Asian Market Insights: 3 Stocks Like Shenzhen Kinwong Electronic That May Be Underestimated

As global markets navigate mixed signals, with Japan experiencing a divergence in stock performance and China's manufacturing showing resilience, investors are increasingly looking toward Asia for opportunities that may be underestimated. In such an environment, identifying undervalued stocks involves assessing companies with strong fundamentals that might not yet be fully appreciated by the market, offering potential for growth as conditions evolve.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Zhongji Innolight (SZSE:300308) | CN¥1194.90 | CN¥2338.95 | 48.9% |

| Shenzhen Yanmade Technology (SHSE:688312) | CN¥66.20 | CN¥132.37 | 50% |

| Rakus (TSE:3923) | ¥1029.00 | ¥2011.31 | 48.8% |

| NC Chem (KOSDAQ:A482630) | ₩13040.00 | ₩25754.36 | 49.4% |

| Matrix Design (SZSE:301365) | CN¥36.86 | CN¥72.78 | 49.4% |

| Laopu Gold (SEHK:6181) | HK$383.00 | HK$746.24 | 48.7% |

| Kunshan Dongwei TechnologyLtd (SHSE:688700) | CN¥76.11 | CN¥148.50 | 48.7% |

| Contec.Co.Ltd (KOSDAQ:A451760) | ₩8100.00 | ₩16175.23 | 49.9% |

| APT Medical (SHSE:688617) | CN¥197.35 | CN¥388.60 | 49.2% |

| Addvalue Technologies (SGX:A31) | SGD0.133 | SGD0.26 | 48.9% |

Let's explore several standout options from the results in the screener.

