Is DHT Holdings (DHT) Still A Bargain With Revenue And Yield In Focus?

DHT Holdings stock has delivered a very large 5-year gain, yet current valuation checks suggest the shares are not obviously stretched and may still be pricing in its strengths more conservatively than the recent performance might imply.

- Over 5 years, DHT Holdings has returned about 3.4x an initial investment, which puts extra focus on whether the current share price still lines up with its fundamentals.

- Recent coverage has highlighted strong revenue momentum and a high dividend yield as potential supports for the valuation. At the same time, reliance on tanker market conditions and geopolitical trade flows can remain a key risk for how durable those cash flows prove to be.

- DHT Holdings currently passes 5 of 6 broad valuation checks, which suggests the stock leans cheap on these measures rather than clearly expensive, according to our value score of 5.

The issue now is whether DHT Holdings' strong share price performance has already captured these supports, or if the current valuation still leaves room for further upside without assuming overly optimistic conditions.

Is DHT Holdings Fairly Priced on Earnings?

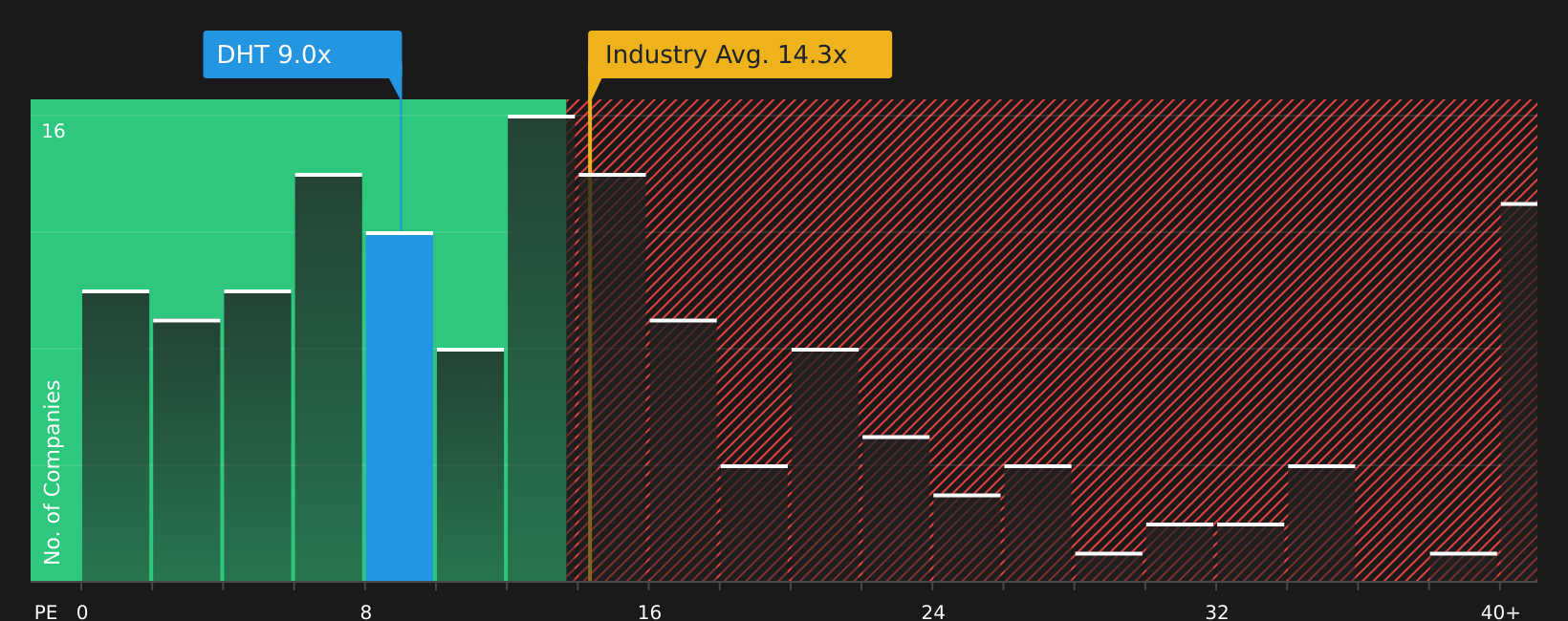

The P/E ratio is a useful way to sanity check what you are paying for each dollar of current earnings at DHT Holdings. Right now the stock trades on about 8.6x earnings, which sits well below both the Oil and Gas industry average of roughly 13.3x and a peer group average of about 14.4x.

The Fair P/E Ratio for DHT Holdings, which blends factors such as its profitability profile, risk, sector and size, sits at about 9.2x. That is only a small step above the current 8.6x level, so the market price looks broadly in line with what this framework would suggest. Despite the recent focus on stronger revenue and a high dividend yield, the shares still do not look aggressively re rated against peers on earnings.

On the P/E multiple, DHT Holdings stock looks priced roughly in line with what its earnings and risk profile would justify.

See what the numbers say about this price — find out in our valuation breakdown.

The DHT Holdings Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for DHT Holdings pick up where the P/E work leaves off by setting out the growth, margin and earnings paths that would need to hold for DHT Holdings' stock to be worth significantly more or less than today based on different assumptions. Each narrative links a specific valuation outcome to a clear story about potential catalysts and risks for DHT Holdings, so you can track over time which version appears to be playing out on the Community page.

One of the top community narratives on DHT Holdings: 51% undervalued

"DHT Holdings, Inc. maintains a high degree of spot market exposure compared to its peers, with management explicitly stating a target of approximately 70 to 75% spot market voyages exposure by Q2 2026…"

Read one of the top narratives on DHT Holdings

Do you think there's more to the story for DHT Holdings? Head over to our Community to see what others are saying!

The Bottom Line

For DHT Holdings, the current picture on earnings multiples points to a stock that looks about right rather than clearly undervalued or overvalued. The strong score across broader valuation checks suggests the market has not fully priced it as a premium tanker stock, even after a very large 5 year share price move. From here, the key question is whether tanker market conditions and trade flows stay supportive enough for DHT Holdings to keep justifying its earnings profile and dividend without the valuation slipping into value trap territory.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com