eToro (ETOR) Stock Looks Priced Above Fair Value After Its 32% Fall

eToro Group stock sits in an awkward spot for valuation focused investors. The Excess Returns intrinsic value estimate indicates the shares trade at a premium, while the market multiples still screen as inexpensive, all against a 1 year share price that has fallen 32.1%.

- Over the past year, eToro Group is down 32.1%, which means anyone buying today is looking at a stock that has already retraced significantly from previous levels.

- Recent coverage highlighting strong price momentum and a low P/S ratio may support the case that improving sentiment around the core trading platform can help sustain the current valuation, but the crypto related backdrop leaves the stock exposed if risk appetite weakens again.

- With a value score of 2 out of 6, eToro Group does not screen as a clear bargain on the broader valuation checks, even though some multiples look appealing.

The issue now is whether the intrinsic value premium or the apparently cheap multiples turn out to be the better guide to where eToro Group stock should trade.

Find out why eToro Group's -32.1% return over the last year is lagging behind its peers.

Does eToro Group Look Pricey on Excess Returns?

The Excess Returns model looks at how efficiently eToro Group turns its equity base into profits after covering the required return for shareholders. It uses book value, earnings power and the cost of equity to estimate what the shares might be worth.

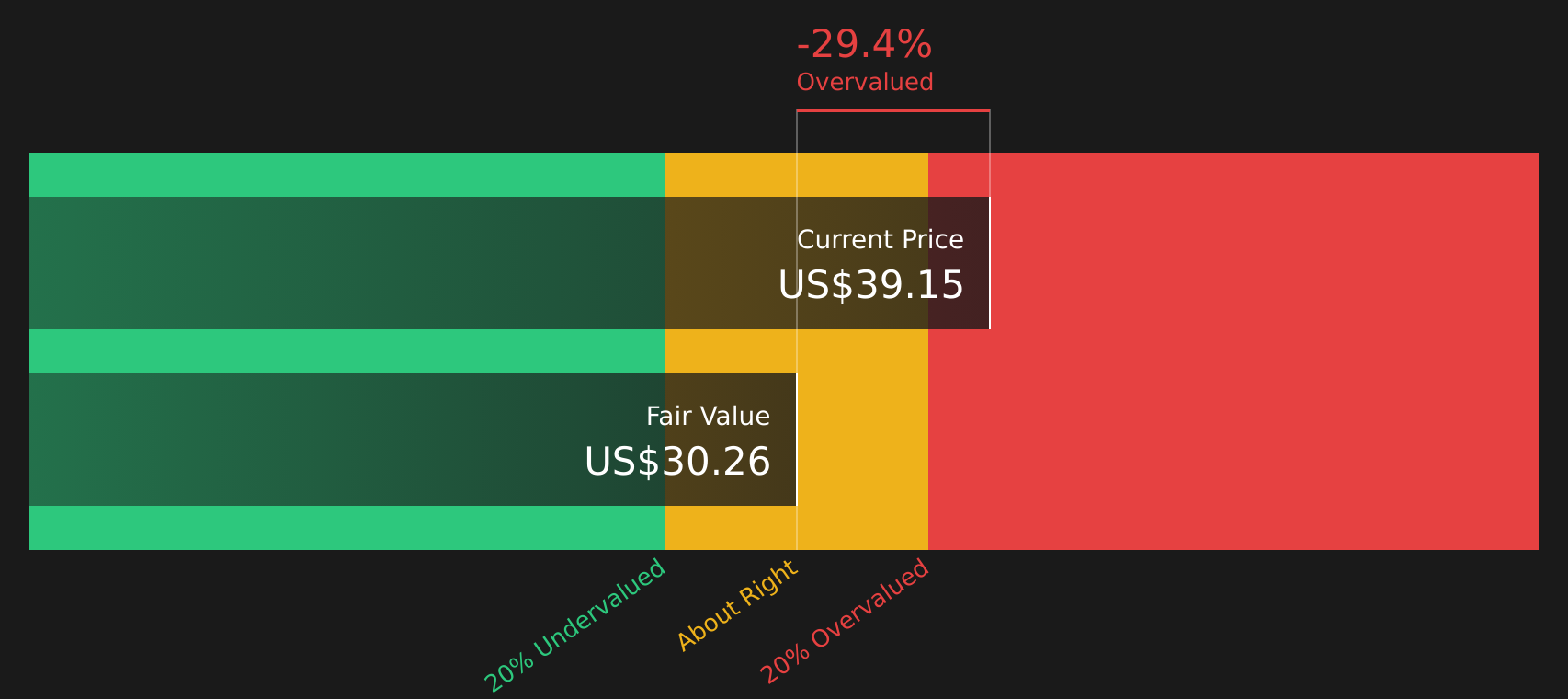

For eToro Group, the model works off a Book Value of $16.36 per share and Stable EPS of $2.39 per share, based on the median return on equity over the past 5 years. With a Cost of Equity of $1.56 per share, the model derives an Excess Return of $0.83 per share on an Average Return on Equity of 14.59%, assuming a Stable Book Value of $16.36 per share. This cash generation relative to the equity base feeds into an intrinsic value estimate of $30.24 per share. This sits below the current share price and implies the stock is 29.4% overvalued on this framework.

Recent commentary around strong share price momentum and a low P/S ratio helps explain why the market price stands above what the Excess Returns model supports.

On these Excess Returns assumptions, eToro Group stock currently screens as overvalued.

Our Excess Returns analysis suggests eToro Group may be overvalued by 29.4%. Discover 44 high quality undervalued stocks or create your own screener to find better value opportunities.

Does eToro Group Look Undervalued on Earnings?

The P/E ratio is a useful way to see what you are paying for each dollar of eToro Group earnings. eToro Group trades on a P/E of 13.1x, which sits well below the broader Capital Markets industry average of 40.9x and also below the peer group average of 3.9x cited for its direct comparison set.

The tailored fair P/E ratio for eToro Group is 16.7x, based on its earnings profile, industry, size and risk inputs. Against that benchmark, the current 13.1x suggests the stock trades at a discount to what this framework indicates would be reasonable, taking into account sector specific risks and the crypto related backdrop discussed earlier.

On the P/E multiple, eToro Group stock currently appears undervalued relative to the earnings level that the fair ratio would indicate.

See what the numbers say about this price — find out in our valuation breakdown.

The eToro Group Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for eToro Group pick up where this valuation puzzle leaves off. They spell out which combinations of future growth, margins and earnings would need to hold for the stock to be worth materially more or less than today’s price, and they sit on Simply Wall St’s Community page. Each narrative treats eToro Group's fair value as a thesis about the business that you can revisit over time, rather than a one off snapshot.

Add your voice to the Simply Wall St community by setting out a clear, number driven narrative on eToro Group. Include your view on whether its recent momentum profile and low P/S ratio really support today's pricing. It is a straightforward way to test your thesis in public and see how it stacks up as new results and crypto related news come through.

Do you think there's more to the story for eToro Group? Head over to our Community to see what others are saying!

The Bottom Line

For eToro Group, the Excess Returns intrinsic value estimate points to shares trading on the rich side, while the P/E based view suggests the stock screens as undervalued relative to its earnings profile. That split reflects two different lenses: the intrinsic value model focuses on the pace and efficiency of cash generation, while the multiples view is driven more by how much growth and sentiment are already baked into comparable stocks. With the broader valuation checks still weak, the key question is whether the current earnings and crypto exposed business mix are strong enough to justify a sustained re rating rather than a value trap.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com