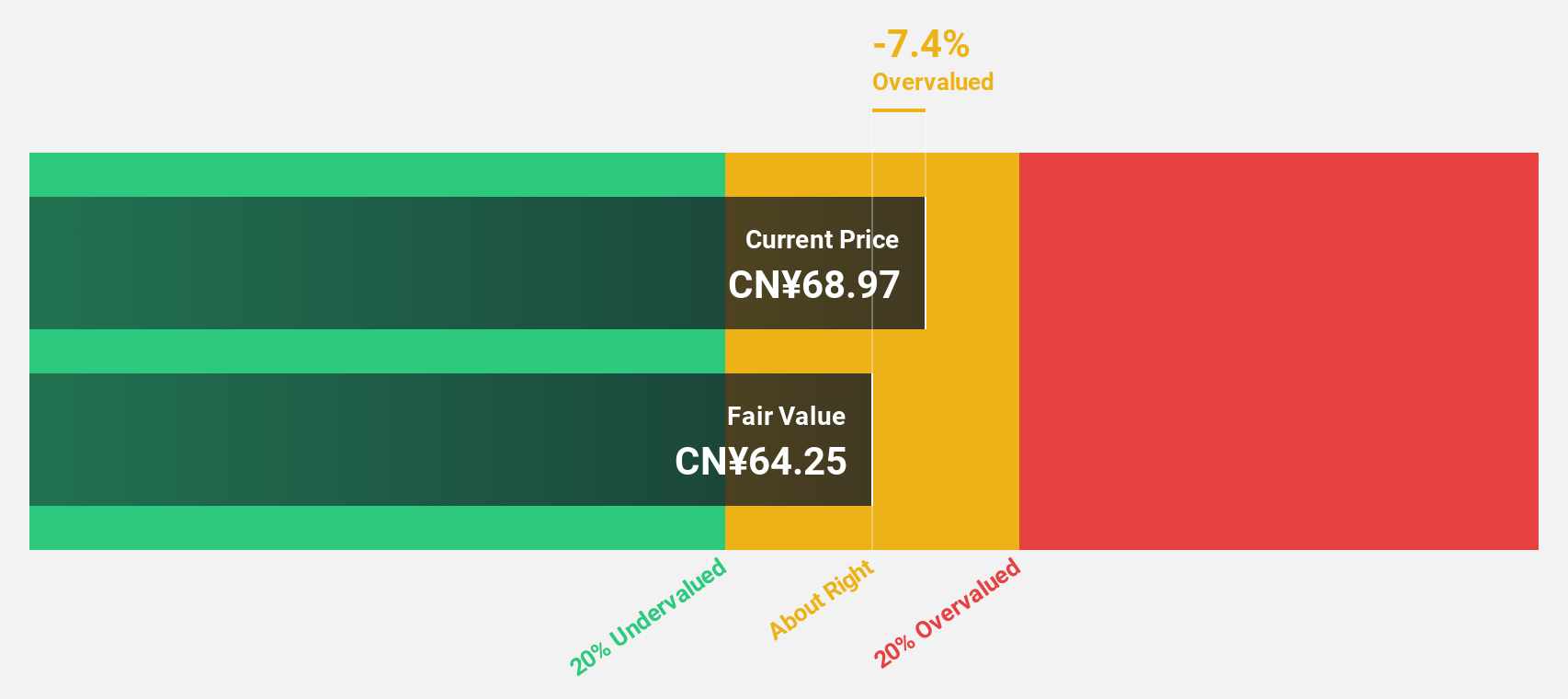

Shenzhen Kinwong Electronic (SHSE:603228)

Overview: Shenzhen Kinwong Electronic Co., Ltd. is involved in the research, development, production, and sale of printed circuit boards and electronic materials both in China and internationally, with a market cap of CN¥67.32 billion.

Operations: The company's revenue primarily comes from its Printed Circuit Board segment, which generated CN¥15.86 billion.

Estimated Discount To Fair Value: 45.8%

Shenzhen Kinwong Electronic is trading at CN¥68.25, significantly below its estimated cash flow value of CN¥125.91, indicating it may be undervalued based on cash flows. Despite recent volatility in its share price and a dividend not well covered by free cash flows, the company's earnings are forecast to grow 48.1% annually over the next three years, outpacing both industry peers and the broader Chinese market's growth expectations.

- The analysis detailed in our Shenzhen Kinwong Electronic growth report hints at robust future financial performance.

- Dive into the specifics of Shenzhen Kinwong Electronic here with our thorough financial health report.

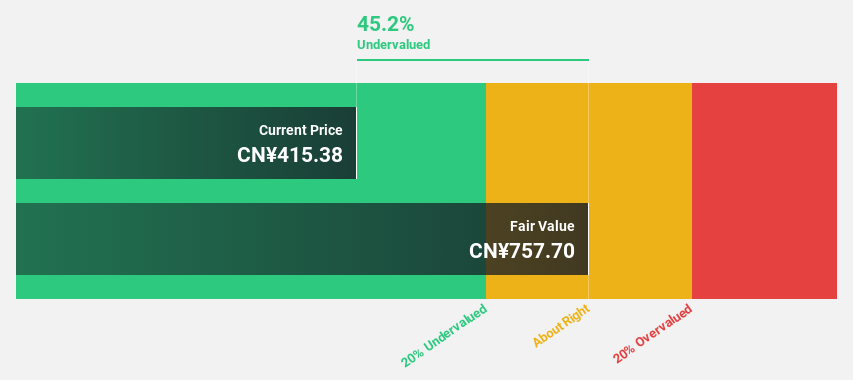

APT Medical (SHSE:688617)

Overview: APT Medical Inc. focuses on the research, development, production, and sale of cardiovascular interventional medical devices in China with a market cap of CN¥27.85 billion.

Operations: The company generates revenue from its medical products segment, which amounted to CN¥2.72 billion.

Estimated Discount To Fair Value: 49.2%

APT Medical is trading at CN¥197.35, significantly below its estimated cash flow value of CN¥388.6, highlighting potential undervaluation based on cash flows. The company recently completed a share buyback program worth CNY 99.98 million, enhancing shareholder value. Despite an unstable dividend history and earnings growth forecasted to be slower than the Chinese market average, APT Medical's revenue is expected to grow faster than the market at 22.3% annually.

- Our expertly prepared growth report on APT Medical implies its future financial outlook may be stronger than recent results.

- Click to explore a detailed breakdown of our findings in APT Medical's balance sheet health report.

