nLIGHT (LASR) Is Up 18.1% After Securing Major US$627 Million Laser Weapon Deal - Has The Bull Case Changed?

- On 9 July 2026, nLIGHT, Inc. announced it had been selected for a Joint Laser Weapon System Other Transaction Authority agreement supporting the U.S. Department of War’s next-generation cruise missile defense architecture, with an initial US$44 million award and a potential ceiling of up to US$627 million for follow-on work.

- This award expands nLIGHT’s role in high-energy laser weapons, highlighting how its coherent beam combination technology and vertically integrated manufacturing are being pulled into containerized systems intended for rapid deployment across multiple defense platforms.

- We’ll now examine how this sizeable Joint Laser Weapon System award, built around modular high-energy laser platforms, could reshape nLIGHT’s investment narrative.

We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

nLIGHT Investment Narrative Recap

To own nLIGHT, you need to believe high energy lasers can become a meaningful, repeat business across U.S. and allied defense programs, offsetting a weaker and less predictable commercial segment. The JLWS win sharpens that near term catalyst by adding a concrete, modular laser weapons path, but it also heightens the key risk: even more revenue tied to U.S. defense priorities, funding cycles and execution on complex amplifier manufacturing at scale.

Against this backdrop, nLIGHT’s recent removal from multiple Russell indexes is relevant. While it does not affect operations, it can influence near term trading, liquidity and ownership mix just as the market is reassessing JLWS and other directed energy programs as potential earnings drivers.

Yet behind the contract headlines, investors should also factor in how concentrated defense exposure and index removal could impact liquidity and valuations over time...

Read the full narrative on nLIGHT (it's free!)

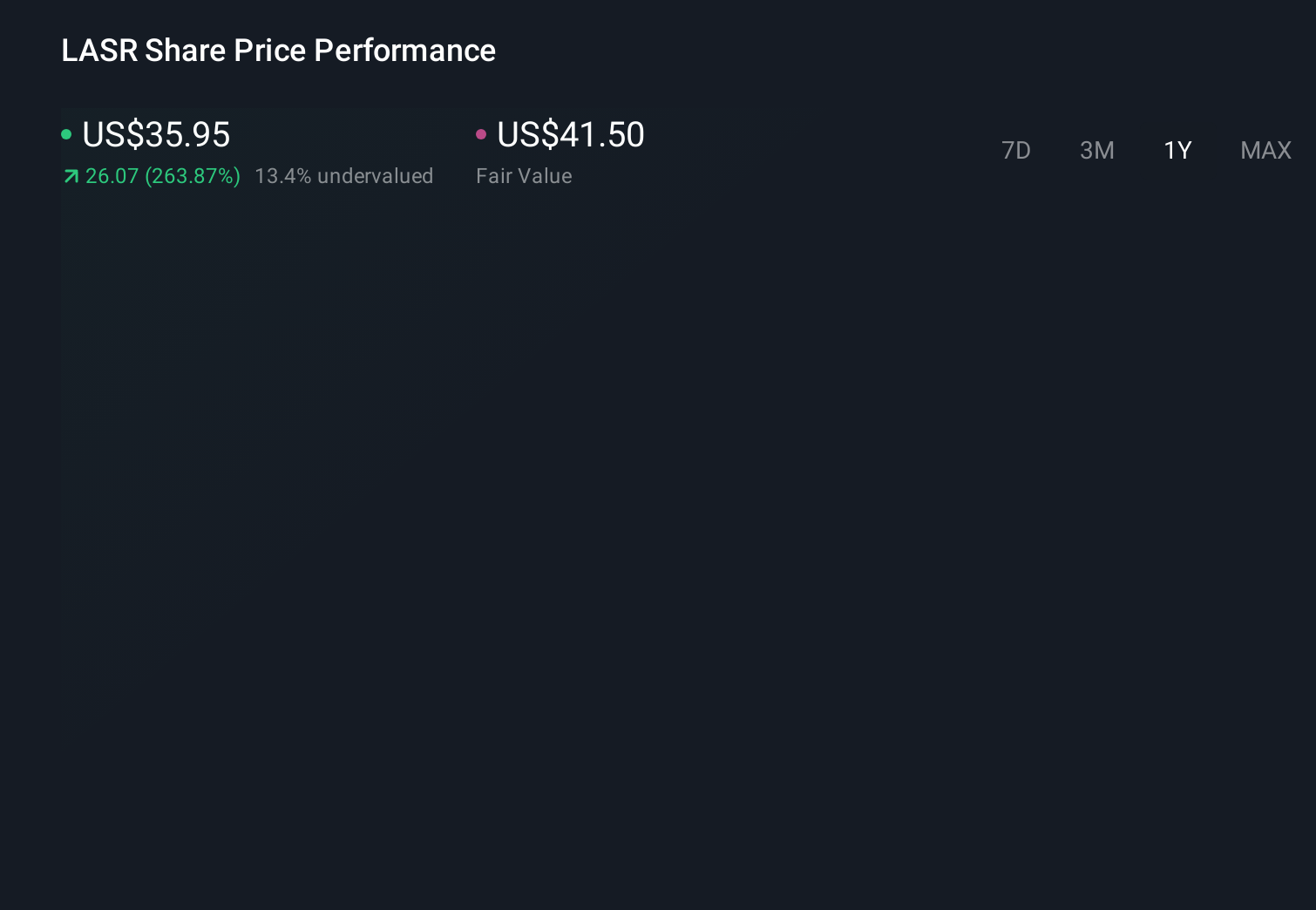

nLIGHT's narrative projects $454.9 million revenue and $8.2 million earnings by 2029.

Uncover how nLIGHT's forecasts yield a $86.43 fair value, a 16% upside to its current price.

Exploring Other Perspectives

Before JLWS, the most cautious analysts already assumed revenue of about US$463.1 million and earnings of US$36.1 million by 2029, so this new contract could challenge that more pessimistic view and is a reminder that your own expectations might sit anywhere between those bookends.

Explore 5 other fair value estimates on nLIGHT - why the stock might be worth as much as 34% more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your nLIGHT research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free nLIGHT research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate nLIGHT's overall financial health at a glance.

Searching For A Fresh Perspective?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com