Frasers Property (SGX:TQ5) Plans Singapore CEO Succession, Is The Valuation Gap Being Missed?

Frasers Property (SGX:TQ5) has outlined a planned leadership transition in its Singapore business, with CEO Soon Su Lin moving into an Adviser role and Tan Wee Hsien stepping in as CEO Designate.

See our latest analysis for Frasers Property.

At a share price of SGD1.08, Frasers Property has seen a 4.85% 90 day share price return and a 26.08% 1 year total shareholder return. This suggests recent momentum contrasts with softer year to date share price performance as investors weigh leadership succession and broader group developments.

If this kind of leadership transition has you thinking about where else value and growth potential might be hiding, now is a good time to broaden your search and check out our 108 top founder-led companies

Frasers Property trades at a sizeable discount to both intrinsic estimates and analyst targets, yet the share price has only inched up after the leadership news. Is the market sensibly cautious, or mispricing the story?

Price-to-Earnings of 24.6x: Is it justified?

Frasers Property trades on a P/E of 24.6x, which screens as expensive relative to both its own fair P/E estimate and the broader Singapore real estate peer group.

The P/E ratio compares the current share price with earnings per share, so a higher multiple usually means investors are paying more for each dollar of profit. For a company like Frasers Property, which operates across Singapore, Australia, Europe and the region with a sizable real estate portfolio, that multiple often reflects expectations around future earnings, asset quality and balance sheet resilience.

In this case, the stock’s 24.6x P/E stands well above the estimated fair P/E of 16.4x. This suggests the market is pricing in richer earnings expectations than this fair ratio implies. At the same time, it is also higher than the Singapore real estate industry average of 13x, so the current multiple is not just elevated versus a modelled fair level, it is also lofty compared with sector peers and could be an area investors pay close attention to if expectations change.

Explore the SWS fair ratio for Frasers Property

Result: Price-to-Earnings of 24.6x (OVERVALUED)

However, Frasers Property still faces execution risk around leadership transition and exposure to multiple real estate markets, where weaker demand or asset impairments could quickly challenge today’s valuation story.

Find out about the key risks to this Frasers Property narrative.

Another View: Frasers Property on a Cash Flow Basis

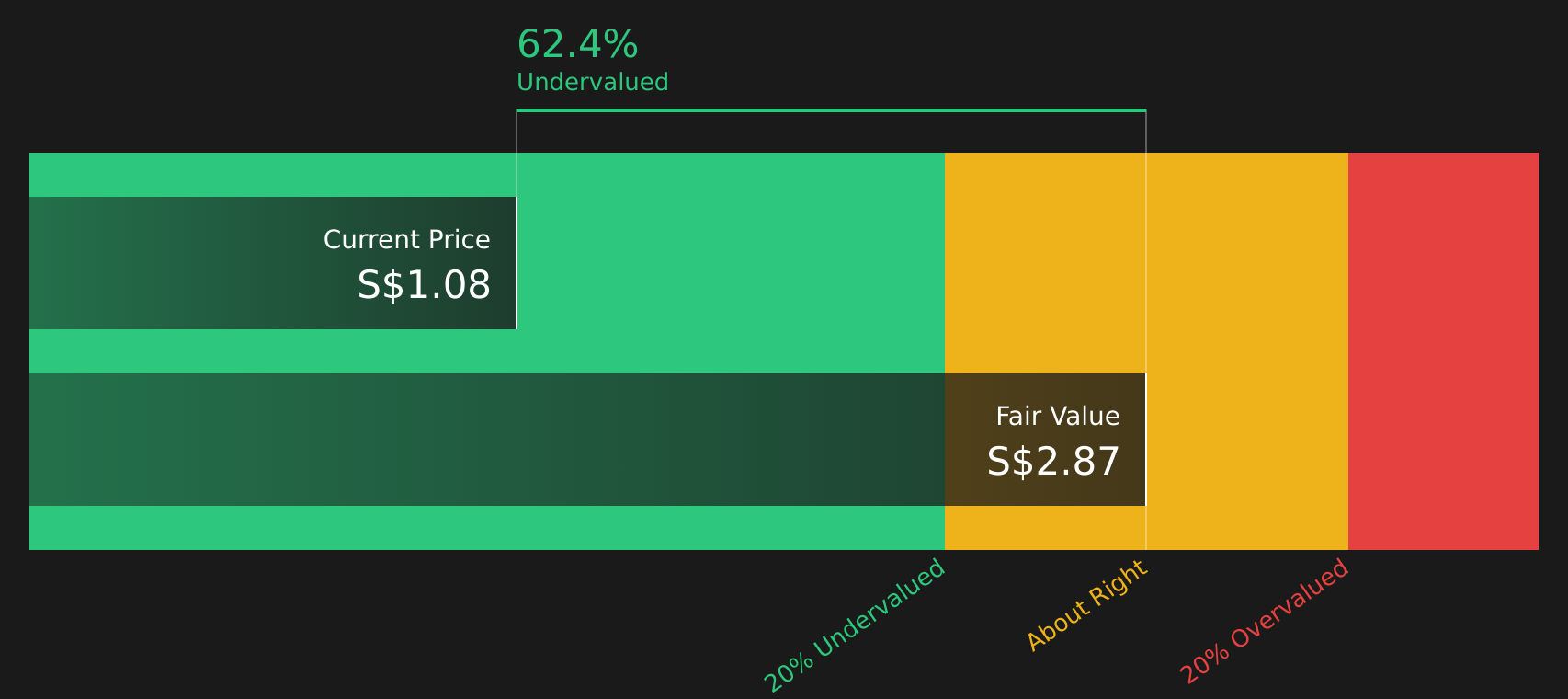

The P/E ratio presents Frasers Property as expensive, but the SWS DCF model suggests a different picture. It indicates an estimated future cash flow value of SGD2.87 per share compared with the current SGD1.08. If cash flows are closer to the mark than earnings multiples, is the real gap here upside or risk?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Frasers Property for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 215 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of caution and potential around Frasers Property leaves you unsure, act quickly by reviewing the data, weighing both sides, and checking the 2 key rewards and 2 important warning signs

Looking for more investment ideas beyond Frasers Property?

If Frasers Property has sharpened your interest, do not stop here. Broaden your watchlist with other clear, data backed opportunities across sectors and styles.

- Target resilient cash generators by reviewing our 215 high quality undervalued stocks that combine earnings strength with prices that sit below internally assessed worth.

- Strengthen your income focus by scanning the 471 dividend fortresses for companies offering higher yields with an emphasis on consistency.

- Prioritise sturdier balance sheets by running through the solid balance sheet and fundamentals stocks screener (419 results) and filter for businesses with stronger financial footing.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com