Is Life Time (LTH) Using Upscale Retail Clubs to Sharpen Its Premium Wellness Positioning?

- Life Time, Inc. has recently opened its Life Time Brea Athletic Country Club in North Orange County and Life Time North Shore in Illinois, large-format athletic country clubs featuring resort-style pools, expansive pickleball facilities, recovery zones, and comprehensive family-focused wellness and fitness amenities.

- By anchoring high-traffic retail and lifestyle centers with premium, multi-generational clubs offering everything from pickleball to work lounges and kids programs, Life Time is deepening its presence in affluent, experience-driven markets that value comprehensive health and social offerings under one roof.

- We’ll now examine how these large-format openings in affluent retail hubs may influence Life Time’s investment narrative built around premium wellness expansion.

We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Life Time Group Holdings Investment Narrative Recap

To own Life Time, you need to believe its high-end, multi-generational clubs can keep filling up and spending, even as heavy capital needs and debt stay manageable. The Brea and North Shore openings support the premium wellness expansion catalyst in the near term, but they also lean into the biggest current risk: execution and financing of large, capital-intensive projects in a changing financing and consumer backdrop.

Life Time’s recent inclusion in multiple Russell value and small cap benchmarks may matter more to the near-term stock narrative than a single club opening. Index additions can influence trading volumes and ownership mix, intersecting with existing catalysts around balance sheet discipline and capital allocation, while sitting against risks tied to continued high debt levels and ongoing sale-leaseback dependence for growth funding.

Yet behind the glossy new clubs, investors should also be aware of how rising build costs and dependence on sale-leasebacks could...

Read the full narrative on Life Time Group Holdings (it's free!)

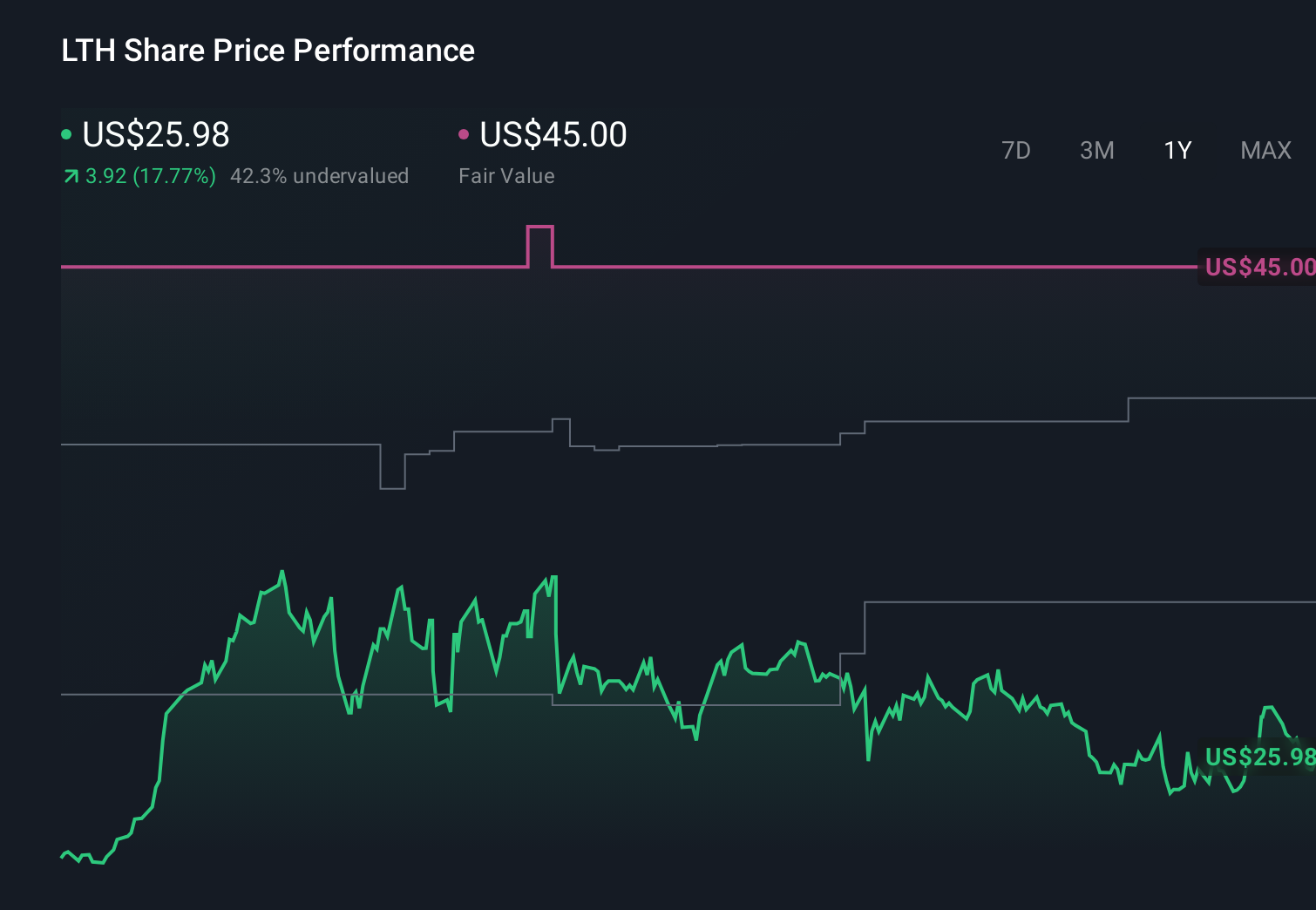

Life Time Group Holdings' narrative projects $4.2 billion revenue and $434.5 million earnings by 2029. This requires 11.1% yearly revenue growth and about a $48.9 million earnings increase from $385.6 million today.

Uncover how Life Time Group Holdings' forecasts yield a $41.00 fair value, in line with its current price.

Exploring Other Perspectives

Some of the lowest-estimate analysts were already cautious, assuming revenue of about US$4.2 billion and profit margins slipping to 10.2 percent by 2029, so these big new clubs could either ease those concerns about expansion strain or reinforce them, depending on how you think they affect cash flow and financing flexibility.

Explore 2 other fair value estimates on Life Time Group Holdings - why the stock might be worth as much as $41.00!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Life Time Group Holdings research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Life Time Group Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Life Time Group Holdings' overall financial health at a glance.

Searching For A Fresh Perspective?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com