3 Large Cap Value Stocks Trading Below Fair Value Today

With inflation readings easing in several major economies, bond yields reacting to every move in oil, and industrial data pointing to softer but still active global growth, many stocks are being priced more on fear than on fundamentals. That is where high quality undervalued stocks can stand out. This screener focuses on companies with healthy cash flows and balance sheets that markets may be overlooking. In this article, you will see 3 stocks from the High Quality Undervalued Stocks screener that illustrate how solid businesses can still trade at appealing valuations in a choppy macro backdrop.

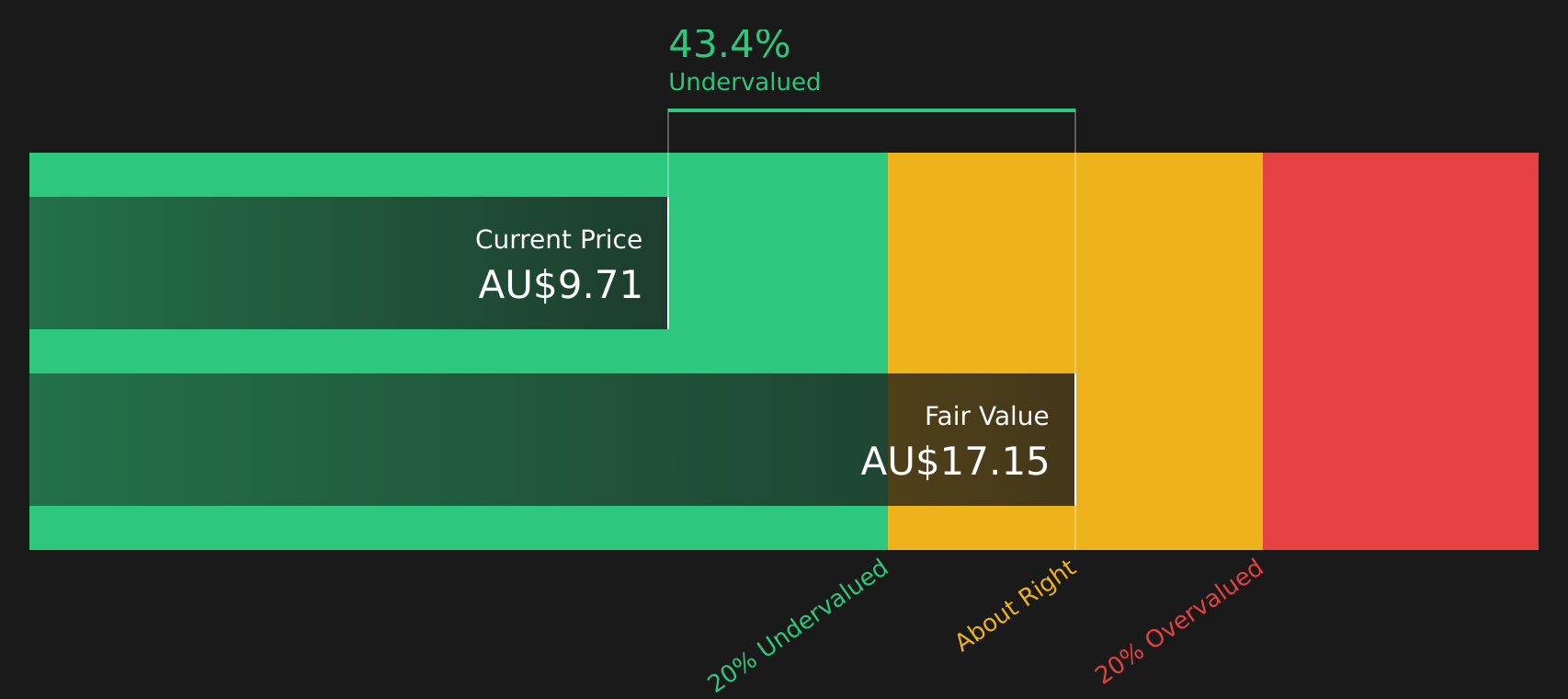

Magellan Financial Group (ASX:MFG)

Overview: Magellan Financial Group is an Australia based investment manager that runs funds focused on global equities and global listed infrastructure for clients around the world, aiming to earn management and performance fees from those portfolios.

