Is Primerica (PRI) Fairly Valued As Russell 1000 Index Removal Shifts Focus?

Primerica (PRI) has been removed from the Russell 1000 Dynamic Index, an action that can prompt index-tracking funds and other benchmark-focused investors to adjust positions. This change may affect trading activity and market attention around the stock.

See our latest analysis for Primerica.

Despite being dropped from the Russell 1000 Dynamic Index, Primerica’s recent share price momentum has been firm, with a 30 day share price return of 12.66% and a 5 year total shareholder return of 125.62%. This suggests that investors have been reassessing both growth prospects and risk over time.

If this index change has you reviewing your portfolio, it can be a good moment to broaden your search and check out 18 top founder-led companies

Bulls point to Primerica’s recent gains and steady business mix, while bears question whether the index removal hints at stretched expectations. So which side does the valuation evidence support next?

Most Popular Narrative: 3% Overvalued

The most followed narrative currently places Primerica's fair value at $298.50, just below the last close of $306.20, so expectations are finely balanced.

Strong demographic drivers, especially the large cohort of Baby Boomers and Gen X approaching retirement, are fueling sustained demand for retirement planning products, annuities, and investment solutions, providing a multi-year tailwind for Primerica's ISP segment and supporting double-digit sales growth, which should boost top-line revenue and client assets.

Want to see how a steady revenue glide path, slightly tighter margins, and a higher future earnings multiple are stitched together into one valuation story? The key tension sits between modest growth assumptions and a richer future P/E, all filtered through a single discount rate and ongoing share count reduction.

Result: Fair Value of $298.50 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still pressure points, including softer term life policy trends and rising operating expenses, that could challenge Primerica’s earnings path and valuation story.

Find out about the key risks to this Primerica narrative.

Another View on Primerica’s Valuation

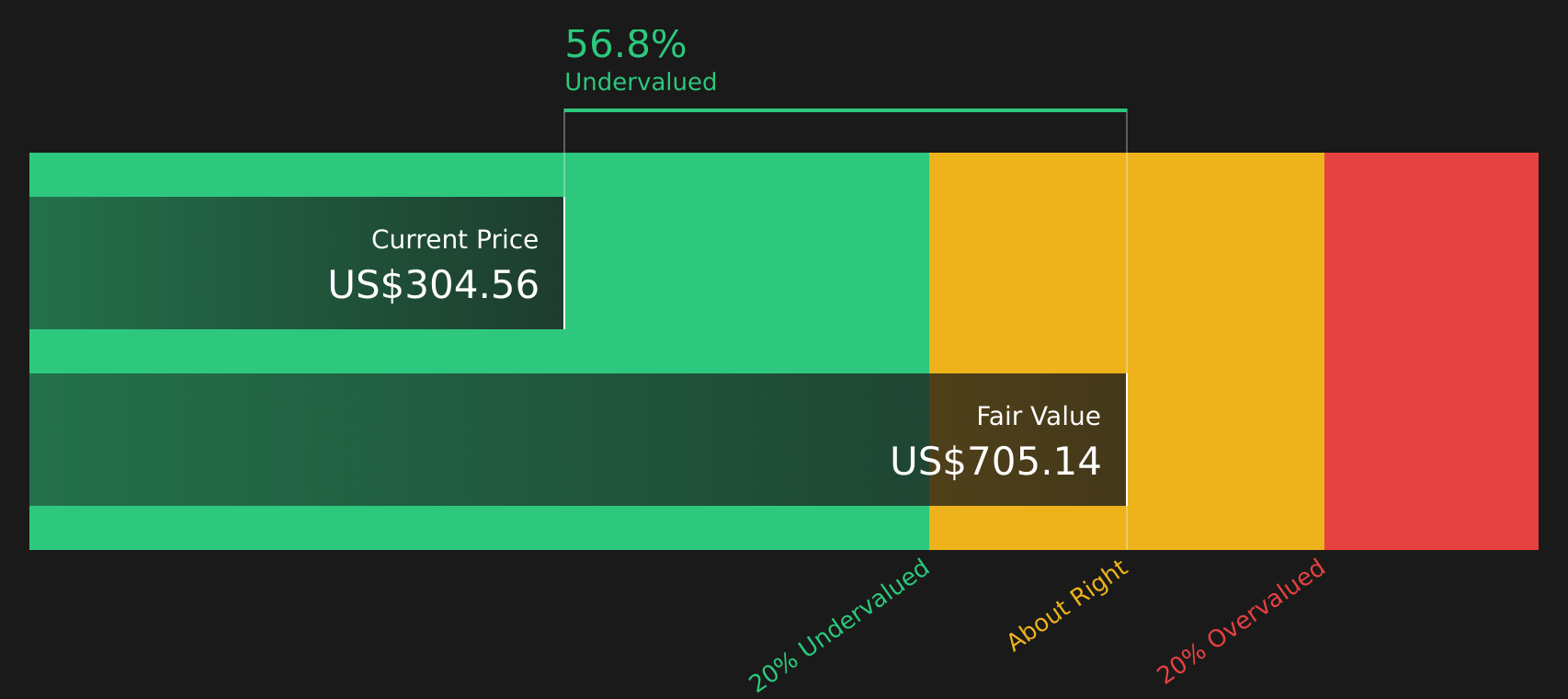

The analyst narrative has Primerica at around 3% overvalued on a fair value of $298.50 versus the $306.20 share price. Our DCF model presents a different perspective, with a future cash flow value of $700.48 per share, which frames the current price as heavily undervalued instead. Which set of assumptions feels more realistic to you?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Primerica for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Conflicted by the mix of optimism and concern around Primerica’s outlook and valuation story today? Take a closer look at the underlying data, weigh both sides, and then assess the 3 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Primerica?

If this Primerica update has sharpened your thinking, do not stop here. Let the same disciplined approach guide you toward fresh stock ideas that fit your goals.

- Hunt for potential bargains by screening companies that combine quality with attractive pricing using the 44 high quality undervalued stocks.

- Prioritise resilience and capital protection by focusing on companies with steadier risk profiles through the 73 resilient stocks with low risk scores.

- Seek early-stage opportunities with solid financial footing by scanning the 20 elite penny stocks with strong financials.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com