DWS Group GmbH KGaA (XTRA:DWS) Weighs A New Name, Is The Stock Still A Bargain?

DWS Group GmbH KGaA (XTRA:DWS) is reportedly weighing a rebrand to Deutsche Asset Management, tying the stock more closely to Deutsche Bank’s global profile and potentially reshaping how institutional investors view the business.

See our latest analysis for DWS Group GmbH KGaA.

DWS Group GmbH KGaA’s recent rebrand discussion comes after a strong run in the stock, with a 30 day share price return of 15.43% and a year to date share price return of 20.04%, alongside a 1 year total shareholder return of 42.74% that builds on multi year gains exceeding 100%. Recent leadership appointments in Asia Pacific and the Middle East hint at investors reassessing both its growth prospects and risk profile.

If you are looking beyond DWS Group GmbH KGaA for other ideas in financials and beyond, this is a useful moment to broaden your search through 108 top founder-led companies

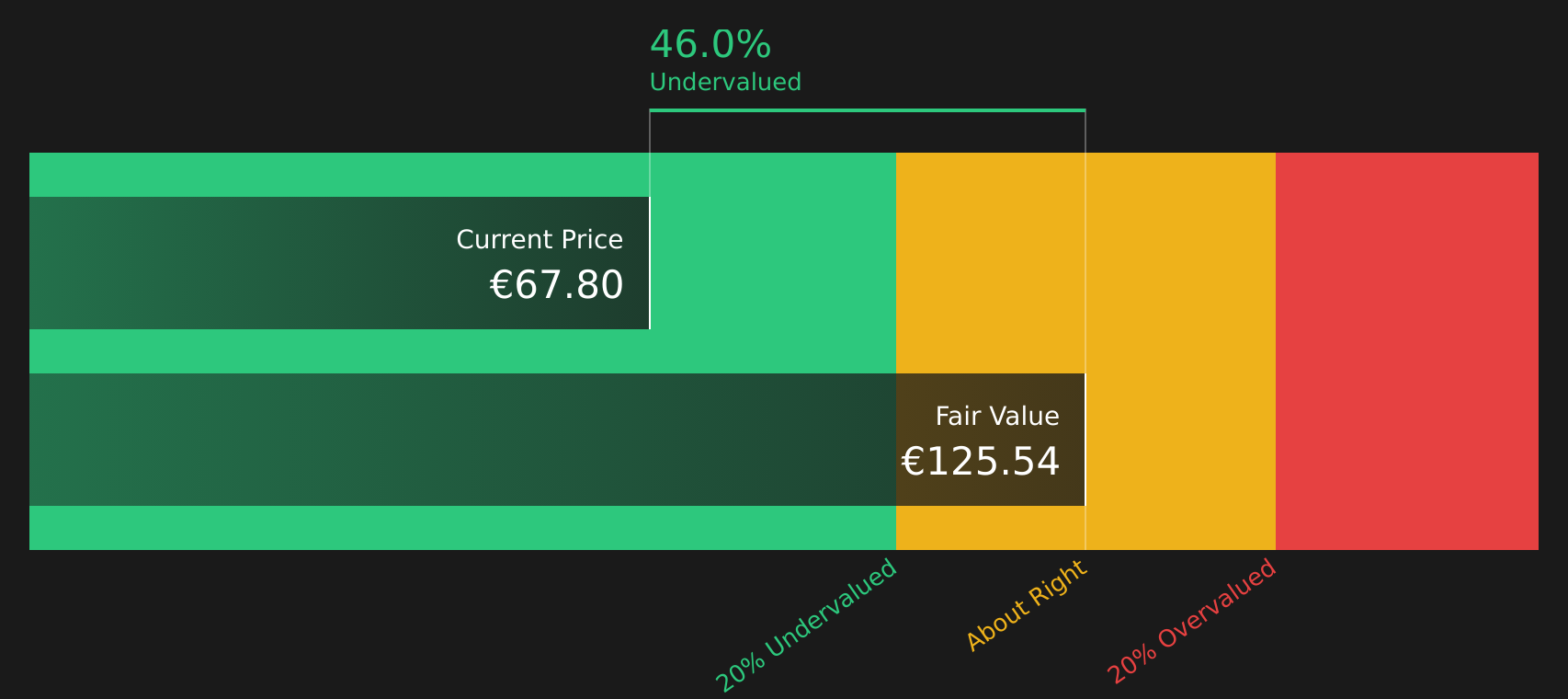

After such a sharp rerating and talk of a Deutsche Asset Management badge, DWS Group GmbH KGaA now asks a simple question of you as an investor: does the current valuation still leave enough upside for the risk you are taking?

Preferred P/E of 13.6x: Is it justified?

On Simply Wall St’s numbers, DWS Group GmbH KGaA screens as undervalued on earnings, with the stock at €67.7 and trading on a P/E of 13.6x that sits below both its peer group and an estimated fair P/E level.

The P/E ratio compares the current share price with earnings per share and is a common way investors judge how much they are paying for each euro of profit. For an asset manager like DWS Group GmbH KGaA, this lens ties directly to fee based profitability and how the market is weighing its earnings record against expectations for future cash generation.

Here, the gap is clear. DWS is described as good value versus the peer average P/E of 15.6x and the German Capital Markets industry average P/E of 14.5x, and also against an estimated fair P/E of 21.2x that the market could move towards if sentiment and assumptions stay aligned with that model.

Explore the SWS fair ratio for DWS Group GmbH KGaA

Result: Price-to-Earnings of 13.6x (UNDERVALUED)

However, investors also need to weigh risks such as DWS Group GmbH KGaA’s declining annual revenue and any shift in sentiment around the possible Deutsche Asset Management rebrand.

Find out about the key risks to this DWS Group GmbH KGaA narrative.

Another view on DWS Group GmbH KGaA’s value

The earnings based view presents DWS Group GmbH KGaA as attractively priced, but the SWS DCF model goes further, putting fair value at €125.22 per share versus the current €67.7. That is a large gap, so the real question is whether you trust the cash flow assumptions that sit behind it.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out DWS Group GmbH KGaA for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 211 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With DWS Group GmbH KGaA showing both strong recent returns and lingering questions around risks and the rebrand, it is worth checking the underlying data yourself and deciding quickly whether the balance of upside and downside fits your approach, starting with the 4 key rewards and 1 important warning sign

Looking for more investment ideas beyond DWS Group GmbH KGaA?

If DWS Group GmbH KGaA has sharpened your focus on valuation and quality, do not stop here; widen your watchlist with targeted stock ideas that fit your style.

- Target resilient cash generators by scanning companies with strong balance sheets and fundamentals using the solid balance sheet and fundamentals stocks screener (419 results).

- Hunt for quality at a reasonable price by reviewing the 211 high quality undervalued stocks before the market fully prices them in.

- Prioritise stability and defence by checking out the 291 resilient stocks with low risk scores that aim to keep drawdowns in check.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com