3 European Travel Stocks Facing Border Control Disruption Risks

Europe’s new border control system is turning into a real stress test for travel and tourism stocks, as queues, suspended checks, and calls for an overhaul raise questions about costs, capacity, and reputation. When passenger flow depends on smooth airport operations, even a technical glitch can ripple through airlines, airport operators, and tourism groups. This article focuses on that pressure point, using our European Travel and Tourism Companies Facing Border System Headwinds screener to spotlight 3 stocks that look particularly exposed to these disruptions, and why some investors may choose to steer clear or tread carefully around them right now.

Aegean Airlines (ATSE:AEGN)

Overview: Aegean Airlines is Greece’s flagship airline, carrying passengers and cargo on scheduled, unscheduled and charter flights across domestic and international routes, while also providing aircraft maintenance, ground handling and leasing services from its Athens base.

Market Cap: €1.12b

Aegean Airlines may screen as appealing, with profitability over the last five years, high recent ROE around 20.8% and a P/E that sits below many peers, but the picture looks far less comfortable once current headwinds are factored in. The company is already dealing with widened quarterly losses, heavy reliance on higher risk funding sources and an unstable dividend record. It now faces an EU border system that is disrupting key Greek airports and could frustrate tourists at the height of the season. For an airline so closely tied to Greece’s inbound traffic, operational bottlenecks, customer frustration and any cooling of demand could matter far more than the headline valuation suggests.

Aegean Airlines’ low P/E and high ROE can easily distract from widening losses, funding stress and border chaos risk, so it is worth reading the 4 key rewards and 1 important warning sign before this story takes an unexpected turn

