Will FirstCash’s (FCFS) Analyst Upgrade Amid Insider Selling Recast Its Valuation Narrative?

- Recently, FirstCash Holdings was upgraded to a Zacks Rank #2 rating, reflecting analysts’ higher earnings estimates and improved expectations for its underlying business performance.

- This shift in analyst sentiment, coming alongside earlier insider share sales and questions about valuation, highlights contrasting signals investors may weigh when assessing the company.

- With rising earnings estimates underpinning the analyst upgrade, we’ll now examine how this development influences FirstCash Holdings’ broader investment narrative.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

What Is FirstCash Holdings' Investment Narrative?

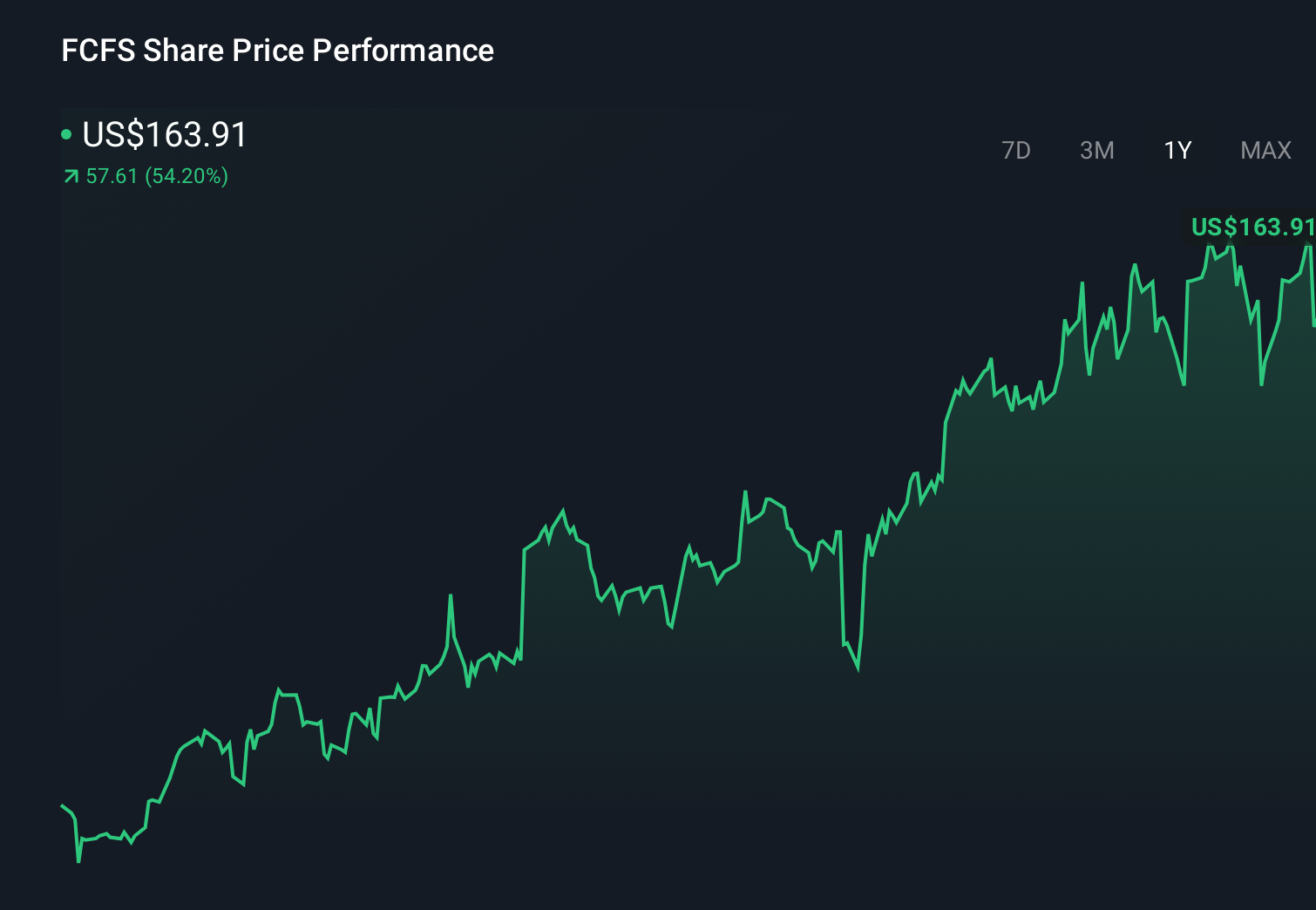

To own FirstCash, you have to be comfortable backing a mature, debt-fueled specialty finance business that pairs steady pawn and retail cash flows with shareholder returns via dividends and buybacks. Recent results showed rising revenue, expanding net income and ongoing capital returns, but also a rich earnings multiple and a balance sheet that leans on sizeable unsecured borrowings. The fresh Zacks Rank #2 upgrade, driven by higher earnings estimates, slightly strengthens the near-term earnings momentum story ahead of the next quarterly report, even as the share price has pulled back a bit after a strong run. At the same time, the earlier insider sales and third-party views that the stock screens as expensive suggest that, while the rating change is supportive, it probably does not remove valuation or leverage as key risks.

However, one risk in particular is something investors should be aware of before getting comfortable. FirstCash Holdings' share price has been on the slide but might be dropping deeper into value territory. Find out whether it's a bargain at this price.Exploring Other Perspectives

Explore 3 other fair value estimates on FirstCash Holdings - why the stock might be worth as much as 9% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your FirstCash Holdings research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free FirstCash Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate FirstCash Holdings' overall financial health at a glance.

Seeking Other Investments?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com