Does Strong Revenue But Softer Net Interest Income Reshape The Bull Case For Old National Bancorp (ONB)?

- In the recent past, Old National Bancorp reported quarterly revenue of US$702.7 million, up 44.3% year on year but slightly below analyst estimates, with net interest income missing forecasts while earnings per share matched expectations.

- This combination of robust top-line growth, softer core banking income, and management’s emphasis on disciplined execution has highlighted how Old National is balancing expansion with profitability pressures in a competitive regional banking landscape.

- Now we’ll consider how the revenue growth alongside weaker net interest income shapes Old National Bancorp’s existing investment narrative and assumptions.

Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

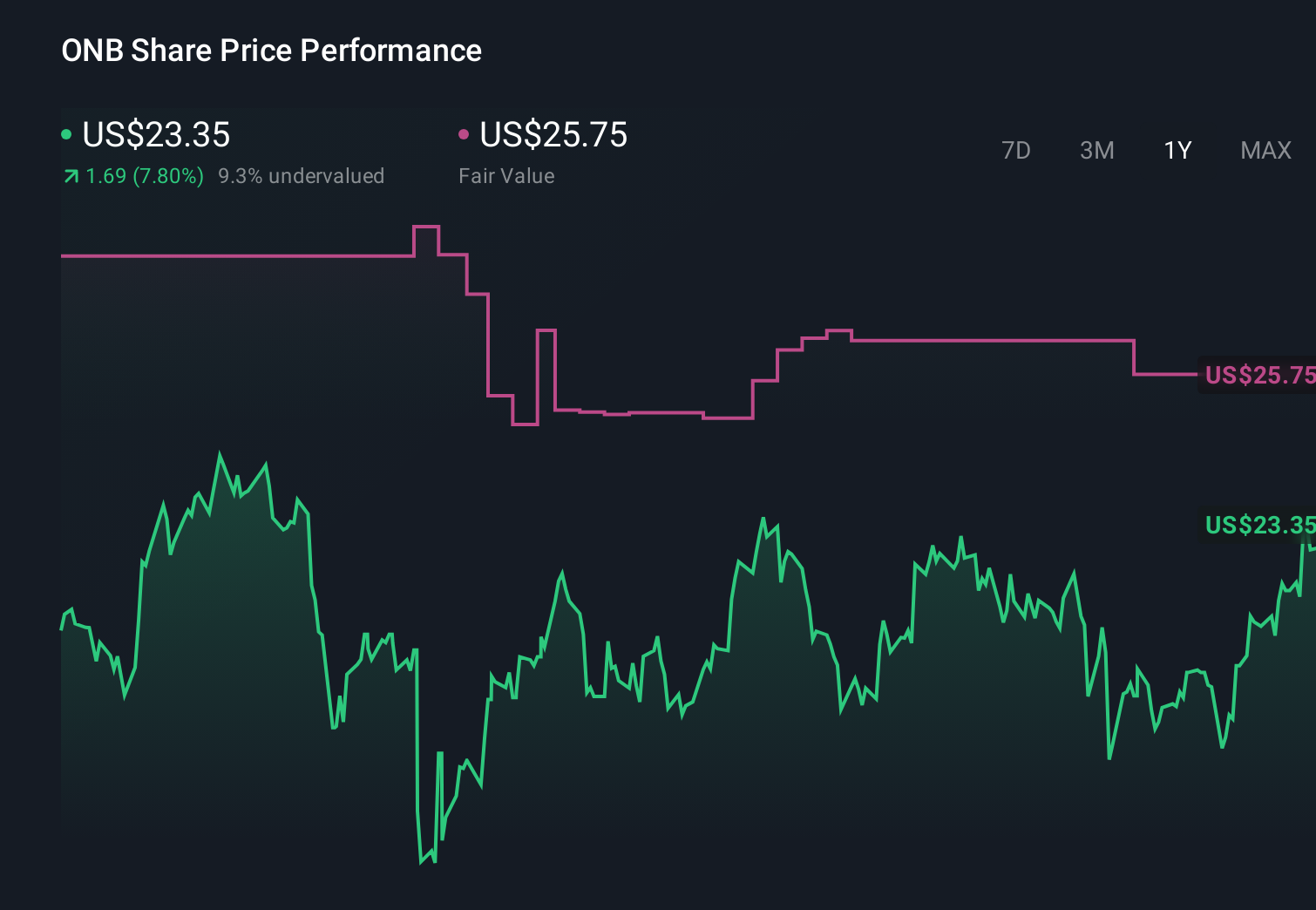

Old National Bancorp Investment Narrative Recap

To own Old National Bancorp, you need to believe in its ability to grow as a regional bank while managing credit, margin, and regulatory pressures. The latest quarter’s strong revenue but softer net interest income does not materially change the near term catalyst of integrating acquisitions and expanding fee income, nor the key risk around its sizable commercial real estate exposure.

Among recent announcements, the Q1 2026 earnings release, paired with management’s framing of a “disciplined” start to the year, directly connects to these catalysts by showing how Old National is trying to balance higher revenues with margin pressure and credit costs in practice.

Yet, despite this progress, investors should still pay close attention to Old National’s concentrated commercial real estate exposure and how it could...

Read the full narrative on Old National Bancorp (it's free!)

Old National Bancorp's narrative projects $3.4 billion revenue and $1.4 billion earnings by 2029.

Uncover how Old National Bancorp's forecasts yield a $28.00 fair value, a 7% upside to its current price.

Exploring Other Perspectives

Three Simply Wall St Community fair value estimates for Old National Bancorp span from US$28 to over US$12,000, showing just how far apart individual views can be. When those opinions sit alongside concerns about commercial real estate concentration and potential credit losses, it becomes even more important to compare several perspectives before deciding how this bank might fit into your portfolio.

Explore 3 other fair value estimates on Old National Bancorp - why the stock might be a potential multi-bagger!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Old National Bancorp research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Old National Bancorp research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Old National Bancorp's overall financial health at a glance.

Contemplating Other Strategies?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com