China Automobile Dealers Association: The overall inventory coefficient of car dealers in June was 1.58, down 3.1% month-on-month, up 11.3% year-on-year

The Zhitong Finance App learned that on July 10, 2026, the China Automobile Dealers Association released the results of the “Auto Dealer Inventory” survey for June 2026: The comprehensive inventory coefficient for car dealers in June was 1.58, down 3.1% from the previous month, and up 11.3% from the previous year.

The inventory coefficient increased year on year and decreased month on month in January and June

The overall performance of the passenger car market was weak in June, and terminal sales showed a “low front and back high” trend. Continued heavy rainfall, local floods, and hot summer weather in many places put a certain pressure on offline passenger flow, logistics and delivery; in addition, the World Cup divided consumption time and budget, compounded by phased factors such as busy agriculture and college entrance examinations, the overall demand for terminals was under pressure. Dealers launched a semi-annual performance sprint within the month, boosting transactions by increasing terminal discounts, compounding the acceleration of delivery pace after production capacity for new cars launched in the early stages climbed, and together led to a phased recovery in the terminal market. However, this round of market recovery was mainly driven by the mid-year assessment, not a substantial recovery on the consumer side.

According to statistics from the China Automobile Dealers Association, passenger car terminal sales reached 1.602 million units in June. According to this estimate, the total inventory of car dealers at the end of June was about 2.5 million vehicles, and the overall inventory scale of the channel was basically the same as at the end of May.

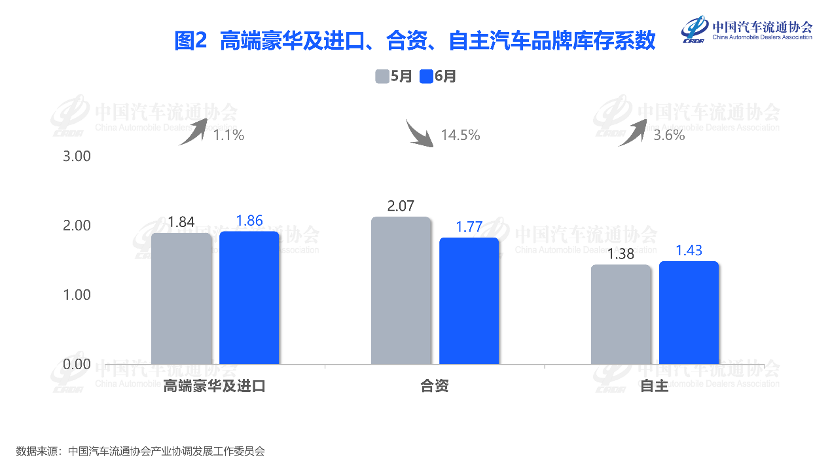

2. Inventory factors for high-end luxury, imported, and independent brands increased month-on-month, while joint venture brands declined month-on-month

The inventory coefficient for high-end luxury and imported brands was 1.86, and the inventory coefficient increased 1.1% month-on-month; the inventory coefficient for joint venture brands was 1.77, down 14.5% month-on-month; and the inventory coefficient for independent brands was 1.43, up 3.6% month-on-month.

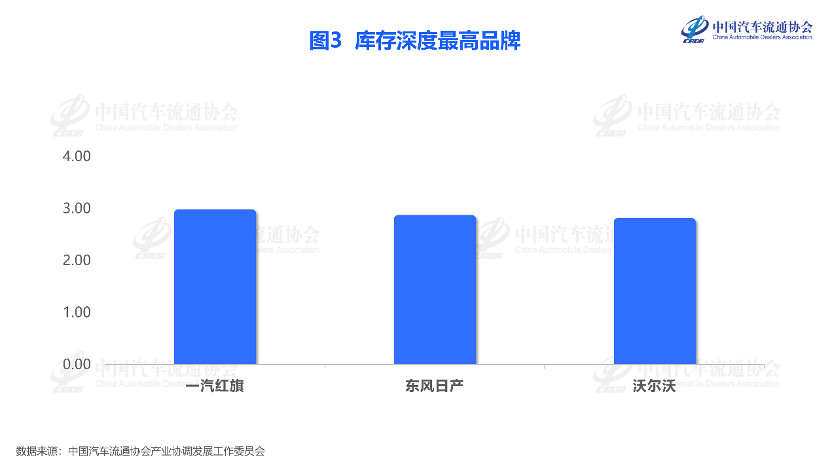

The brand with the highest inventory depth in March and June

According to the survey, the inventory depth of mainstream brands in June was greater than 2 months for a total of 7 brands, a decrease from the previous month. They are ranked by inventory depth from highest to lowest: FAW Hongqi, Dongfeng Nissan, Volvo, GAC Honda, FAW Volkswagen, Audi, and GAC Trumpchi.

4. Carefully anticipate market demand in July 2026 and reasonably control inventory

In July, the car market entered the traditional off-season operation range. Extreme weather such as typhoons, floods, landslides, and continued high temperatures in some regions. Offline store arrivals and test driving activities were significantly restricted, and market passenger flow and terminal delivery were also affected, and the demand overdraft effect formed by dealers in June continued to show; combined with the demand overdraft effect formed by dealers in June, the margins of terminal promotion narrowed. Coupled with the lack of centralized drainage during the month of large-scale holidays, consumer spending on coins increased, and overall market activity declined. However, the demand side still has bottom support: the Ministry of Commerce and other ministries have recently announced 40 pilot cities for automobile distribution and consumption reform and their key reform and innovation directions, and issued the “Notice on Certain Measures to Cultivate and Expand Automobile Aftermarket Consumption”, which will help unblock consumption blockages, optimize the consumption environment, and drive new car consumption through the release of demand in the automotive aftermarket. At the same time, the steady release of structural demand such as car purchases for summer students and long-distance family travel, as well as the continued development of trade-in and local car purchase subsidy policies, will effectively counter the downward trend in off-season demand. Due to mild mid-year impulses in June, car sales are expected to remain basically flat or increase slightly in July.

The China Automobile Dealers Association suggests that dealers should rationally estimate market demand and reasonably control inventory levels according to the actual situation. At the same time, it is necessary to increase publicity on “trade-in and end-of-life renewal policies”, boost consumer confidence by strengthening services, put cost reduction and efficiency first, and prevent business risks.