BNP Paribas (ENXTPA:BNP) Stock Looks Reasonable After Its 188% Five Year Run

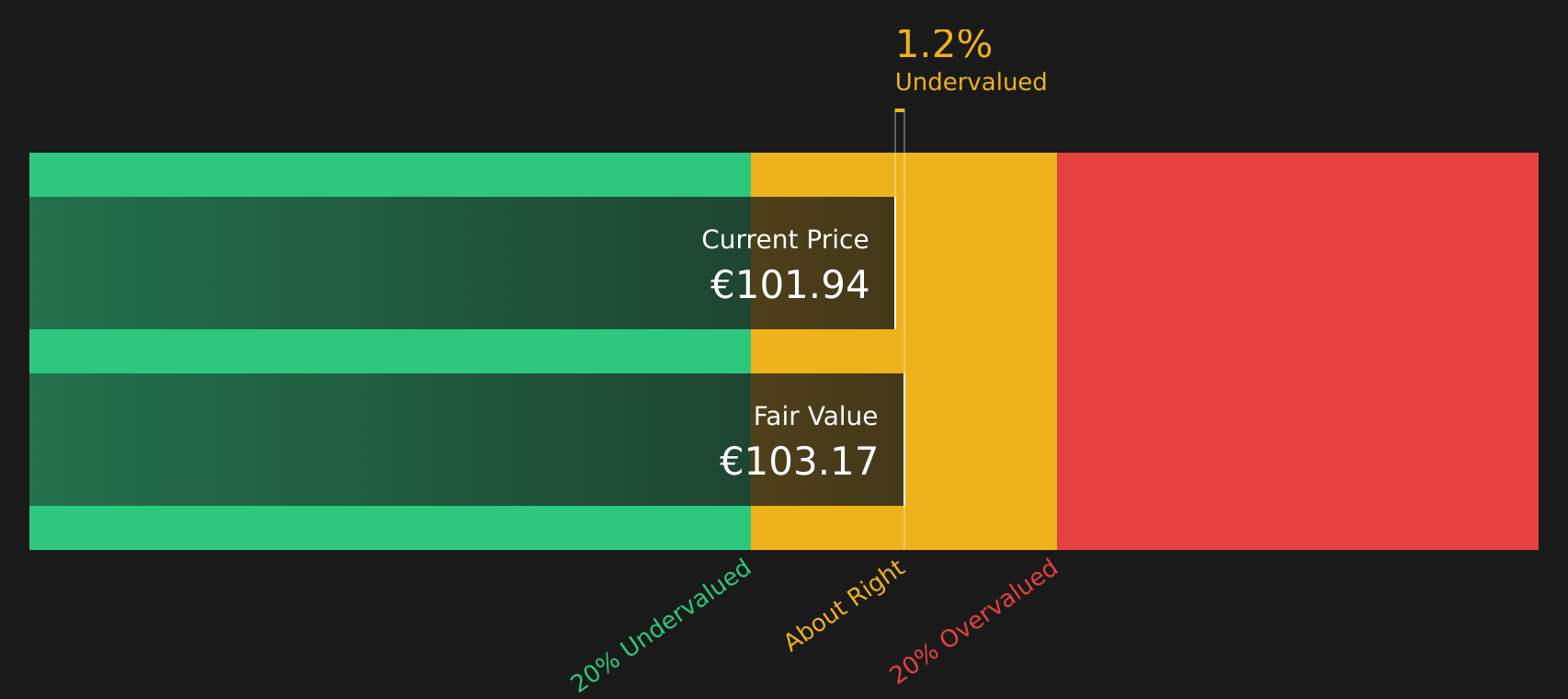

BNP Paribas stock has delivered a strong 188.3% return over the past 5 years, and at around €100.7 per share the valuation checks now suggest it is closer to fairly priced than obviously cheap, with the Excess Returns intrinsic value estimate pointing to only a small discount while market multiples look about right.

- Over 5 years, shareholders have seen a 188.3% total return, which sets a high bar for any further upside case.

- On the supportive side, BNP Paribas may benefit from the Federal Reserve lifting a long running enforcement action, while regulators' focus on AI driven cyber risk highlights a potential cost and risk factor for large banks' future profitability.

- With a mixed valuation score of 4 out of 6, the broader checks point to a middle ground rather than a clear bargain or clear overvaluation.

The issue now is whether BNP Paribas offers enough valuation upside after such a strong multi year run, given that both the intrinsic value estimate and the market's pricing are broadly in the same ballpark.

Where Does BNP Paribas Sit on Excess Returns?

Excess Returns estimates what BNP Paribas is worth by comparing the returns it can earn on its equity to the required return that shareholders expect. For BNP Paribas, the model uses a Book Value of €118.27 per share and a Stable EPS of €13.07 per share, against a Cost of Equity of €14.72 per share. That gap leads to an excess return of €1.65 per share in the negative direction, which signals that forecast returns on equity, at an average of 11.08%, are close to but below the model’s required level.

Feeding these inputs into Excess Returns produces an intrinsic value estimate of €101.49 per share, only slightly above the current share price of about €100.70. On this basis, the stock screens as roughly 0.8% undervalued. The Stable Book Value input of €117.95 per share underlines that the model is treating BNP Paribas as a mature bank with relatively steady capital and earnings rather than a high growth story. Because the Federal Reserve’s decision to end its long running enforcement action removes a specific regulatory overhang, it helps explain why the share price now sits so close to the model’s intrinsic value estimate.

Overall, the Excess Returns work up suggests BNP Paribas stock is trading at about fairly valued levels with only a very small implied discount.

BNP Paribas is fairly valued according to our Excess Returns, but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Where Does BNP Paribas Sit on Earnings?

The P/E ratio is a useful way to think about what you are paying for each euro of BNP Paribas earnings. BNP Paribas currently trades on a P/E of about 9.4x, compared with an industry average of roughly 11.6x and a peer group average near 13.1x, so the stock sits at a discount to both wider banking peers and closer comparables.

On a more tailored view, the Fair P/E Ratio for BNP Paribas is estimated at 9.7x. This is based on factors such as its size, profitability profile and risk characteristics within the Banks sector. That is only slightly above the current 9.4x, suggesting the market price is very close to what this framework indicates, rather than signaling a clear bargain or an expensive outlier.

Overall, BNP Paribas appears roughly fairly valued on its P/E multiple, with only a modest gap to the modelled fair ratio.

See what the numbers say about this price — find out in our valuation breakdown.

The BNP Paribas Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where BNP Paribas' valuation puzzle leaves off by spelling out which paths for future growth, margins and earnings would need to occur for the stock to be worth materially more or less than today’s price. Each Narrative links a specific set of catalysts and risks to a single fair value outcome, so you can track over time which version of BNP Paribas' story appears to be unfolding on the Community page.

Share a Narrative in the Simply Wall St community to set out your numbers-based view on whether developments like the Federal Reserve ending its enforcement action and the ECB's focus on AI powered cyber risk justify BNP Paribas' current pricing. It is a way to put your thesis on record and see how it stacks up as new results and regulatory updates arrive.

Do you think there's more to the story for BNP Paribas? Head over to our Community to see what others are saying!

The Bottom Line

For BNP Paribas, both the Excess Returns intrinsic value estimate and the P/E workup indicate that the stock is roughly in line with what current fundamentals support, with only a very small implied discount. The broader checks are mixed rather than strongly one sided, so the valuation case is no longer about a clear mispricing and more about modest fine tuning around fair value. From this point, the key question is whether profitability and risk costs, including regulatory and cyber related pressures, evolve in a way that keeps returns on equity comfortably aligned with what the current price already assumes.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com