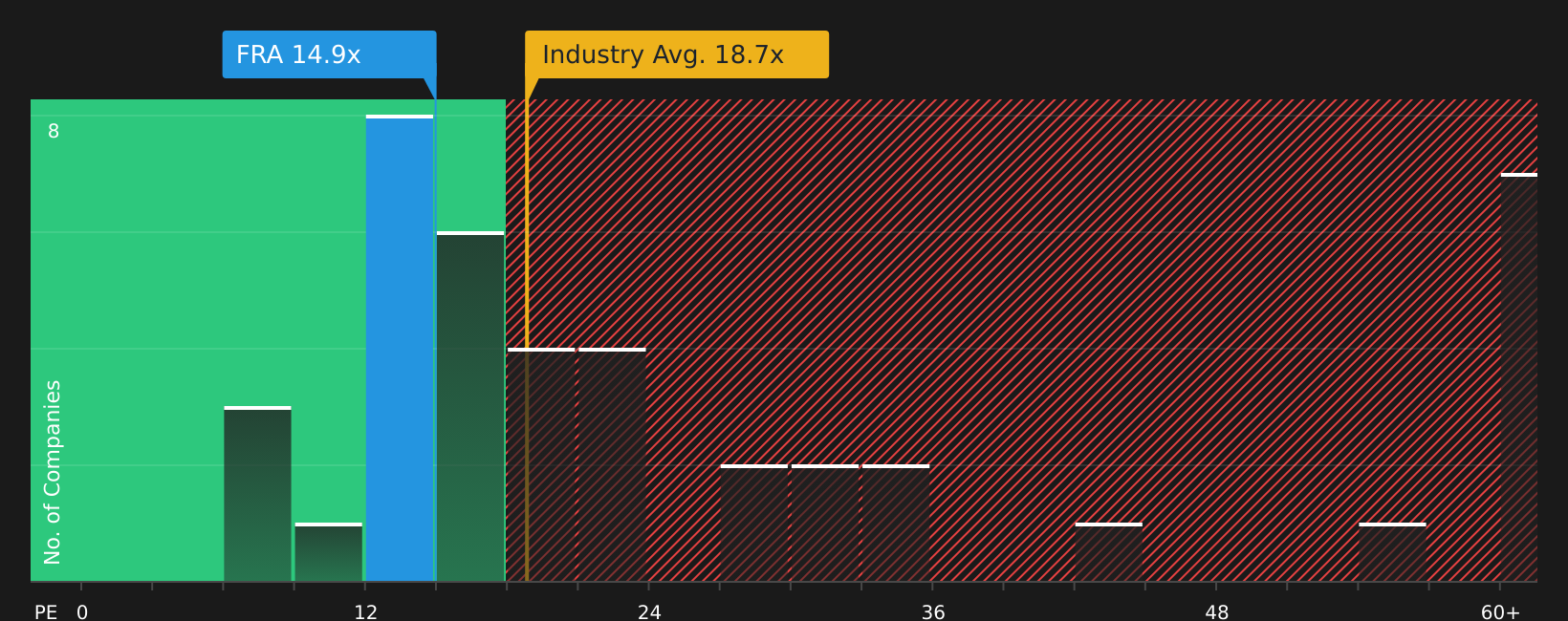

Fraport (XTRA:FRA)

Overview: Fraport is a global airport operator best known for running Frankfurt Airport while also managing and providing services at airports across Europe, the Americas and other regions.

Operations: Fraport generates about €1.5b from Aviation, €927.1m from Ground Handling, €806.8m from Retail & Real Estate, €2.2b from International Activities & Services and records a segment adjustment of €848m.

Market Cap: €6.44b

Fraport might look appealing at first glance, with earnings growth, a P/E below many infrastructure peers and a focus on higher margin retail and international airport assets. However, the picture turns more uncomfortable once current risks are layered in. The company carries high leverage, posted a small net loss in Q1 2026 and relies heavily on Frankfurt at a time when management itself has called the EU entry exit system a “real problem” that is causing delays across Europe. With Fraport Greece directly exposed to the airports now in the headlines, investors face a mix of operational disruption, potential extra technology and staffing costs and reputational damage that could challenge the idea that this stock is simply “cheap” rather than risky.

Fraport’s earnings wobble, high leverage and border system headaches could be masking deeper pressure on its core hub and overseas assets. It is worth reading the 3 key rewards and 1 important major warning sign to see what might be building beneath the surface.

TUI (XTRA:TUI1)

Overview: TUI is a large European tourism group that packages flights, hotels, cruises and local experiences into holidays under brands such as TUI Blue, Riu, Marella and Hapag-Lloyd Cruises, selling trips directly and through third party travel agents worldwide.

Operations: TUI generates most of its revenue from its Markets & Airlines divisions, with around €9.1b from the Northern region, €9.0b from the Central region and €3.4b from the Western region, alongside €2.3b from Hotels & Resorts, €1.5b from TUI Musement and €890.5m from Cruises.

Market Cap: €3.59b

TUI may appear attractively valued at first glance, with historic earnings growth, a P/E around 5.1x and reported undervaluation against some fair value estimates, but the current risks are hard to ignore. The group is still loss making in the first half of 2026, carries funding risk due to reliance on external borrowing, and is heavily exposed to Greece and other Mediterranean destinations at a time when border system failures threaten queues, cancellations and unhappy customers. In addition, TUI is spending heavily on transforming its Markets & Airlines segment and rolling out new digital and product initiatives, which adds cost precisely when travel disruption and geopolitical shocks can quickly unsettle bookings.

TUI’s low P/E near 5.1x can make the stock look like a bargain, but heavy borrowing, ongoing losses and border turmoil may be telling a different story. Compare that picture with the analysis report for TUI to see what might be missing.

Take Control of Your Investment Journey

If Fraport or any of these companies are making you feel more cautious, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Others Catch On?

Fresh stock ideas can move from quiet to crowded fast, as momentum builds and prices start flying. The best entry points may be taken by early movers, so consider acting before they do.

- Spot potential turnarounds early by scanning 215 high quality undervalued stocks that may still be under the radar for now, before renewed interest builds momentum.

- Ride long term income themes by checking the 471 dividend fortresses that could help anchor a portfolio when prices are swinging.

- Position ahead of infrastructure demand by reviewing 34 power grid technology and infrastructure stocks supporting critical energy and grid upgrades while the crowd is still focused elsewhere.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com