Global Growth Companies With High Insider Ownership July 2026

As global markets navigate a mixed landscape marked by cooling labor growth in the U.S., steady inflation in Europe, and resilient manufacturing activity in China, investors are increasingly focused on companies with robust fundamentals. In this context, growth companies with high insider ownership can be particularly appealing as they often demonstrate strong alignment between management and shareholder interests, which may be beneficial during times of economic uncertainty.

Top 10 Growth Companies With High Insider Ownership Globally

| Name | Insider Ownership | Earnings Growth |

| Shanghai Biren Technology (SEHK:6082) | 11% | 116.9% |

| Meitu (SEHK:1357) | 22.8% | 31.4% |

| Meiko Electronics (TSE:6787) | 19.2% | 27.6% |

| KebNi (OM:KEBNI B) | 11.8% | 90.9% |

| HUMAN MADE (TSE:456A) | 23.9% | 23.4% |

| Guangzhou Tinci Materials Technology (SZSE:002709) | 38.4% | 28.9% |

| Great Microwave Technology (SHSE:688270) | 29.5% | 85.5% |

| Gold Circuit Electronics (TWSE:2368) | 30.1% | 38.2% |

| CD Projekt (WSE:CDR) | 35.2% | 29.7% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 14.1% | 40.4% |

Underneath we present a selection of stocks filtered out by our screen.

Vista Energy. de (BMV:VISTA A)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Vista Energy, S.A.B. de C.V. operates in the exploration and production of oil and gas across Latin America, with a market capitalization of approximately MX$120.90 billion.

Operations: The company generates revenue of $2.90 billion from its activities in the exploration and production of crude oil, natural gas, and LPG.

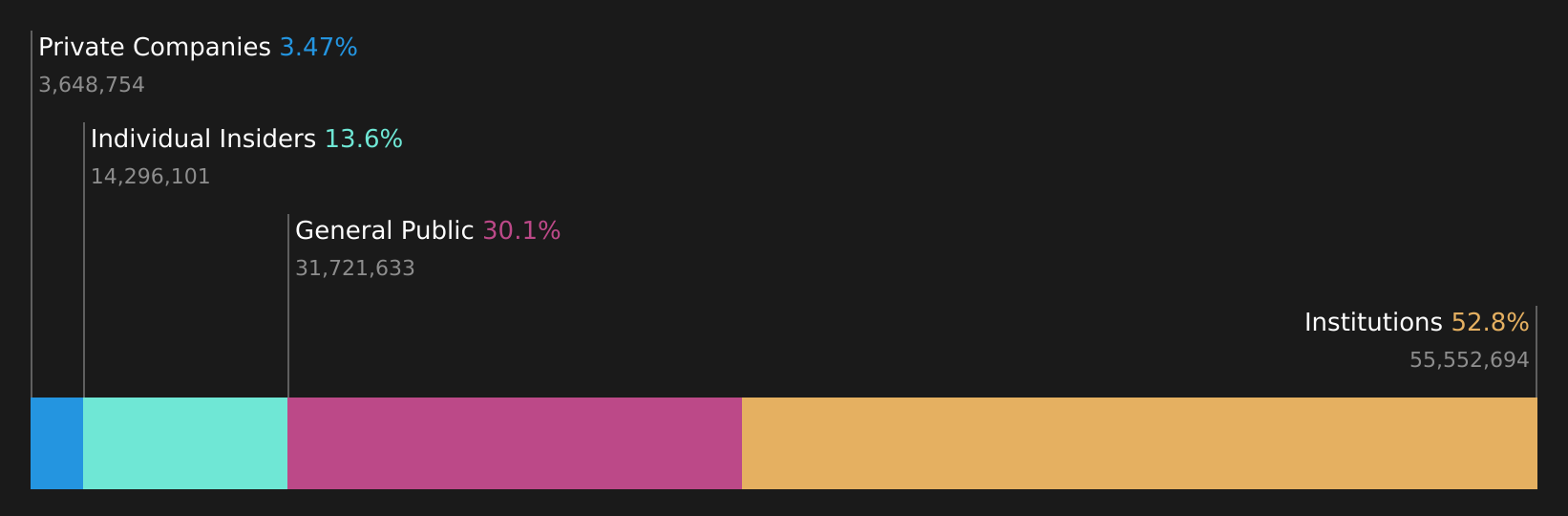

Insider Ownership: 13.6%

Revenue Growth Forecast: 12.3% p.a.

