Hudbay Minerals (TSX:HBM) Stock May Be 19% Undervalued As Constancia Permit Expands

After a very large 332.8% return over the past three years, Hudbay Minerals now sits at a point where its recent rally, a mixed overall value score, and an intrinsic value estimate from a Discounted Cash Flow (DCF) model suggesting the stock trades below that estimate all pull in slightly different directions.

- Hudbay Minerals has delivered a very large 332.8% return over three years, which puts extra focus on whether the current share price still leaves room for further upside.

- The recent approval to increase mill throughput at the Constancia mine in Peru can support expectations for sustained copper output. At the same time, execution and regulatory risks around expanding production remain important for how investors price the stock.

- With a value score of 4 out of 6, Hudbay Minerals screens as a mixed picture rather than a clear bargain or clear overvaluation on the broader checks.

The stock's next move may depend on whether the current price already reflects the intrinsic value signalled by the Discounted Cash Flow (DCF) estimate or still leaves a margin between market price and that intrinsic value.

Is Hudbay Minerals Still Cheap on Cash Flow?

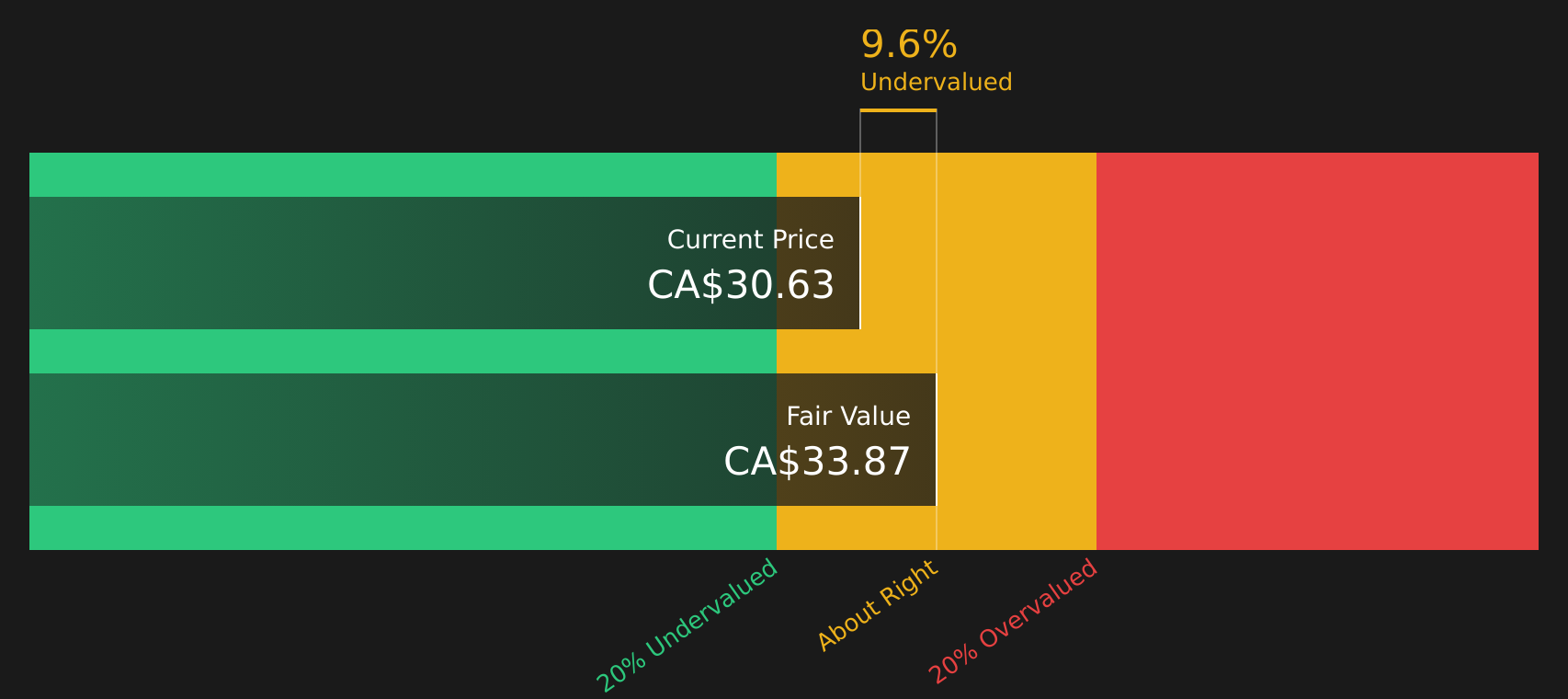

The Discounted Cash Flow (DCF) method estimates what Hudbay Minerals could be worth based on the cash it is expected to generate for shareholders. The model uses latest twelve-month free cash flow of about $358.8 million and assumes cash flows grow from current levels before settling into a steadier pattern, which fits a company with producing assets and defined expansion projects. On that basis, the DCF indicates an intrinsic value of around CA$37.65 per share.

Compared with the current share price, this implies the stock screens about 18.9% undervalued on a cash flow basis. Because the recent approval to increase mill throughput at the Constancia mine raises the potential for sustained copper output, it helps explain why investors are paying closer attention to whether Hudbay Minerals’ share price still sits below this intrinsic value estimate. Overall, the DCF workup indicates that, under the assumptions used, Hudbay Minerals appears undervalued relative to the cash flows currently built into the model.

Our Discounted Cash Flow (DCF) analysis suggests Hudbay Minerals is undervalued by 18.9%. Track this in your watchlist or portfolio, or discover 6 more high quality undervalued stocks.

Does Hudbay Minerals Look Fairly Valued on Earnings?

