Williams Sonoma (WSM) Stock May Be 18% Undervalued As Cash Flow Holds Up

Williams-Sonoma has delivered a very strong share price run over the past three years, yet its valuation signals are split, with a Discounted Cash Flow (DCF) intrinsic value estimate pointing to meaningful upside while earnings based multiples suggest the stock already trades at a premium.

- Over the past three years, Williams-Sonoma has returned about 256.3%, which puts extra focus on whether current buyers are paying too much for that track record.

- Expectations that the company can keep converting its brand strength into consistent cash generation may support the current price, while any pressure on margins or consumer demand would quickly test how much investors are willing to pay for those cash flows.

- On Simply Wall St's broader checks, Williams-Sonoma scores 1 out of 6 for value, which leans more expensive overall even though the DCF suggests the shares trade around 18.2% below intrinsic value.

The issue now is whether the DCF style upside or the richer market multiples offer the more reliable guide to what Williams-Sonoma stock is worth today.

Does Williams-Sonoma Look Undervalued on Cash Flow?

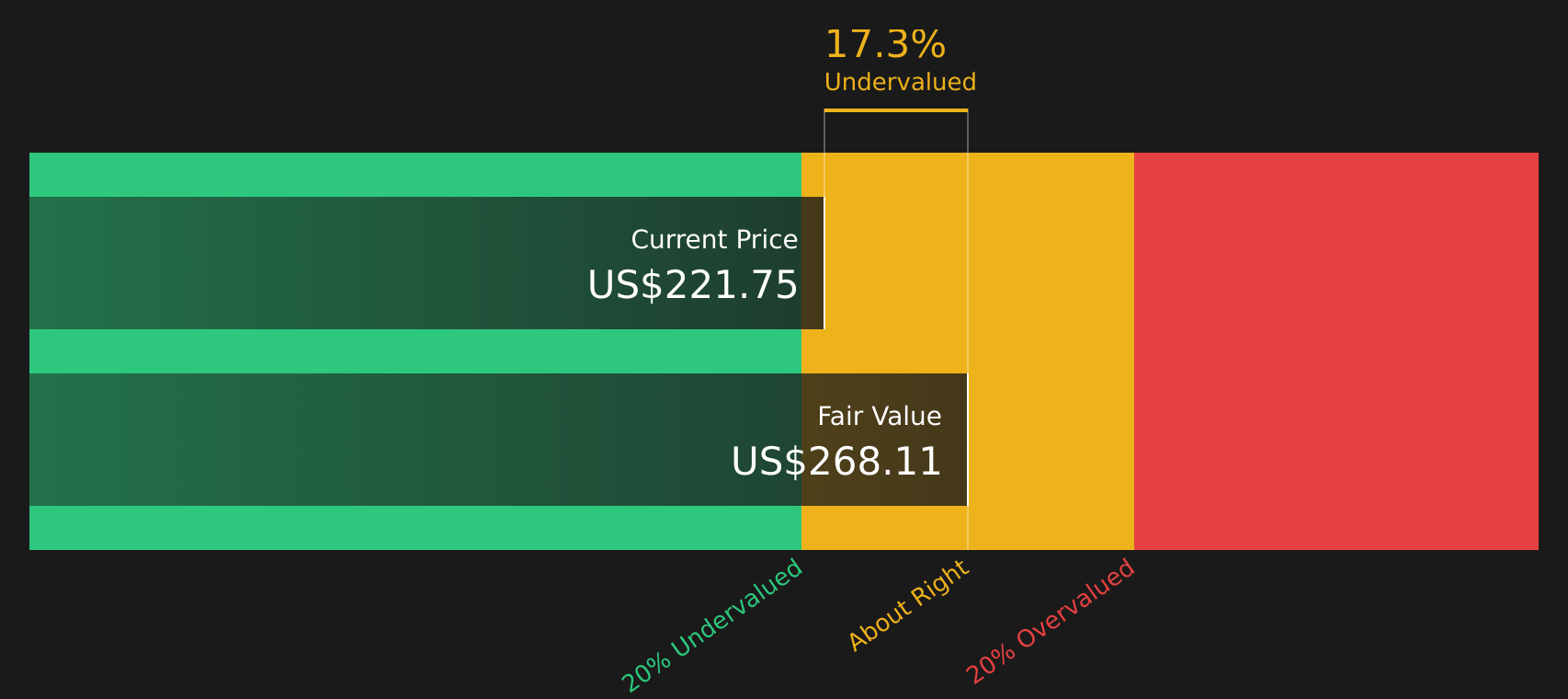

The Discounted Cash Flow (DCF) model values Williams-Sonoma by projecting the cash it can return to shareholders in the future and discounting that back to today. On the latest twelve month numbers, the company is generating about $1.12b in free cash flow, and the model applies a growing but moderating cash flow profile over time rather than assuming an aggressive surge.

On that basis, the 2 Stage Free Cash Flow to Equity model points to an estimated intrinsic value of about $269 per share, which is roughly 18.2% above the current share price implied by this analysis. That gap suggests the cash flow outlook supports a higher value than the market is currently assigning to Williams-Sonoma, even after a strong share price performance in recent years.

Overall, the Discounted Cash Flow (DCF) workup indicates Williams-Sonoma stock screens as undervalued relative to its projected cash generation.

Our Discounted Cash Flow (DCF) analysis suggests Williams-Sonoma is undervalued by 18.2%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Has Williams-Sonoma Run Too Far on Earnings?

