Did BRP's New Global PA&A Hub Just Shift BRP's (TSX:DOO) Investment Narrative?

- In early July 2026, BRP Inc. opened its largest global distribution and logistics center in Saint-Philippe, Quebec, a 950,000-square-foot hub that now handles all parts, accessories, and apparel shipments for its brands to over 2,050 dealers in 110 countries.

- This consolidation supports a PA&A business that generates more than CA$1,000 million in annual revenue and has seen sales more than double over the past decade, while also deepening BRP’s ties to the local community through a CA$75,000 school donation.

- Next, we’ll examine how centralizing PA&A logistics in Saint-Philippe could reshape BRP’s investment narrative around margins, scale, and growth.

Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

BRP Investment Narrative Recap

To own BRP, you have to believe its powersports ecosystem can keep converting passionate riders into recurring, higher-margin PA&A spending, even through economic and regulatory bumps. The new Saint-Philippe hub looks supportive for the near term margin recovery story, but it does not directly address the biggest current risk: how sensitive BRP’s discretionary vehicle demand remains to any prolonged macro or credit tightening.

Among recent announcements, the fiscal 2027 guidance for revenue of CA$9,125 million to CA$9,375 million and net income of CA$215 million to CA$250 million matters most here. That outlook, set before the Saint-Philippe consolidation, gives investors a reference point to judge whether PA&A efficiencies and volume throughput from this new center can help offset tariff and cost pressures and support the margin and earnings recovery many are watching.

But while the logistics upgrade looks encouraging, investors should also be aware of how tariff and regulatory shocks could still...

Read the full narrative on BRP (it's free!)

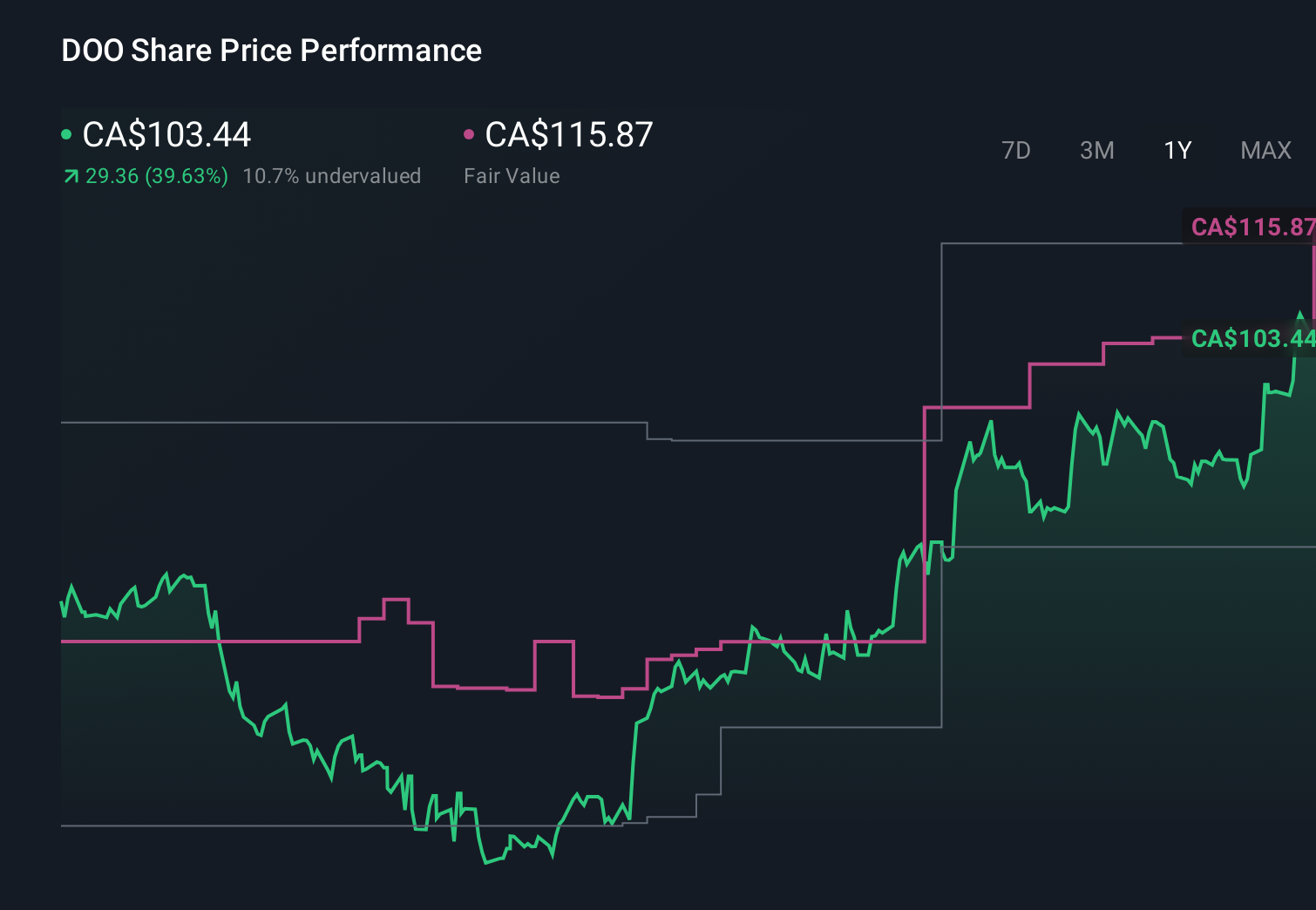

BRP's narrative projects CA$10.0 billion revenue and CA$651.2 million earnings by 2029.

Uncover how BRP's forecasts yield a CA$97.22 fair value, a 17% upside to its current price.

Exploring Other Perspectives

While consensus focuses on gradual growth and macro risks, the most optimistic analysts see CA$10.8 billion revenue and CA$689.8 million earnings potential, especially if network optimization and digital initiatives really amplify the benefits of the new Saint Philippe hub.

Explore 5 other fair value estimates on BRP - why the stock might be worth just CA$83.00!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your BRP research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free BRP research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate BRP's overall financial health at a glance.

Searching For A Fresh Perspective?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- We've uncovered the 6 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- AI is about to change healthcare. These 7 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com