Vista Energy demonstrates strong growth potential with forecasted revenue and earnings growth rates of 12.3% and 14.7% per year, respectively, surpassing the MX market averages. Despite its high debt levels, the company trades at a significant discount to its estimated fair value and has shown substantial earnings improvement, with Q1 sales reaching US$865 million compared to US$438.46 million last year. Recent presentations at major conferences suggest active engagement in investor relations efforts.

- Delve into the full analysis future growth report here for a deeper understanding of Vista Energy. de.

- According our valuation report, there's an indication that Vista Energy. de's share price might be on the cheaper side.

Vanchip (Tianjin) Technology (SHSE:688153)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Vanchip (Tianjin) Technology Co., Ltd. designs, manufactures, and sells radio frequency front end and high-end analog chips in China with a market cap of CN¥13.62 billion.

Operations: The company's revenue is primarily generated from electronic components and parts, amounting to CN¥2.30 billion.

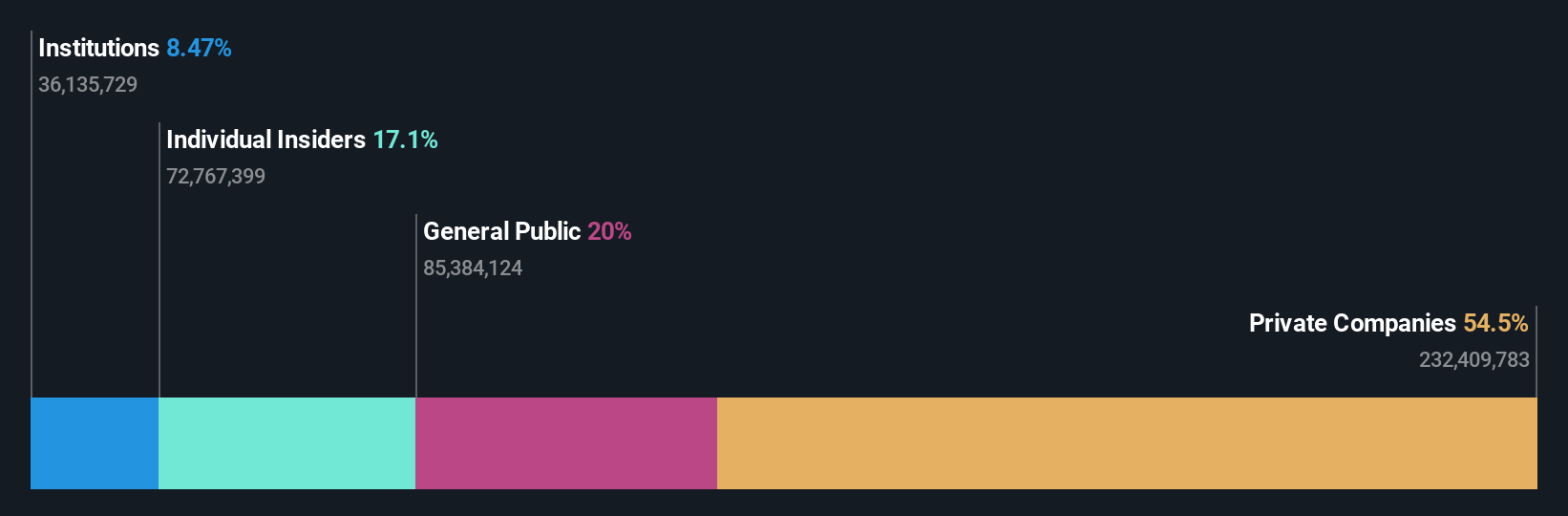

Insider Ownership: 16.8%

Revenue Growth Forecast: 17.2% p.a.

Vanchip (Tianjin) Technology's earnings are expected to grow significantly, outpacing the CN market with a forecasted annual growth rate of 71.3%. Despite becoming profitable this year, recent financials show a net loss of CNY 48.14 million for Q1 2026. The company's revenue growth is projected at 17.2% annually, slightly above the market average. Recent shareholder activities include approving an audit institution proposal during its Annual General Meeting on June 23, 2026.

- Click to explore a detailed breakdown of our findings in Vanchip (Tianjin) Technology's earnings growth report.

- Our expertly prepared valuation report Vanchip (Tianjin) Technology implies its share price may be too high.

