Chinese AI Stocks Retail Investors Are Watching After The Manus Deal Fell Apart

China’s push to keep core artificial intelligence talent and data under local control is reshaping who gets access to promising AI companies like Manus. Beijing’s order for Meta to unwind its planned $2b purchase of Manus, and Tencent’s move to step in at the same valuation, highlight how policy decisions can quickly change the outlook for listed Chinese AI stocks. For investors, this creates fresh questions about regulatory risk, capital access, and competitive positioning. This article looks at 3 Chinese AI related stocks exposed to this news, each presented as a potential beneficiary in different ways.

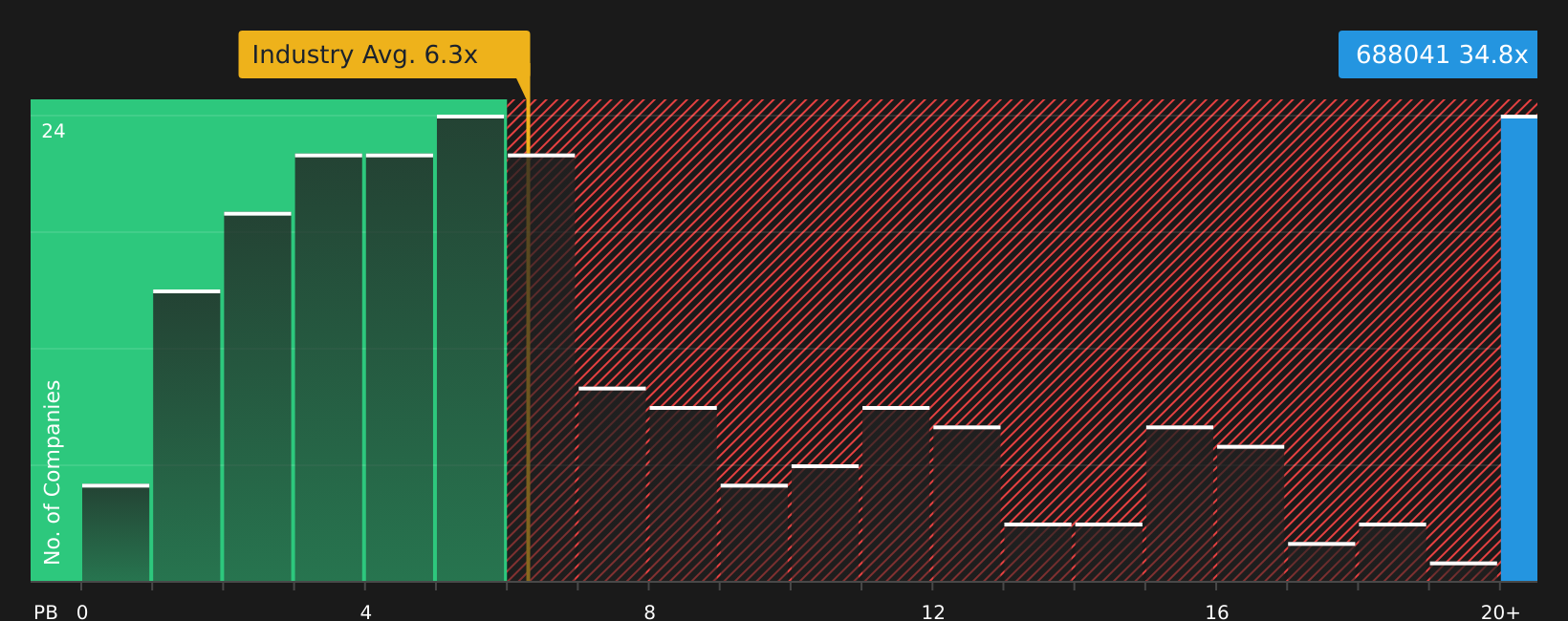

Hygon Information Technology (SHSE:688041)

Overview: Hygon Information Technology develops and sells high performance processors, accelerators, and computing chip systems used in data centers, cloud computing, artificial intelligence, and industrial and scientific computing across China. Its products support commercial workstations and secure, domestically produced computing infrastructure for a wide range of enterprise and government workloads.

