Yum! Brands (YUM) Faces A Valuation Test After Taco Bell Produce Pullback

Yum! Brands (YUM) is under scrutiny after its Taco Bell division pulled several fresh produce ingredients as U.S. health officials investigate a Cyclospora outbreak linked to nearly 2,000 reported illnesses nationwide.

See our latest analysis for Yum! Brands.

Despite the Taco Bell setback, Yum! Brands’ recent share price performance has been relatively resilient. The share price is $162.39 after a 30-day share price return of 7.10% and a 1-year total shareholder return of 8.64%, which hints at steady but not explosive momentum.

If this health scare has you thinking more broadly about consumer and supply chain risks, it could be a good time to broaden your search and check out 18 top founder-led companies

Bulls point to Yum! Brands’ recent 7.10% 30 day share price gain and solid 1 year total return, while bears highlight Taco Bell’s Cyclospora risk and reputation overhang. Do current valuation markers really support the optimistic camp?

Most Popular Narrative: 6.5% Undervalued

Compared with the current Yum! Brands share price of $162.39, the most followed fair value narrative of about $173.71 points to a modest valuation gap that hinges on how future earnings and margins play out under a 9.25% discount rate.

The rapid acceleration and global rollout of Yum!'s Byte digital platform, including AI-driven marketing, operational automation, and proprietary ordering/delivery solutions, positions the company to capture higher transaction volumes, expand check sizes, and enhance customer loyalty, driving both top-line revenue growth and improving net margins over the long term.

Want to see what sits behind that premium on Yum! Brands future cash flows? The narrative leans heavily on sustained revenue progress, firmer margins and a richer earnings multiple baked into that fair value.

Result: Fair Value of $173.71 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this Yum! Brands narrative could be knocked off course if international exposure amplifies currency or geopolitical shocks, or if digital and AI investments fail to earn back their upfront cost.

Find out about the key risks to this Yum! Brands narrative.

Another View on Yum! Brands Valuation

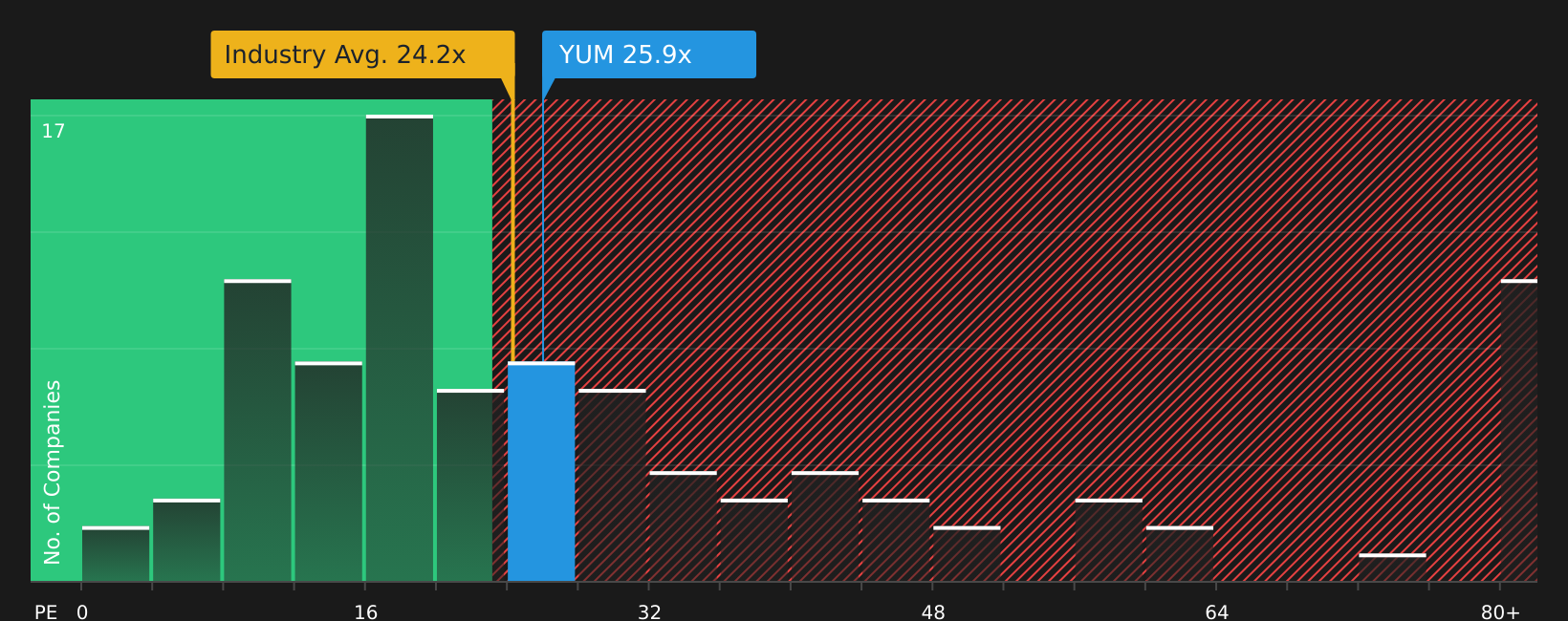

The fair value narrative for Yum! Brands leans on future earnings and a projected P/E of about 28x. On today’s numbers, the stock trades on a P/E of 25.8x, which is higher than the US Hospitality industry at 23.5x and slightly above a fair ratio of 25.3x, while still below a peer average of 41.1x. That mix of richer pricing than the sector, but cheaper than peers, raises a simple question: is the current valuation leaving much room for error if the growth narrative softens?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With mixed signals on Yum! Brands valuation and narrative, do you want to rely solely on sentiment, or test the thesis yourself quickly and independently by reviewing the 3 key rewards and 4 important warning signs?

Looking for more investment ideas beyond Yum! Brands?

If you are weighing what Taco Bell’s news means for Yum! Brands, it makes sense to compare it with other opportunities and see where your capital could work harder.

- Target potential bargains on quality by reviewing companies in the 44 high quality undervalued stocks that combine appealing pricing with fundamentals screened by Simply Wall Street.

- Prioritise resilience by assessing companies in the 73 resilient stocks with low risk scores that score well on factors aimed at reducing the chance of major downside surprises.

- Hunt for underfollowed opportunities by scanning the screener containing 19 high quality undiscovered gems where strong fundamentals have not yet attracted widespread attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com