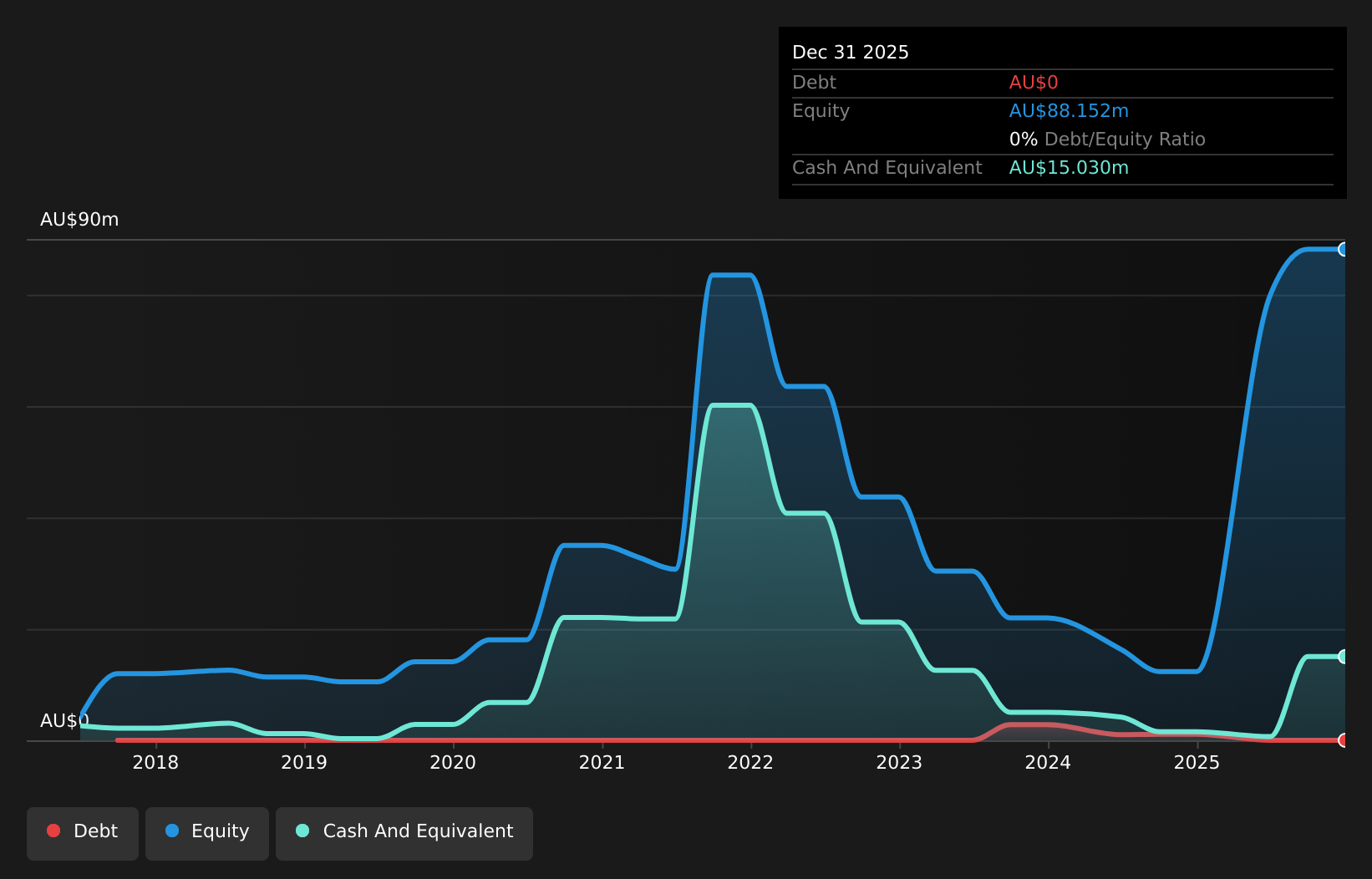

Blackstone Minerals (ASX:BSX)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Blackstone Minerals Limited is involved in the exploration of mineral properties in North America and Vietnam, with a market capitalization of A$72.38 million.

Operations: Blackstone Minerals Limited does not report any revenue segments.

Market Cap: A$72.38M

Blackstone Minerals Limited, with a market cap of A$72.38 million, is pre-revenue and unprofitable. The company has reduced its losses by 8.6% annually over the past five years, indicating some progress towards profitability. It benefits from being debt-free and having short-term assets (A$18.7M) that exceed both its short-term (A$1.5M) and long-term liabilities (A$184.1K). However, it faces challenges with high share price volatility and an inexperienced board averaging 0.6 years in tenure. Blackstone has a cash runway exceeding one year if current free cash flow trends persist without significant shareholder dilution recently observed.

- Unlock comprehensive insights into our analysis of Blackstone Minerals stock in this financial health report.

- Assess Blackstone Minerals' previous results with our detailed historical performance reports.

GWA Group (ASX:GWA)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: GWA Group Limited is involved in the research, design, manufacture, importation, and marketing of building fixtures and fittings for residential and commercial properties across Australia, New Zealand, the United Kingdom, and internationally with a market cap of A$603.08 million.

Operations: The company generates revenue primarily through its Water Solutions segment, which reported A$422.68 million.

Market Cap: A$603.08M

GWA Group, with a market cap of A$603.08 million, is not pre-revenue and shows promising financial metrics despite some challenges. Its net debt to equity ratio is satisfactory at 32%, and earnings grew by 26% last year, outpacing the industry average. The company trades at a significant discount to its estimated fair value, offering potential investment appeal. However, its dividend yield of 6.6% isn't well covered by earnings, indicating potential sustainability issues. Recent board changes include John Mulcahy's retirement as part of ongoing renewal efforts aimed at balancing director tenure diversity within the company’s leadership structure.

- Click here and access our complete financial health analysis report to understand the dynamics of GWA Group.

- Assess GWA Group's future earnings estimates with our detailed growth reports.

Qualitas (ASX:QAL)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Qualitas is a real estate investment firm that engages in direct investments across various real estate classes and geographies, distressed debt acquisitions and restructuring, third-party capital raisings, and consulting services, with a market cap of A$932.23 million.

Operations: The company generates revenue from two primary segments: Direct Lending, which accounts for A$0.46 million, and Funds Management, contributing A$31.53 million.

Market Cap: A$932.23M

Qualitas, with a market cap of A$932.23 million, is not pre-revenue and has shown strong financial performance despite some concerns. Its earnings grew by 26.7% over the past year, surpassing industry averages, and its short-term assets comfortably cover both short-term and long-term liabilities. The company’s debt to equity ratio has significantly improved over five years, though operating cash flow remains negative. Trading below analyst price targets suggests potential for appreciation; however, the dividend yield of 3.17% isn't well covered by free cash flows. Recent initiatives include launching a real estate private credit platform in Europe and AI updates.

- Dive into the specifics of Qualitas here with our thorough balance sheet health report.

- Review our growth performance report to gain insights into Qualitas' future.

Summing It All Up

- Discover the full array of 405 ASX Penny Stocks right here.

- Searching for a Fresh Perspective? Trump's oil boom is here — pipelines are primed to profit. Discover the 23 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com