3 Defensive Dividend Stocks For Higher Rates and Sticky Inflation

With the Federal Reserve under Kevin Warsh signaling no more rate cuts for 2026 and even hinting at a possible hike, many growth stocks face a tougher backdrop, while pockets of value and income are gaining attention. Higher borrowing costs, sticky inflation, and sector rotation toward more defensive areas are reshaping where risk and opportunity sit. This article looks at how that backdrop connects with our Value and Defensive Dividend Stocks screener and reveals 3 stocks that appear well aligned with the current macro tone, helping you decide whether they deserve a closer look or a wider berth.

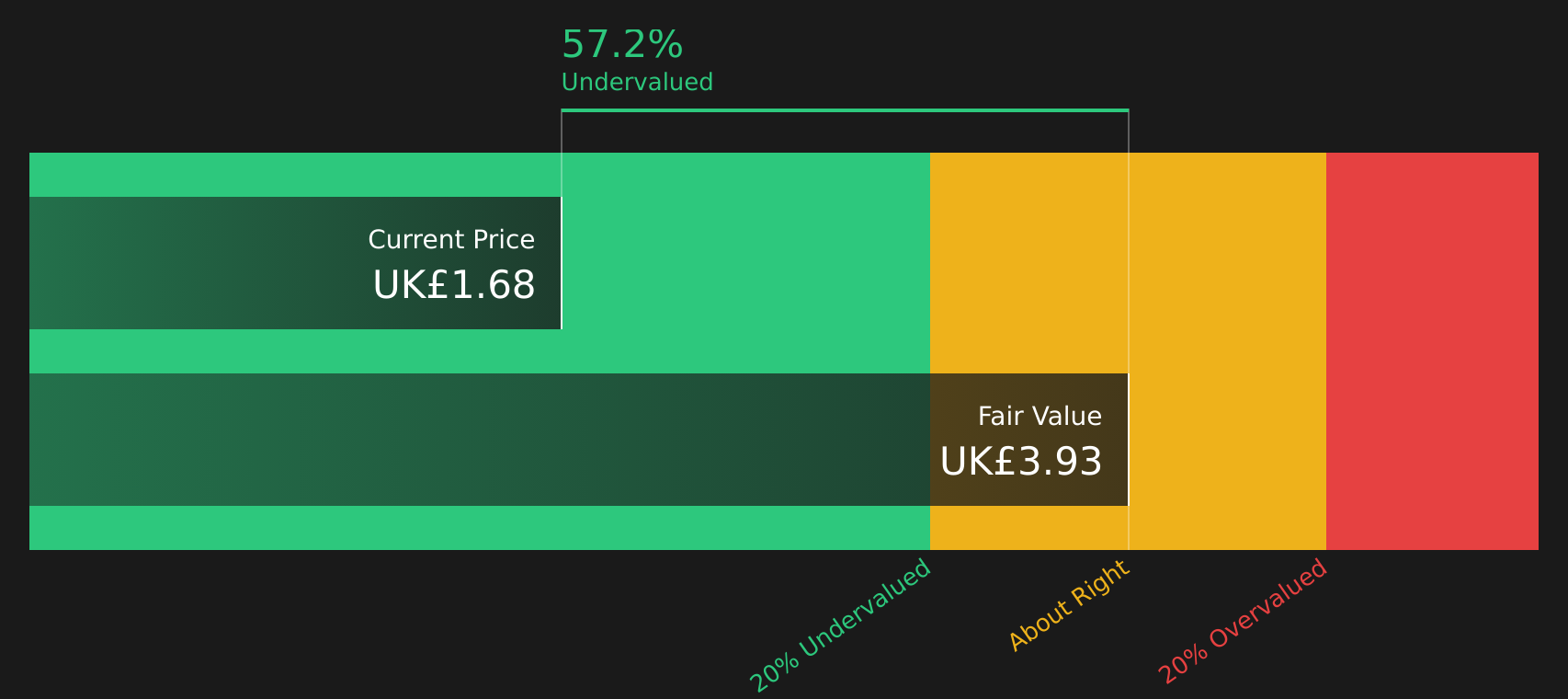

Scales (NZSE:SCL)

Overview: Scales Corporation is a diversified New Zealand agribusiness that processes and markets protein products, runs apple orchards and fruit packing operations, produces juice concentrate, and offers cold storage, freight, logistics, and insurance services across New Zealand, Asia, Europe, North America, and other regions.