Operations: Magellan Financial Group generates most of its A$231.9 million in business revenue from Investment Management Services, with smaller contributions from Partnerships & Investments at A$45.7 million and Corporate activities at A$6.3 million. Australia & New Zealand is its largest geographic market at A$193.8 million in revenue.

Market Cap: A$1.84b

Magellan Financial Group stands out on this screener because the market appears cautious about fee pressure, client outflows and a relatively new leadership team, yet the stock trades well below one estimate of fair value while still offering high quality earnings and a dividend yield of 8.7%. New CEO and board appointments, growing partnerships such as Vinva and an expansion tilt toward North America and Europe give the business levers to rebuild client trust and support revenue, even as management fees and margins come under pressure. For investors willing to weigh those risks against the balance sheet strength and revenue growth forecasts, the real question is how the story looks when all of these moving parts are put into one valuation picture.

Magellan Financial Group’s lowly priced stock and 8.7% yield suggest many investors may be missing the full picture. The real twist often becomes clearer when you review everything in the 3 key rewards and 1 important warning sign

Xero (ASX:XRO)

Overview: Xero is a Wellington headquartered software company that provides cloud based accounting, payroll, payments and tax tools for small businesses and their advisors, tying together products like Planday, Hubdoc, Syft, Melio and TaxCycle into one financial operating system.

Operations: Xero generates NZ$2.75b in business revenue from providing online solutions for small businesses and their advisors, with geographic exposure across Australia, New Zealand, the United Kingdom, the United States and the Rest of the World.

Market Cap: A$12.52b

Xero sits at the centre of small business finances, combining high gross margins of about 88% with an ecosystem of AI powered tools such as JAX, Industry Benchmarks and deep integrations with Microsoft 365 and Anthropic Claude that aim to automate cash flow, reporting and day to day workflows. At the same time, investors need to weigh recent margin compression, earnings that declined 26.5% in the past year and a high P/E near 90x against forecasts for earnings growth and a sizeable revenue base of NZ$2,753.08m. For anyone interested in how productivity gains, AI agents and subscription scale could relate to those risks, Xero’s setup on this screener may warrant a closer look.

Xero’s high P/E and recent earnings decline suggest the story is stalling. However, its AI tools and subscription engine tell a different story that the analyst forecasts for Xero hints at but does not fully explain.