APT Medical (SHSE:688617)

Simply Wall St Growth Rating: ★★★★★☆

Overview: APT Medical Inc. focuses on the research, development, production, and sale of cardiovascular interventional medical devices in China with a market cap of CN¥27.85 billion.

Operations: The company generates revenue of CN¥2.72 billion from its medical products segment, specializing in cardiovascular interventional devices within China.

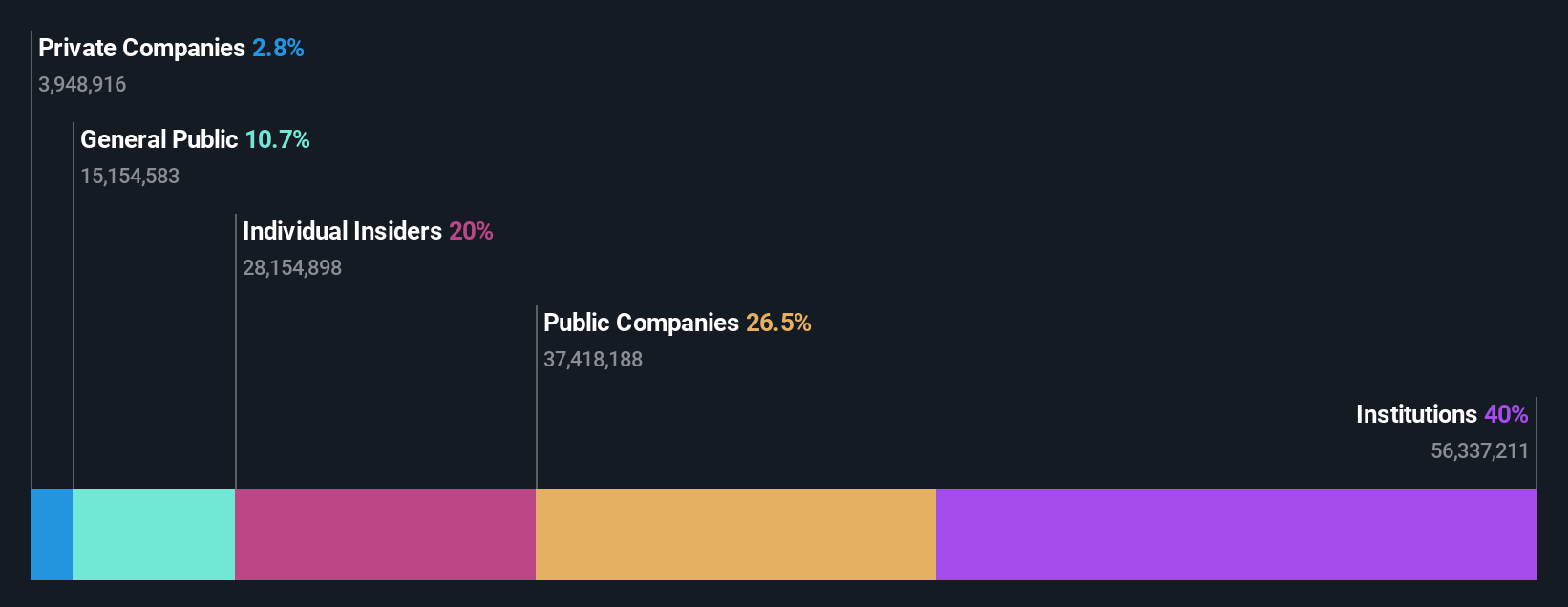

Insider Ownership: 20%

Revenue Growth Forecast: 22.3% p.a.

APT Medical demonstrates strong growth potential, with earnings expected to grow significantly at 23% annually, though slightly below the CN market's pace. Revenue growth is forecasted at 22.3%, surpassing market expectations. The company recently completed a share buyback worth CNY 99.98 million, enhancing shareholder value and potentially boosting insider ownership stakes. Despite an unstable dividend track record, APT Medical trades below its estimated fair value and analyst price targets suggest a significant upside potential of 63.7%.

- Click here and access our complete growth analysis report to understand the dynamics of APT Medical.

- Upon reviewing our latest valuation report, APT Medical's share price might be too pessimistic.

Summing It All Up

- Click through to start exploring the rest of the 683 Fast Growing Global Companies With High Insider Ownership now.

- Ready For A Different Approach? AI is about to change healthcare. These 129 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com