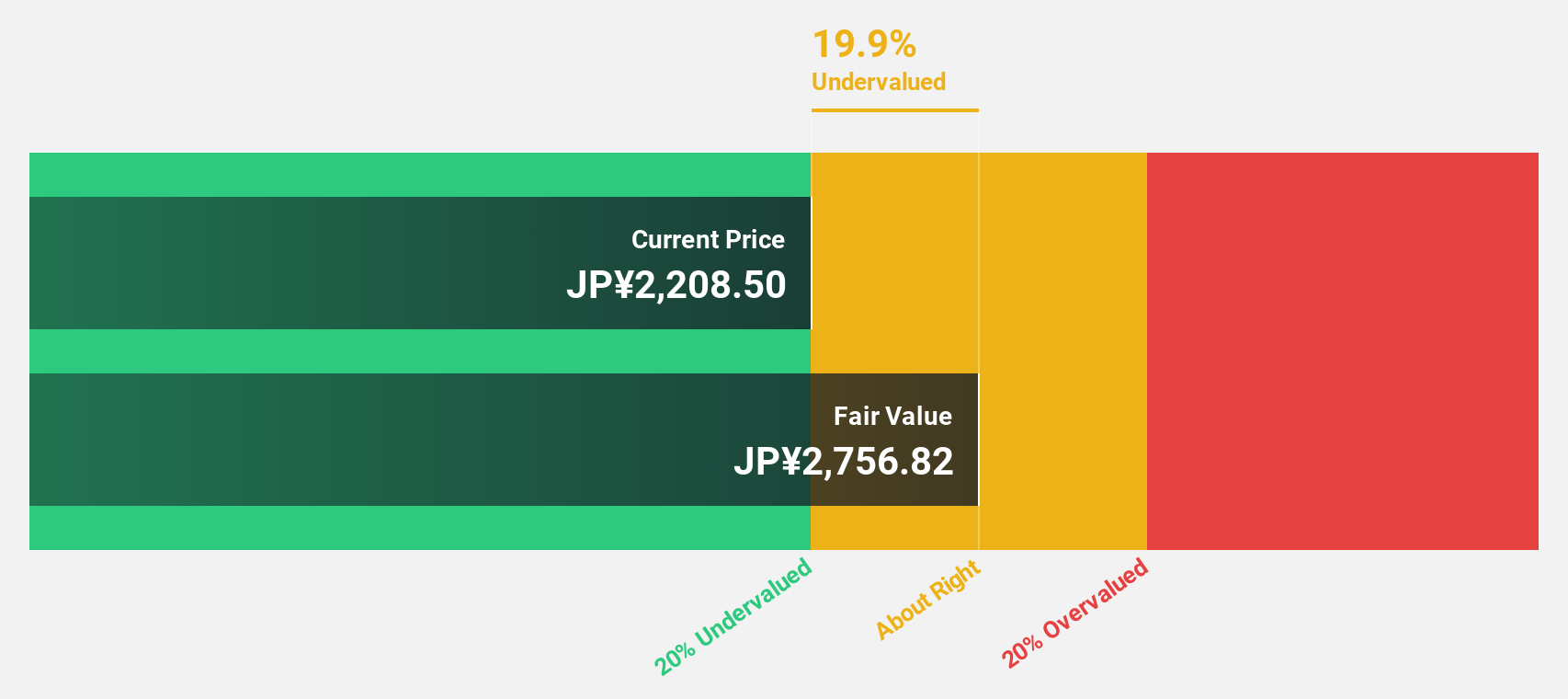

MonotaRO (TSE:3064)

Overview: MonotaRO Co., Ltd. operates an online store specializing in maintenance, repair, and operations (MRO) products for factories both in Japan and internationally, with a market capitalization of approximately ¥971.12 billion.

Operations: The company generates revenue primarily through its Indirect Material Sales Business for Factories, amounting to ¥350.36 billion.

Estimated Discount To Fair Value: 24.3%

MonotaRO is trading at ¥1,975, below its estimated future cash flow value of ¥2,608.95, suggesting potential undervaluation. The company reported strong sales growth in recent months and completed a share buyback totaling ¥9.99 billion. However, its dividend yield of 1.87% is not well covered by free cash flows. Earnings are projected to grow at 12% annually, outpacing the Japanese market average while maintaining a high forecasted return on equity of 28.4%.

- According our earnings growth report, there's an indication that MonotaRO might be ready to expand.

- Get an in-depth perspective on MonotaRO's balance sheet by reading our health report here.

Turning Ideas Into Actions

- Embark on your investment journey to our 182 Undervalued Asian Stocks Based On Cash Flows selection here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com