CSL Stock And 2 Australian Dividend Shares With Income That Looks More Reliable

With inflation trends mixed across regions and bond yields easing in several major markets, many investors are looking for income that feels more reliable than short term sentiment swings. The Dividend Powerhouses (3%+ Yield) screener focuses on companies paying more than a 5% dividend yield that is described as well covered, growing and stable, which can appeal if you want cash returns while policy expectations and growth signals keep shifting. In this article, you will see three stocks from this screener that stand out on dividend quality and consistency within the current global backdrop.

CSL (ASX:CSL)

Overview: CSL is a global biopharmaceutical company that develops and supplies plasma based therapies, vaccines and treatments for conditions such as immune disorders, bleeding disorders, iron deficiency and kidney disease through its CSL Behring, CSL Seqirus and CSL Vifor businesses.

Operations: CSL generates most of its revenue from CSL Behring (about US$10.9b), with additional contributions from CSL Vifor (about US$2.4b) and CSL Seqirus (about US$2.2b), and key markets including the United States, Rest of World regions and Germany.

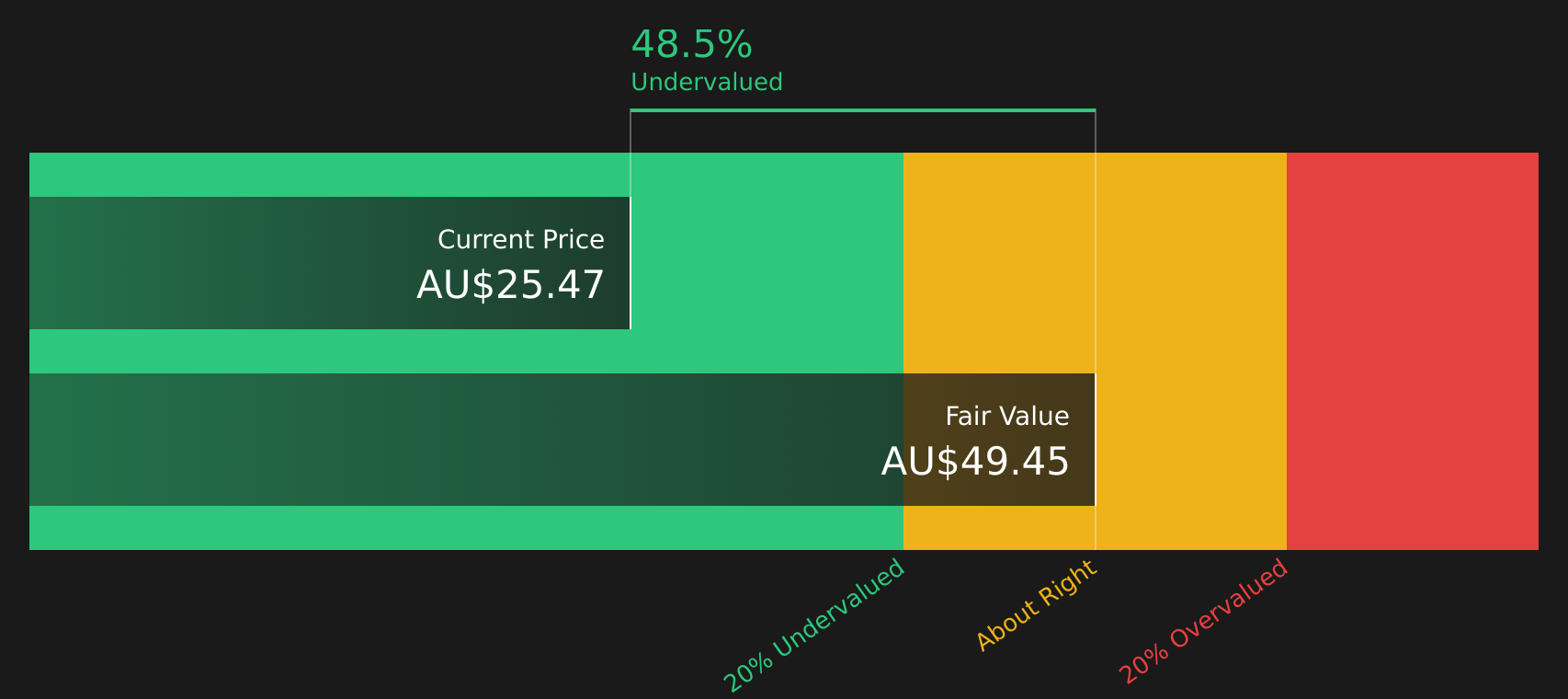

Market Cap: A$58.9b

CSL combines an essential plasma therapy network with exposure to vaccines and kidney and iron deficiency treatments. This profile may appeal to income focused investors who are also interested in long term growth potential. The company is working through restructuring and one off charges that weigh on recent margins and earnings, alongside high debt and a dividend that is not fully covered by current earnings, so the risks are material. Analysts also note forecasts that indicate faster earnings growth than the broader Australian market, and they currently see the stock trading below their estimates of fair value. The key question is whether the earnings recovery, cost savings and product pipeline can offset recent setbacks and governance churn.

