3 Japanese AI Chip Stocks With Strong Balance Sheets

Cooling inflation in several major economies, mixed but resilient growth signals, and central banks stressing data dependence have pushed many investors toward companies with solid balance sheets and disciplined use of capital. In this setting, stocks that combine high return on equity, a history of sound execution, and robust financial foundations can offer a cleaner way to gain exposure without relying heavily on momentum or aggressive forecasts. This article focuses on our Solid Balance Sheet and Fundamentals screener and highlights 3 of the best stocks it surfaces, so you can see how this theme might fit into a long term portfolio.

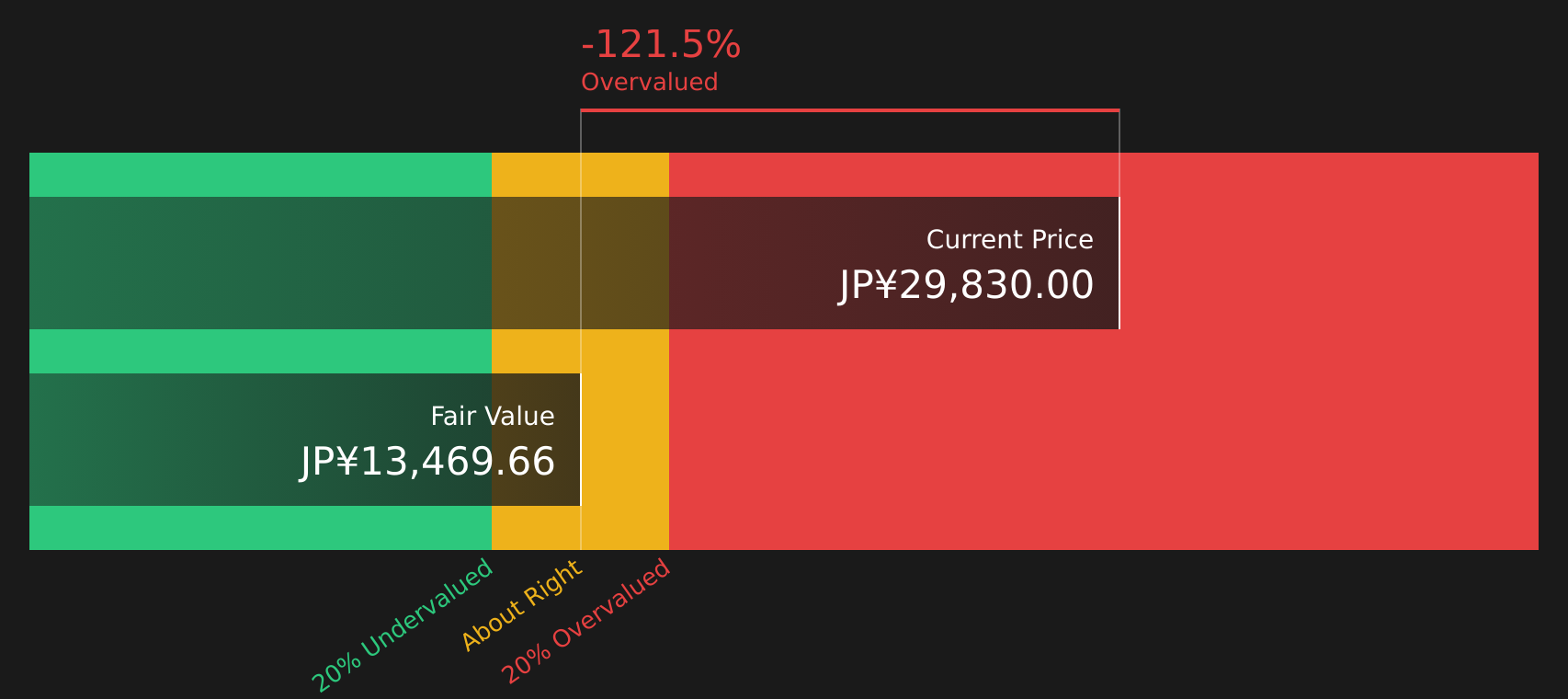

Advantest (TSE:6857)

Overview: Advantest is a Japan based supplier of semiconductor testing equipment and related software, providing system on chip, memory and power device testers, metrology tools, and cloud based test solutions that help chip makers verify increasingly complex AI and high performance computing designs.

Operations: Advantest generates the bulk of its revenue from its Test System Business at ¥1,019.4b, with an additional ¥109.2b from Services and Others across Asia, Japan, Europe and the Americas.

