Asian Growth Companies With High Insider Ownership To Watch

As global markets experience mixed performances, with notable shifts in sectors and indices, Asia remains a focal point for investors seeking growth opportunities amid evolving economic conditions. In this environment, companies with high insider ownership often attract attention due to the potential alignment of interests between management and shareholders, making them intriguing prospects in the region's diverse market landscape.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| Suzhou Dongshan Precision Manufacturing (SZSE:002384) | 33.5% | 73.1% |

| SEERS (KOSDAQ:A458870) | 33.2% | 41.5% |

| Meitu (SEHK:1357) | 22.8% | 31.4% |

| Meiko Electronics (TSE:6787) | 19.2% | 27.6% |

| L&C BIOLTD (KOSDAQ:A290650) | 24% | 148.5% |

| Jiangxi Fushine Pharmaceutical (SZSE:300497) | 21.1% | 55.9% |

| Guangzhou Tinci Materials Technology (SZSE:002709) | 38.4% | 28.9% |

| Great Microwave Technology (SHSE:688270) | 29.5% | 85.5% |

| Gold Circuit Electronics (TWSE:2368) | 30.1% | 38.2% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 14.1% | 40.4% |

Let's explore several standout options from the results in the screener.

Busy Ming Group (SEHK:1768)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Busy Ming Group Co., Ltd. operates as a food and beverage retailer in China with a market cap of HK$79.67 billion.

Operations: The company generates revenue primarily from its grocery store segment, totaling CN¥66.17 billion.

Insider Ownership: 29.5%

Revenue Growth Forecast: 17.8% p.a.

Busy Ming Group, recently added to the S&P Global BMI Index, is trading at 37.2% below its estimated fair value and shows promising growth potential with earnings forecasted to grow significantly by 24.73% annually over the next three years. This growth rate surpasses both the Hong Kong market's average and Busy Ming's revenue growth of 17.8%. Despite no recent insider trading activity, high insider ownership aligns interests with shareholders effectively.

- Click to explore a detailed breakdown of our findings in Busy Ming Group's earnings growth report.

- Upon reviewing our latest valuation report, Busy Ming Group's share price might be too pessimistic.

Jiangsu Eazytec (SHSE:688258)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Jiangsu Eazytec Co., Ltd. specializes in cloud computing equipment core firmware products both in China and internationally, with a market capitalization of CN¥16.42 billion.

Operations: Jiangsu Eazytec generates its revenue primarily from the sale of core firmware products for cloud computing equipment in both domestic and international markets.

Insider Ownership: 37.9%

Revenue Growth Forecast: 50.5% p.a.

Jiangsu Eazytec demonstrates robust growth potential with earnings and revenue forecasted to grow significantly at 49.1% and 50.5% annually, outpacing the broader Chinese market. The company reported a substantial increase in net income for Q1 2026, driven by large one-off items impacting results. Despite recent share price volatility, high insider ownership suggests aligned interests with shareholders. A private placement aims to raise CNY 300 million, reflecting strategic expansion efforts without recent insider trading activity.

- Take a closer look at Jiangsu Eazytec's potential here in our earnings growth report.

- Our expertly prepared valuation report Jiangsu Eazytec implies its share price may be too high.

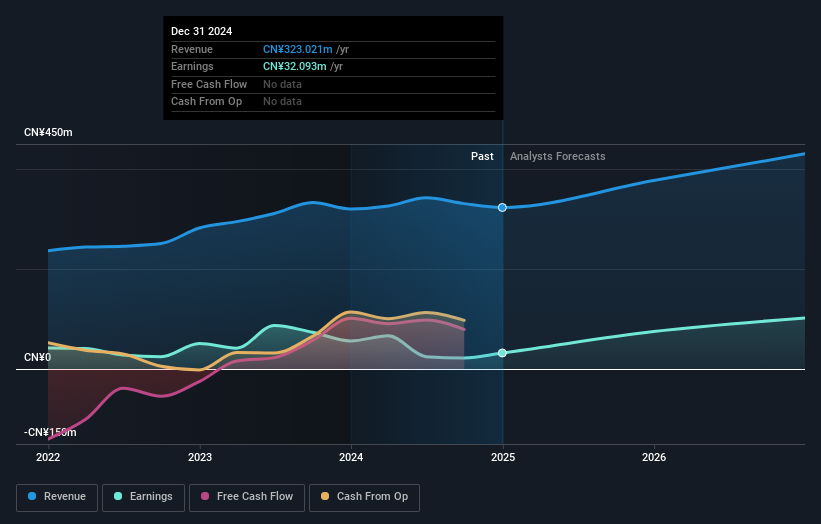

Great Microwave Technology (SHSE:688270)

Simply Wall St Growth Rating: ★★★★★★

Overview: Great Microwave Technology Co., Ltd. focuses on the research, development, production, and sale of integrated circuit chips and microsystems in China with a market cap of CN¥27.53 billion.

Operations: The company generates revenue from the research, development, production, and sale of integrated circuit chips and microsystems in China.

Insider Ownership: 29.5%

Revenue Growth Forecast: 78% p.a.

Great Microwave Technology shows strong growth prospects, with revenue and earnings expected to grow significantly faster than the Chinese market. Recent Q1 results revealed a notable rise in net income to CNY 39.58 million, supported by a substantial increase in sales. Despite being dropped from the S&P Global BMI Index and experiencing share price volatility, the company's high insider ownership aligns management interests with shareholders, indicating confidence in its strategic direction amid no recent insider trading activity.

- Dive into the specifics of Great Microwave Technology here with our thorough growth forecast report.

- Our comprehensive valuation report raises the possibility that Great Microwave Technology is priced higher than what may be justified by its financials.

Seize The Opportunity

- Click here to access our complete index of 478 Fast Growing Asian Companies With High Insider Ownership.

- Curious About Other Options? This technology could replace computers: discover the 26 stocks are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com