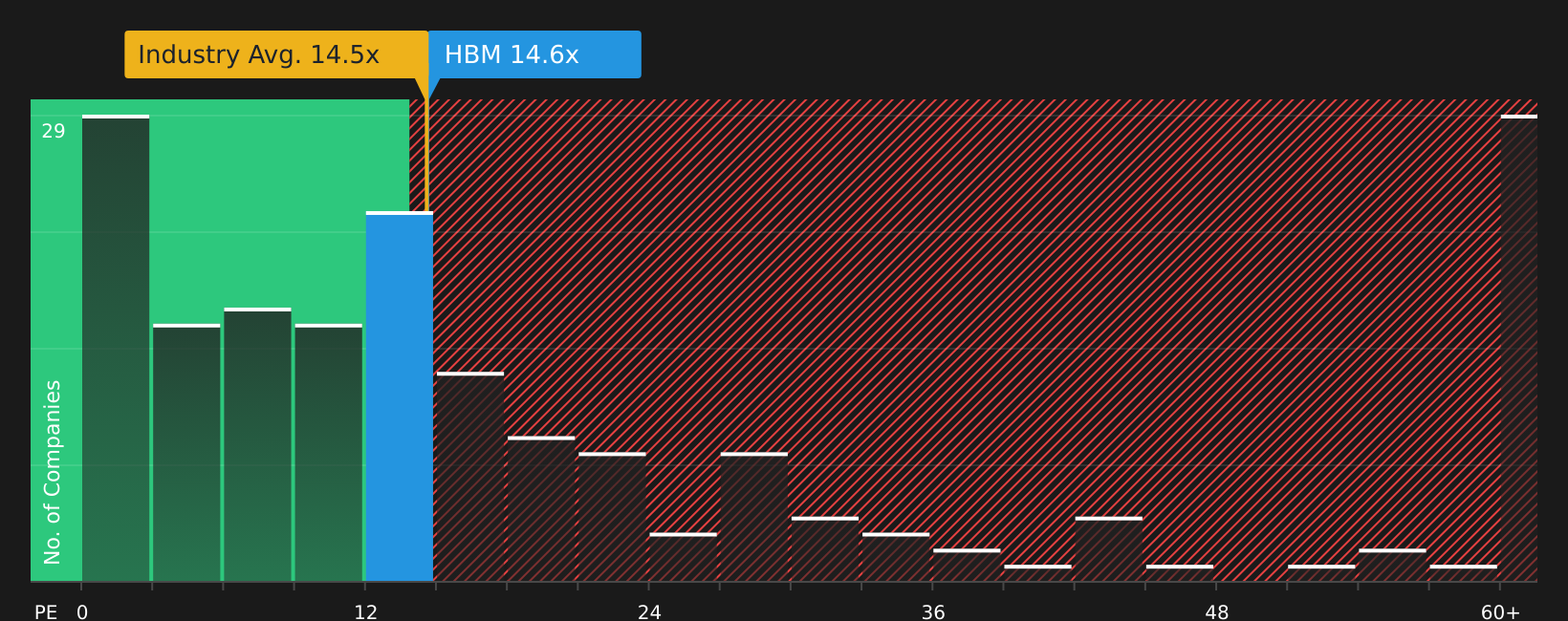

P/E is one of the clearest ways to compare Hudbay Minerals with other copper and mining stocks because it links the current share price directly to reported earnings. Hudbay Minerals trades on a P/E of about 13.0x, which sits slightly below the Metals and Mining industry average of roughly 14.5x and also below the broader peer group near 18.4x.

The fair P/E ratio for Hudbay Minerals, based on factors such as its size, profitability profile and sector, is estimated at about 12.5x, which is very close to where the stock currently trades. That small gap suggests the market is pricing Hudbay Minerals at roughly the level implied by its earnings, with neither a clear discount nor a clear premium emerging from this single metric.

On the P/E multiple, Hudbay Minerals stock appears to be trading at a level that is roughly in line with what its earnings profile would suggest.

See what the numbers say about this price — find out in our valuation breakdown.

The Hudbay Minerals Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Hudbay Minerals connect the valuation puzzle above with clear, scenario based assumptions about Hudbay Minerals' future growth, margins and earnings. They show what would need to hold for the stock to be worth materially more or less than today's price on the Community page. Instead of leaving you with a single output from a ratio or model, they break out the future that figure relies on so you can watch how reality lines up over time.

The community is split on Hudbay Minerals, with one camp focused on copper led growth potential and the other worried about how much risk is now tied to a handful of big projects.

Bull case: 43% undervalued

"Once Copper World is operating, Hudbay expects annual copper output to be more than 50% above current levels, with over 70% of consolidated production and revenue coming from copper..."

Read the full Bull Case to see why Hudbay Minerals could be undervalued

Bear case: 22% overvalued

"The Copper World joint venture with Mitsubishi concentrates future capital and execution risk into a single large United States project..."

Read the full Bear Case to see why Hudbay Minerals could be overvalued

Do you think there's more to the story for Hudbay Minerals? Head over to our Community to see what others are saying!

The Bottom Line

For Hudbay Minerals, the Discounted Cash Flow (DCF) work suggests the stock could be undervalued, while the P/E multiple points to pricing that is about right relative to peers. That gap mainly reflects how the intrinsic value model leans on future cash flows from current and planned projects, whereas the market multiple is more tightly linked to sentiment and where similar stocks trade today.

With broader checks painting a mixed picture, the key question is whether execution and regulatory risk on its major projects, especially Copper World and Constancia, are being overestimated or whether that apparent discount is simply the market pricing those risks correctly.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com