Is Walker & Dunlop’s (WD) FHA Hire a Subtle Bet on Government-Backed Multifamily Financing?

- Walker & Dunlop recently announced that Frank Cassidy, former Federal Housing Administration commissioner and assistant secretary for housing at HUD, has rejoined the firm as a senior managing director to advise on FHA and GSE financing strategies across its platform.

- By bringing back an executive who oversaw approximately US$2.00 trillion in FHA mortgage insurance and wide-ranging federal housing programs, Walker & Dunlop is deepening its expertise in government-backed multifamily, affordable housing, and healthcare finance.

- We’ll now explore how Cassidy’s government housing policy experience could influence Walker & Dunlop’s investment narrative around multifamily and affordable housing growth.

Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Walker & Dunlop Investment Narrative Recap

To own Walker & Dunlop, you need to believe in sustained demand for multifamily and affordable housing finance and the value of its government-backed lending niche. The return of former FHA commissioner Frank Cassidy reinforces this FHA and GSE focus but does not materially change the near term catalyst of transaction volume recovery, nor the key risk of policy or agency cap changes that could disrupt fee income.

The recent addition of Walker & Dunlop to the Russell 2000 Dynamic Index is particularly relevant here, as it can broaden the shareholder base just as the firm highlights its FHA and GSE capabilities through Cassidy’s return. Together, index inclusion and enhanced government program expertise sit alongside institutional “dry powder” and housing undersupply as important supports for multifamily oriented growth, even as interest rate volatility and regulatory shifts remain central watchpoints.

Yet, while these strengths are encouraging, investors should be aware of how dependent the story still is on GSE policy stability and...

Read the full narrative on Walker & Dunlop (it's free!)

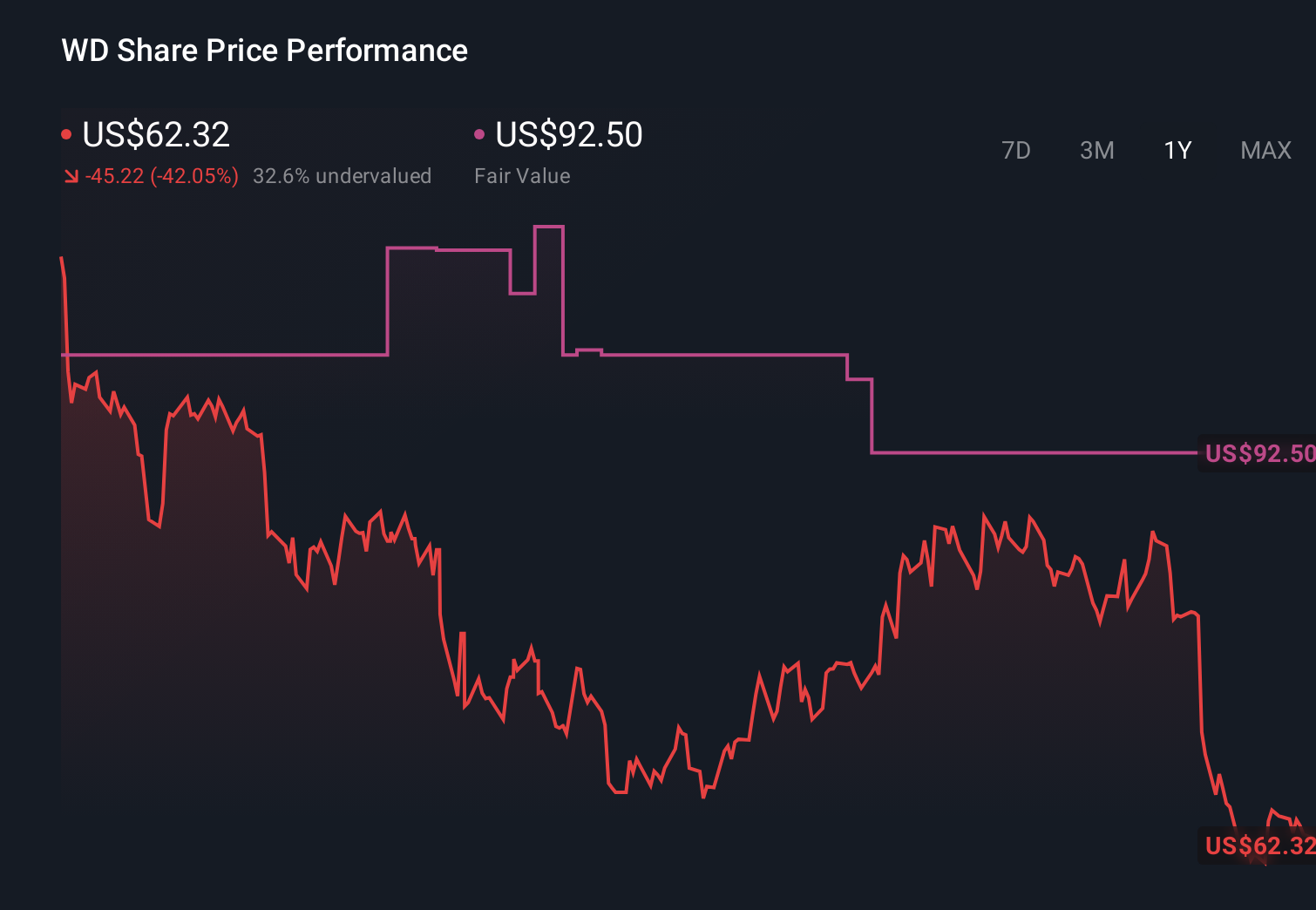

Walker & Dunlop's narrative projects $1.7 billion revenue and $211.3 million earnings by 2029. This requires 11.8% yearly revenue growth and a $143.0 million earnings increase from $68.3 million today.

Uncover how Walker & Dunlop's forecasts yield a $67.33 fair value, a 34% upside to its current price.

Exploring Other Perspectives

Three fair value estimates from the Simply Wall St Community span roughly US$31.87 to US$67.33, underscoring how far apart individual views can be. You should weigh this spread against Walker & Dunlop’s reliance on government backed multifamily and affordable housing finance, and consider how policy or rate shifts could influence the business before siding with any one outlook.

Explore 3 other fair value estimates on Walker & Dunlop - why the stock might be worth as much as 34% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Walker & Dunlop research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Walker & Dunlop research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Walker & Dunlop's overall financial health at a glance.

Looking For Alternative Opportunities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- AI is about to change healthcare. These 41 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com