Will IMCD’s (ENXTAM:IMCD) E‑Sports Nutrition Push at IFT FIRST 2026 Recast Its Growth Narrative?

- IMCD Group recently showcased nine functional food and beverage concepts aimed at the e-sports and gaming segment at the IFT FIRST 2026 expo, including an e-sports energy drink, high-protein gummies, and nutrition bars.

- An immersive virtual reality football experience at the event highlighted how IMCD helps brands connect with performance-focused consumers through both product innovation and new engagement formats.

- We’ll now examine how IMCD’s push into e-sports-oriented functional nutrition could influence its broader investment narrative and growth drivers.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

IMCD Investment Narrative Recap

To own IMCD, you have to believe in its asset light specialty distribution model and its ability to deepen exposure to resilient end markets like food, pharma and personal care while managing cost inflation, FX headwinds and acquisition risk. The gaming focused concepts at IFT FIRST 2026 support the innovation and outsourcing catalyst, but do not materially change the near term picture where modest organic growth and pressure on conversion margins remain key watchpoints.

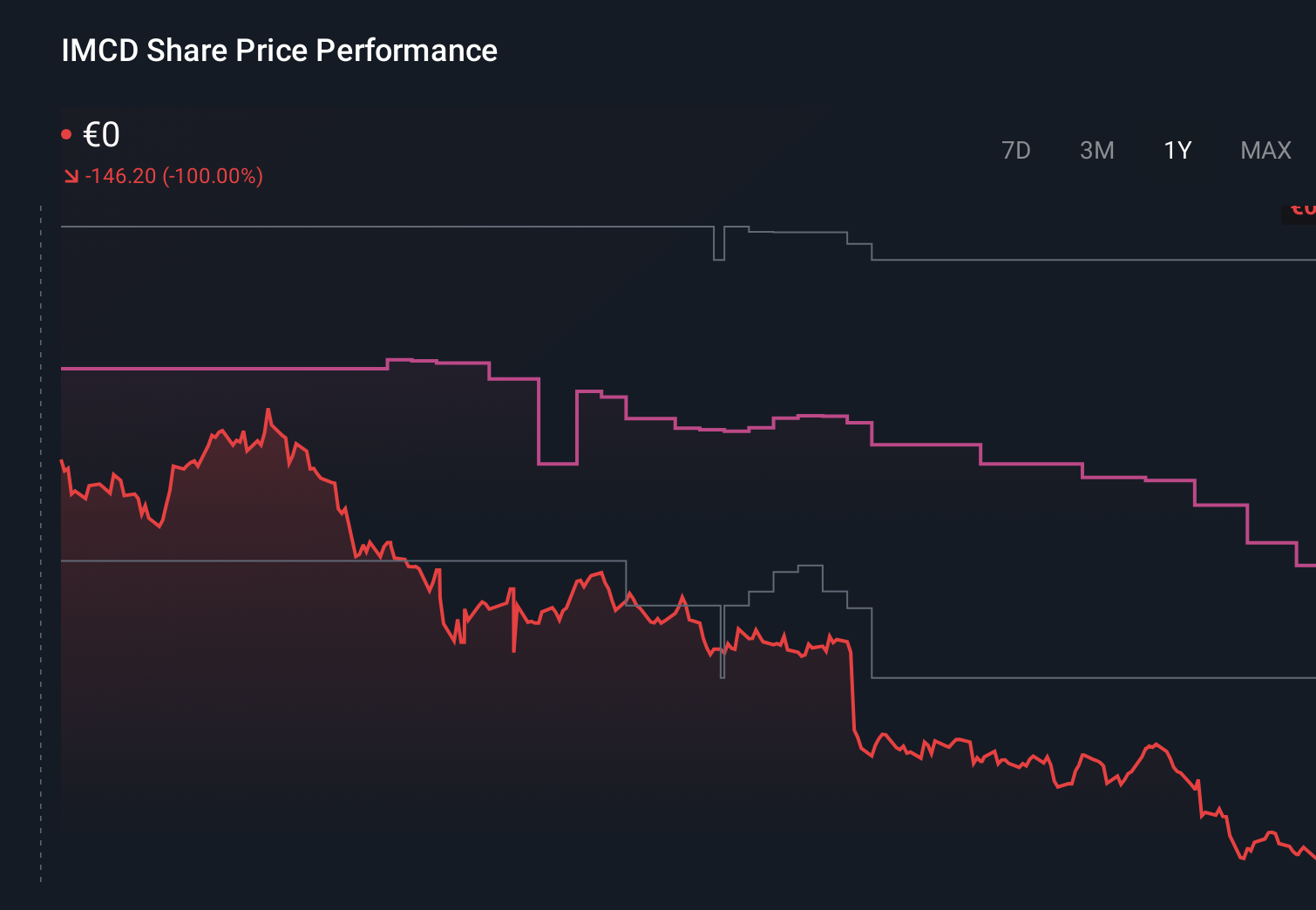

In this context, the recent approval of a reduced EUR 1.81 per share cash dividend for 2025 is more directly relevant. It underlines how management is balancing shareholder returns against softer earnings, higher working capital needs and acquisition related spending. For investors watching IMCD’s expansion into niches such as e sports nutrition, the lower payout is a reminder that capital allocation discipline and margin preservation still anchor the near term equity story.

Yet beneath the appeal of new gamer focused concepts, investors should be aware of...

Read the full narrative on IMCD (it's free!)

IMCD's narrative projects €5.6 billion revenue and €300.2 million earnings by 2029. This requires 5.2% yearly revenue growth and about a €82.6 million earnings increase from €217.6 million today.

Uncover how IMCD's forecasts yield a €112.50 fair value, a 32% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming IMCD could lift revenue to about €6.3 billion and earnings to roughly €360 million, and they view digital tools and complex regulatory support as powerful margin catalysts. The new e sports concepts might support that story or challenge it, and your view on that will shape whether you see IMCD as closer to that bullish case or the more cautious consensus.

Explore 5 other fair value estimates on IMCD - why the stock might be worth 10% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your IMCD research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free IMCD research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate IMCD's overall financial health at a glance.

Contemplating Other Strategies?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com