Market Cap: ¥21.6t

Advantest stands out because it sits at the center of AI and advanced semiconductor testing, supported by strong reported fundamentals. Earnings growth of 132.9% year over year, a 33.3% net margin and a 47.2% return on equity indicate that the business has translated sector demand into substantial profitability. Partnerships with groups such as Applied Materials and OpenLight highlight ties across cutting edge chip and photonics projects. At the same time, a premium P/E multiple, reliance on strong AI and high performance computing demand, and exposure to higher risk external funding contribute to a more complex risk profile. Understanding how these strengths and pressure points relate to each other is important for long term investors.

Advantest’s surging profitability and central role in AI testing raise a clear question: is this premium P/E fully backed by fundamentals or masking something investors are missing? Start with the DCF valuation analysis for Advantest

Trend Micro (TSE:4704)

Overview: Trend Micro is a Japan based cybersecurity company that provides software and cloud platforms to protect devices, emails, networks and data, while also offering AI driven tools and managed services that help enterprises monitor, detect and respond to threats across hybrid IT environments.

Operations: Trend Micro generates revenue across Japan at ¥87,873m, Asia Pacific at ¥77,088m, Europe at ¥65,128m and the Americas at ¥55,822m, with a segment adjustment of ¥3,574m.

Market Cap: ¥814.5b

Trend Micro gives investors exposure to cybersecurity and AI security tools through a company that already reports high profitability, including a 32.3% return on equity and net margin of 13.3%, while actively tying its TrendAI platform into partners such as OpenAI, Anthropic and Claude for threat detection and compliance. The business is focusing on higher value enterprise contracts, multiyear agreements and AI assisted cost control, but carries trade offs such as a relatively expensive P/E versus local software peers, an unstable dividend history and funding that relies fully on higher risk external borrowing. Under the surface, the shift from consumer to enterprise, the use of AI partnerships and the role of share buybacks and dividends in total shareholder returns are important considerations for long term holders.

Trend Micro’s shift toward higher value enterprise security and AI driven platforms could mean its true earnings power is not fully reflected in today’s P/E. However, the full story, including how share buybacks, dividends and that reliance on external borrowing interact, sits inside the analysis report for Trend Micro

Tokyo Electron (TSE:8035)

Overview: Tokyo Electron is a Japan based manufacturer of semiconductor production equipment, supplying tools such as coaters, etchers, cleaners and deposition systems that chip makers use to build advanced logic, memory and power devices around the world.

Operations: Tokyo Electron generates all of its ¥2,443.5b in revenue from Semiconductor Production Equipment, with sales spread across China, Taiwan, South Korea, Japan, the United States, Europe and other regions.

Market Cap: ¥33.2t

Tokyo Electron attracts interest because it sits at the heart of global chip investment, supplying equipment that is exposed to AI, cloud and broader digital transformation trends while reporting high profitability, including a 23.5% net margin and strong return on equity. Rising field solutions revenue points to growing recurring income from its installed base, and recent dividends, buyback plans and a stock split indicate a focus on shareholder returns and liquidity. At the same time, heavy China exposure, reliance on external borrowings and periods of volatile customer spending mean earnings can be sensitive to capital expenditure cycles. Investors are weighing how those quality fundamentals align with a rich valuation and mixed analyst expectations.

Tokyo Electron’s rich valuation, high margins and exposure to global chip spending suggest investors may be missing how earnings sensitivity truly plays out. The full picture sits inside the analysis report for Tokyo Electron

The three stocks highlighted here are only a starting point, as the Solid Balance Sheet and Fundamentals screener has surfaced 35 more companies with similarly compelling stories that combine high return on equity, sound balance sheets and a track record of disciplined execution, all captured inside the Solid Balance Sheet and Fundamentals screener. Use Simply Wall St to identify, filter and analyze the specific catalysts and narratives that matter most to you so you can focus on the highest conviction ideas from this group.

Take Control of Your Investment Journey

If Trend Micro or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond These Stocks

Markets move fast, and the stocks with real breakout potential rarely stay under the radar for long. Before momentum starts flying and ideal entry points get caught, act now.

- Spot under the radar growth stories by scanning 1 elite penny stocks with strong financials curated for stronger balance sheets and cleaner financial profiles than typical speculative micro caps.

- Target durable cash generators by filtering for 43 dividend fortresses that prioritize consistent income, solid coverage ratios and business models built to handle changing conditions.

- Ride structural spending trends with 34 power grid technology and infrastructure stocks that may benefit from grid modernization, electrification projects and long dated infrastructure programs worldwide.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com