CSL’s earnings recovery story appears stronger than the headline risks suggest; however, the real test is whether the cash flows, dividend cover and pipeline stack up against expectations in the analysis report for CSL

QBE Insurance Group (ASX:QBE)

Overview: QBE Insurance Group is a global insurer that underwrites general insurance and reinsurance across Australia Pacific, North America and other international markets, covering everyday risks like home, motor and health, as well as specialist areas such as agriculture, marine, energy, aviation and professional indemnity.

Operations: QBE generates most of its revenue from International operations (about US$11.2b), with further contributions from North America (about US$8.2b), Australia Pacific (about US$5.7b) and smaller corporate and other activities.

Market Cap: A$38.0b

QBE Insurance Group offers a combination of broad insurance coverage, an 18.5% return on equity and global diversification that can appeal if you want dividend income tied to a large, established insurer rather than a single domestic cycle. The stock is flagged as trading well below one estimate of fair value and has recently seen margin improvement, but investors still need to weigh softening premium rates, underwriting volatility and an unstable dividend record. At the same time, QBE is reshaping its balance sheet through debt refinancings, expanding in higher growth regions such as India and Asia, and adding experienced board and regional leaders. Together, these developments may influence how sustainable its income profile looks over the next few years.

QBE’s 18.5% return on equity and global spread hint at a stronger story than its patchy dividend record suggests, but the real twist sits inside the 2 key rewards and 1 important warning sign

Evolution Mining (ASX:EVN)

Overview: Evolution Mining is an Australia based gold producer that explores, develops and operates gold and gold copper mines in Australia and Canada, and also looks for copper and silver deposits.

Operations: Evolution Mining generates most of its revenue from Cowal (about A$1.7b) and Ernest Henry (about A$1.1b), with additional contributions from Mungari (about A$779.9m), Red Lake (about A$673.6m), Northparkes (about A$580.6m), Corporate (about A$156.5m) and Mt Rawdon (about A$153.0m).

Market Cap: A$23.6b

Evolution Mining stands out in this dividend focused list because it combines high quality earnings, a 26% net margin and a 23.6% return on equity with meaningful copper exposure and a lithium joint venture that could support more resilient cash flows than a pure gold producer. Earnings momentum has been strong, yet the stock trades on a P/E above the Metals & Mining average and revenue growth is only expected to be modest. Investors need to be comfortable that mine lives, grades and costs can keep those margins intact while funding an unstable dividend history and higher external borrowing. The Nevada North lithium project and long mine lives across the portfolio make the real story much more interesting than a simple gold price bet.

Evolution Mining’s high margins, copper leverage and lithium exposure suggest a story that is still taking shape, and the real tension between cash flow strength and dividend uncertainty sits inside the analysis report for Evolution Mining

If these three income ideas caught your eye, they are just a small slice of the opportunity set, with the full Dividend Powerhouses screen surfacing 27 more companies that show similarly compelling dividend stories and business narratives in the Dividend Powerhouses (3%+ Yield) screener. Use Simply Wall St to identify and analyze the specific catalysts, dividend profiles and narrative drivers that matter to you so you can focus on the highest conviction income plays.

Take Control of Your Investment Journey

If QBE Insurance Group or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before The Window Closes?

Fresh stock ideas can move from quiet to breakout quickly, and once momentum is flying you risk getting caught late. Scan these curated lists while it matters, act now.

- Spot potential turnarounds early by tracking 59 elite penny stocks with strong financials that pair tiny market caps with screens for stronger balance sheets and cleaner earnings profiles than typical speculative micro caps.

- Ride structural shifts in computing by reviewing 26 quantum computing stocks featuring companies screened for real exposure to quantum hardware, software and enabling technologies still under the radar for now.

- Lock onto powerful secular themes by assessing 52 AI infrastructure stocks where capital heavy enablers of AI demand, from chips to data centers, are filtered for financial resilience and business quality, so consider these opportunities while they are still emerging.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com