Operations: Scales generates most of its NZ$899.9 million revenue from Global Proteins at NZ$477.6 million and Horticulture at NZ$341.8 million. Logistics contributes NZ$119.3 million and the remainder comes from Other activities. Sales are broadly split between Asia at NZ$364.7 million and North America at NZ$361.7 million, with New Zealand at NZ$123.4 million and smaller contributions from Europe and other regions.

Market Cap: NZ$961.7 million

Scales stands out in a higher rate world because its core businesses in premium apples, protein ingredients, and logistics are geared toward everyday food demand rather than discretionary spending. This can help support more resilient earnings and dividends. The company is growing its premium apple mix and expanding Global Proteins, supported by recent guidance upgrades, stronger gross margins, and efficiency initiatives, while still trading at a wide discount to an internal DCF estimate of fair value. At the same time, investors need to weigh exposure to New Zealand horticulture, rising costs, and a funding structure reliant on external borrowing, plus a recent one off gain that flatters earnings. How all of this nets out for Scales is where the real opportunity or risk sits.

Scales looks like an everyday essentials business hiding a more complex story, with premium apples, proteins, and logistics all in play. Get the full context with the 4 key rewards and 3 important warning signs

M.P. Evans Group (AIM:MPE)

Overview: M.P. Evans Group is a UK headquartered agribusiness that owns and operates oil palm plantations in Indonesia and Malaysia, producing and selling crude palm oil and palm kernels, while also providing management and agronomy services and participating in property development.

Operations: The group generates virtually all of its roughly US$371 million revenue from its Indonesian plantation operations, with a very small contribution from other activities.

Market Cap: £805.2 million

M.P. Evans Group offers a mix of value, income, and balance sheet strength that stands out at a time when higher interest rates are rewarding cash generative, asset backed businesses. The company has reported record results with high profit margins, is debt free with net cash, and has a history of returning capital through growing dividends and a buyback program of up to 10% of its shares. At the same time, investors need to factor in palm oil pricing cycles, weather risk in Indonesia, exposure to export levies, and an uneven dividend track record. How those supports and pressure points interact, especially as the Fed keeps policy tight and income stocks stay in focus, is where the real interest in M.P. Evans lies.

Record results, high margins, and a net cash position suggest M.P. Evans might be a stronger income story than the market gives it credit for right now. However, the real twist sits inside the 3 key rewards and 3 important warning signs (1 is major!)

AEP Plantations (LSE:AEP)

Overview: AEP Plantations is a London based agribusiness that owns and runs oil palm and rubber plantations in Indonesia and Malaysia, harvesting fresh fruit bunches and rubber and processing them into crude palm oil, palm kernels, biogas products, rubber slab, and electricity sold into the national grid.

Operations: AEP Plantations generates all of its US$465.21 million revenue from the cultivation of plantations, primarily in Indonesia and Malaysia.

Market Cap: £621.6 million

AEP Plantations may appeal to investors looking for value and income exposure to the palm oil sector, with a P/E of 9.2x, earnings described as high quality, and a 19.5% net profit margin alongside a record of dividend payments, including a recently confirmed 2025 payout of 81.0 cents per share. At the same time, the stock carries funding risk because all liabilities rely on external borrowing, as well as an unstable dividend history and share price volatility, which can matter when rates stay higher for longer. The planned 10 for 1 stock split, recent buybacks, and relatively low analyst coverage are additional features that some investors may consider when assessing AEP Plantations as a potential defensive value-oriented holding.

AEP Plantations looks like a classic income stock on the surface, but its 10 for 1 split, buybacks, and funding profile hint at a more complex risk reward trade off that comes into focus in the 3 key rewards and 2 important warning signs

The three dividend ideas here are just a starting point, with our full Value and Defensive Dividend Stocks screener surfacing 13 more companies with equally interesting income stories and risk profiles through the Value and Defensive Dividend Stocks screener. Identify and analyze the specific catalysts, balance sheet strength, and payout profiles that matter to you on Simply Wall St, so you can focus on the income plays that best fit your own conviction and risk tolerance.

Take Control of Your Investment Journey

If Scales or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Dividends?

Some of the most interesting stock ideas gain momentum quietly, then move once the crowd catches on. Scan these updated lists before the best entry points change.

- Target resilient potential with a curated set of companies that pair strong balance sheets with solid fundamentals using the list of solid balance sheet and fundamentals (419 results).

- Explore the metals space by reviewing curated producers in the 33 elite gold producer stocks.

- Spot under-the-radar opportunities where cash flow and growth ambitions meet in the 63 profitable AI stocks that aren't just burning cash while they are still off most investors’ radars.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com