Market Cap: CN¥843.09b

Hygon Information Technology sits at the center of China’s push for domestic AI and data center computing, which puts it directly in the slipstream of policies that favor local chip suppliers over foreign platforms after moves like Beijing blocking Meta’s Manus deal. The company reports strong historical and forecast earnings and revenue growth, with projected earnings expansion above 30% a year and a forecast ROE of 23.1% in three years. Many investors view this as attractive for a core AI hardware play. That said, the stock trades on a rich P/B multiple, has high non cash earnings and relies on higher risk external funding, so today’s momentum story is also tied to real valuation and balance sheet questions that deserve a closer look.

Hygon’s rapid earnings forecasts and premium P/B raise a key question: is current enthusiasm justified by the underlying business quality or mainly by sentiment, and what the 2 key rewards and 2 important warning signs (1 is major!) quietly hints at next

Cambricon Technologies (SHSE:688256)

Overview: Cambricon Technologies designs and sells core AI chips and accelerator hardware for cloud data centers, edge devices, and terminals in China, alongside the NeuWare and MagicMind software platforms that let customers build and run AI workloads on its hardware. Its portfolio ranges from smart accelerator cards and intelligent computing modules to terminal processor IP that can be embedded into third party devices.

Market Cap: CN¥964.35b

Cambricon Technologies is central to China’s push to keep AI computing capacity onshore, and the Manus decision reinforces that Beijing wants domestic suppliers in key positions. The company combines very strong recent earnings growth with high margins and a 21.1% ROE. Analysts also expect revenue and earnings to keep expanding at rates well above 50% a year. That strength comes with real trade offs, including an extremely high P/B multiple, a volatile share price and reliance on higher risk external borrowing, which all raise questions about how much optimism is already in the price and how robust the earnings quality really is.

Cambricon Technologies combines high growth expectations with a premium valuation and volatile trading, which raises a simple question for investors: what is the market really pricing in and what the 2 key rewards and 2 important warning signs (2 are major!) might be overlooking

iFLYTEKLTD (SZSE:002230)

Overview: iFLYTEKLTD provides speech recognition and broader AI technology across consumer devices, education tools, and enterprise solutions, from smart recorders and translator gadgets to AI transcription platforms and marketing services. It also runs telecom, data, software, and AI application businesses, with additional activities spanning education, industrial robots, and various online and offline services in China and overseas.

Market Cap: CN¥101.78b

iFLYTEKLTD sits in Beijing’s preferred AI camp as a government backed champion in speech and education tech, which matters more as China tightens control over AI talent and platforms after forcing Meta to unwind the Manus deal. Earnings grew 29.3% last year and analysts expect about 37.72% yearly growth ahead. However, the stock trades on a very high P/E and thin 3.1% margins, with ROE at 4.4% and funding largely from higher risk borrowing. When adding in one off gains and a recent private placement that brought in major state linked investors, the result is a business with significant policy support and growth expectations, but with valuation and balance sheet factors that may warrant closer examination.

iFLYTEKLTD’s rapid growth story, thin margins and state linked backing could be masking what really drives its valuation, so it is worth reviewing the 3 key rewards and 1 important warning sign before one detail quietly changes the whole picture.

The three Chinese AI stocks covered here are just a starting point, and the full Chinese Artificial Intelligence (AI) Companies screener surfaces 39 more companies that share similar AI linked narratives and financial filters worth your attention. Use Simply Wall St to identify and analyze the specific catalysts, balance sheet traits and earnings narratives that matter to you so you can focus on the highest conviction ideas in this theme.

Take Control of Your Investment Journey

If Cambricon Technologies or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before The Crowd?

Fresh ideas can move quickly, and potential entry points may pass by while you are still watching the last breakout. Scan these under the radar lists before the momentum is fully recognized so you can consider your options in time.

- Spot fast moving small caps before they accelerate further by scanning a curated set of 133 AI small caps that focus on real businesses, not just hype.

- Hunt for income opportunities that could provide ongoing payments even when sentiment weakens by reviewing a hand picked pool of 468 dividend fortresses built for durability.

- Track the picks that may be more resilient if conditions turn rough by checking a focused group of 291 resilient stocks with low risk scores designed with downside protection in mind.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com