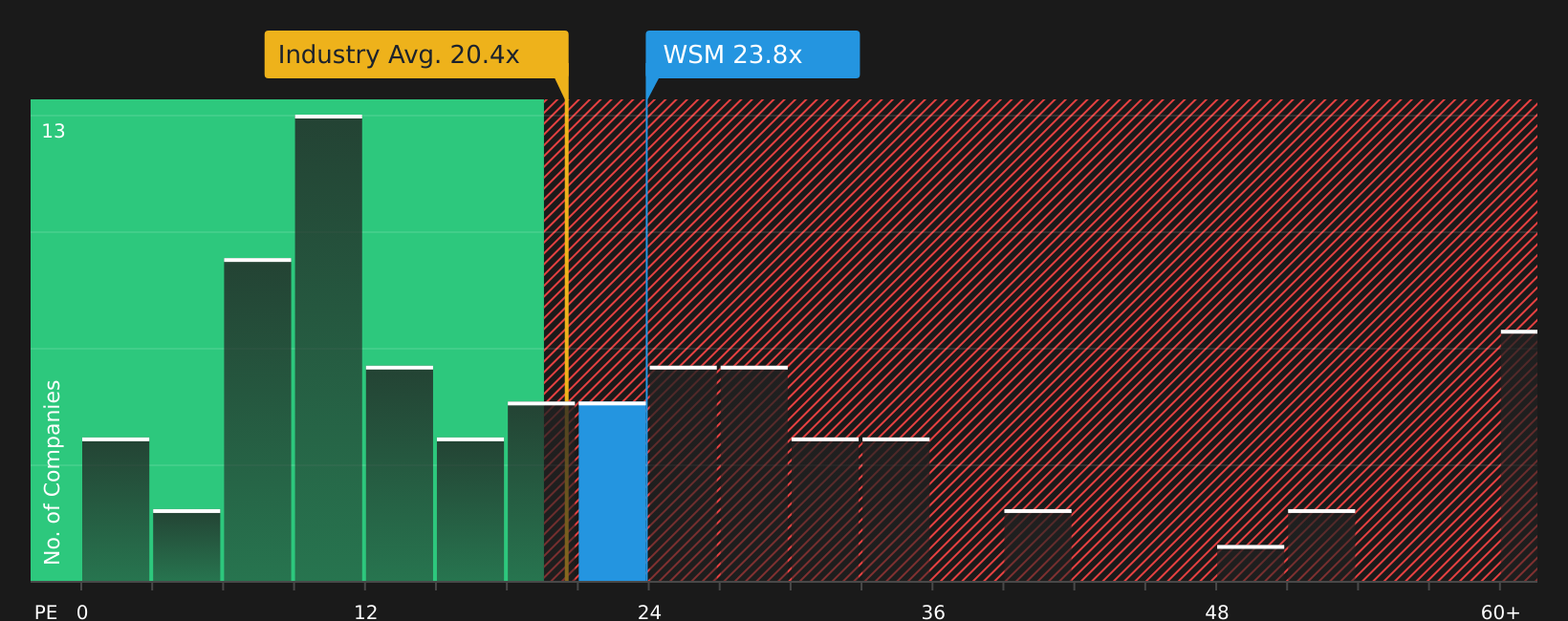

The P/E multiple suits Williams-Sonoma because earnings are a core focus for many investors in established retailers. The stock currently trades on a P/E of about 23.8x, compared with a Specialty Retail industry average of roughly 19.9x and a peer average around 20.7x, so the market is asking investors to pay more per dollar of earnings than for many comparable companies.

A fair P/E ratio for Williams-Sonoma, based on factors such as its sector, profitability profile, size and risk, is estimated at about 16.3x, which is well below the current 23.8x level. That gap indicates investors are assigning a premium to the stock that is not reflected in this fair multiple estimate and leaves limited room for disappointment if sentiment cools.

On the P/E yardstick, Williams-Sonoma stock currently appears overvalued compared with both tailored fair value estimates and its wider Specialty Retail peer group.

See what the numbers say about this price — find out in our valuation breakdown.

The Williams-Sonoma Narrative: What Would Justify Today's Price?

Simply Wall St Narratives aim to close the gap between Williams-Sonoma's mixed valuation signals and the story the market is really pricing in by spelling out which paths for revenue, margins and earnings would justify a meaningfully higher or lower share price from here. They sit on the company’s Community page. Each narrative ties a reasonable fair value estimate to a specific set of potential catalysts and risks, so you can track over time which version of Williams-Sonoma's story appears to be taking shape.

Community views on Williams-Sonoma sit far apart, with one camp seeing solid room for upside and another concerned about premium pricing and macro risks.

Bull case: 15% undervalued

"Continued expansion and innovation of exclusive, in-house brands such as Pottery Barn, West Elm, and an emerging billion-dollar brand in Rejuvenation enhance pricing power, brand loyalty, and reduce dependency on third-party vendors..."

Read the full Bull Case to see why Williams-Sonoma could be undervalued

Bear case: 6% overvalued

"Tariff volatility, weak housing demand, and shifting consumer preferences create significant risks to margins, revenue growth, and supply chain stability for Williams-Sonoma..."

Read the full Bear Case to see why Williams-Sonoma could be overvalued

Do you think there's more to the story for Williams-Sonoma? Head over to our Community to see what others are saying!

The Bottom Line

Williams-Sonoma sits in a genuine valuation tug of war, with the Discounted Cash Flow (DCF) intrinsic value estimate suggesting upside while earnings-based multiples flag the stock as overvalued. That split reflects two different focal points: cash generation capacity on one side and current market expectations and peer pricing on the other. Broader checks still point to a weak overall value profile despite the DCF support. For you, the key question is whether Williams-Sonoma can keep turning its brand strength into resilient cash flow without slipping on margins or demand, which would decide whether today’s apparent discount is an opportunity or simply compensation for those risks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com