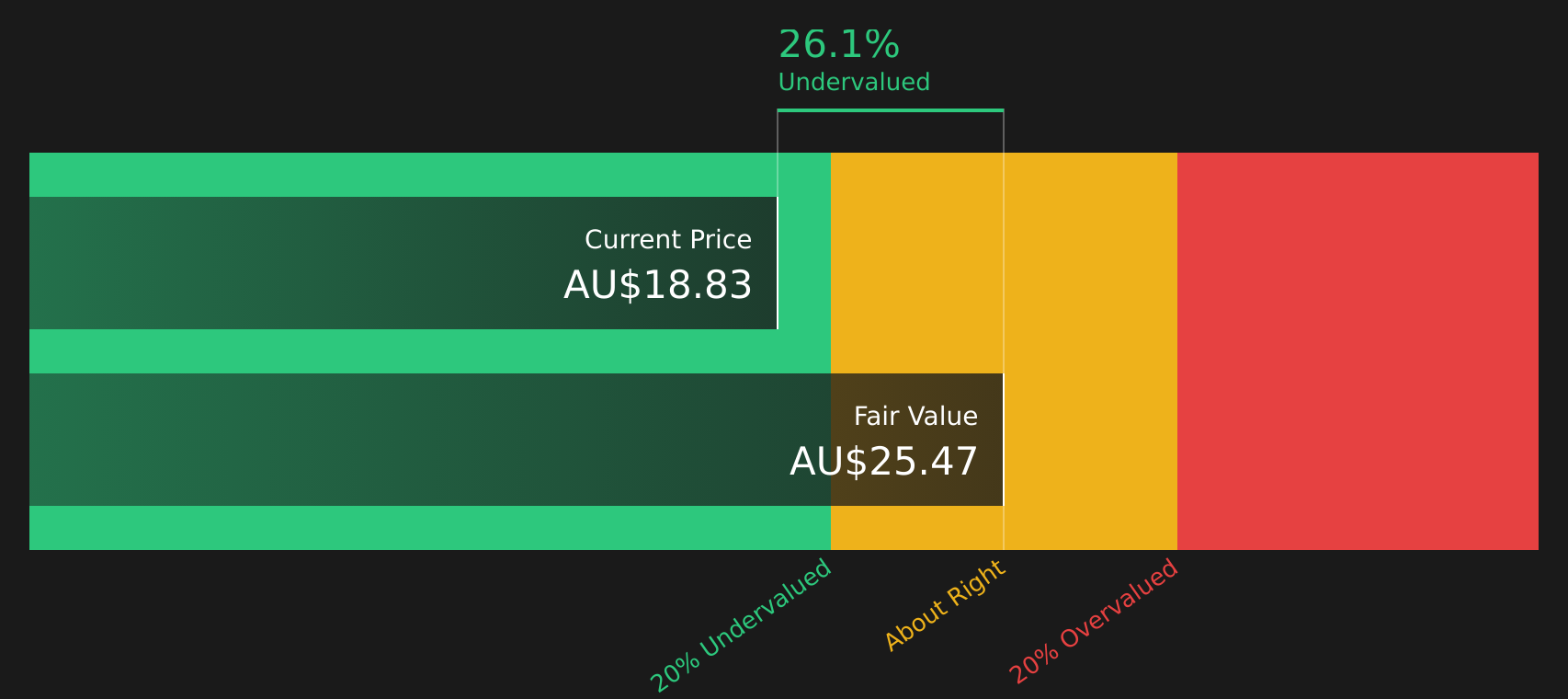

Sandfire Resources (ASX:SFR)

Overview: Sandfire Resources is an Australian mining company that explores for, develops and operates copper focused projects, with additional exposure to gold, silver, lead and zinc across its portfolio.

Operations: Sandfire Resources generates most of its revenue from the MATSA Copper Operations at about $719.7 million and the Motheo Copper Project at about $548.6 million, with smaller contributions from Exploration and Other activities at about $21.6 million.

Market Cap: A$8.88b

Sandfire Resources is on investors’ radar because it combines high quality copper assets, such as MATSA in Spain and Motheo in Botswana, with improving earnings, rising profit margins and a focus on cost control and debt reduction, yet still trades below one estimate of its future cash flow value. At the same time, the stock carries a rich P/E and depends on major projects hitting volume and cost targets while managing inflation, heavy capital spending and ESG and jurisdiction risks. If you are looking for a copper focused stock where earnings growth potential and balance sheet repair are pulling against valuation and funding questions, there is more to Sandfire’s story than the headline multiples suggest.

Sandfire Resources appears to be a copper story the market has not fully priced, with project execution and funding questions often masking the bigger picture you will see in the analysis report for Sandfire Resources

The 3 stocks covered here are only a sample of what this idea turns up, as the full High Quality Undervalued Stocks screener has identified 7 more companies with equally compelling setups across cash flows, balance sheets and potential breakout catalysts, all available through the High Quality Undervalued Stocks screener. By using Simply Wall St, you can analyze and filter for the specific catalysts and narratives discussed here so you can focus on the highest conviction opportunities rather than scrolling through hundreds of stocks.

Take Control of Your Investment Journey

If Xero or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly?

Fresh stock ideas can move from quiet to breakout quickly. The best entries often appear while they are still under the radar for now, get in early.

- Spot income workhorses with staying power by scanning our curated pool of 6 dividend fortresses designed for investors who want yields that work as hard as they do.

- Track powerful trends in automation by reviewing 30 robotics and automation stocks where selected companies are pushing robotics and efficiency tools that could reshape how entire industries operate.

- Zero in on stability first by filtering for the list of solid balance sheet and fundamentals (20 results) so you focus on companies where financial strength backs every growth story.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com