Is Mastercard (MA) Undervalued On Its New AI Payments Push?

Mastercard (MA) is pushing deeper into AI driven payments with its Agent Pay for Machines (AP4M) platform, which connects traditional card networks to stablecoin settlement on public blockchains for autonomous software transactions.

See our latest analysis for Mastercard.

Against this backdrop of AI driven initiatives, Mastercard’s share price has been mixed, with a 30 day share price return of 7.70% contrasting with a year to date share price decline of 6.46%, while 5 year total shareholder return of 40.15% points to stronger longer term compounding.

If you are looking beyond Mastercard’s AI push, this could be a useful moment to scan for other payment and fintech players tied to artificial intelligence through the 63 profitable AI stocks that aren't just burning cash

The recent rebound in Mastercard after a weaker year to date highlights a key tension: are investors reassessing the underlying $462.3b business, or simply rotating back into a high quality compounder following a sentiment driven pullback that the current valuation must reflect?

Most Popular Narrative: 29.8% Undervalued

On the numbers used in the most followed narrative, Mastercard’s fair value of $750 sits well above the last close at $526.74. That puts that user view under a spotlight for readers weighing the recent AI headlines against longer term fundamentals.

What it offers instead: a business that compounds safely, a payout growing at double-digit rates from a tiny base, and a price that does not currently reflect either of those things. Setups like that do not come around often, and the current pullback looks more like an entry point than a warning sign.

Curious what sits behind that $750 figure and the near 30% gap, according to Investingwilly. The narrative focuses on steady revenue expansion, thick margins and a future earnings multiple that many investors usually associate with different sectors, not just card networks. Want to see how those ingredients are stitched together into one fair value story.

Result: Fair Value of $750 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Mastercard’s story can still break if regulators hit fees harder than expected or if stablecoin based rails gain traction faster than its own platforms adapt.

Find out about the key risks to this Mastercard narrative.

Another View On Mastercard’s Valuation

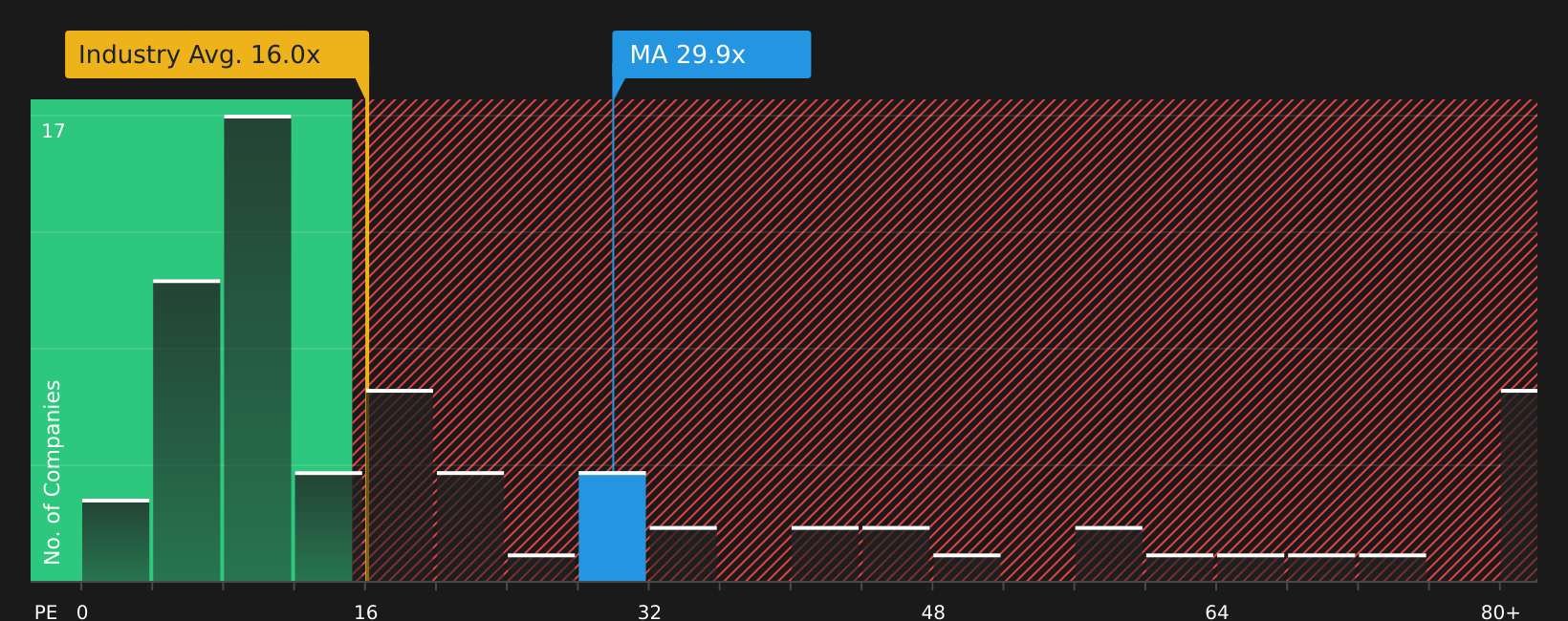

While the user narrative leans on a fair value of $750, the current P/E of 29.9x tells a different story. It sits well above both the US Diversified Financial industry at 16x and the peer average at 26x, as well as a fair ratio of 20.9x that the market could move towards. For investors, that gap points to valuation risk rather than a clear discount, so which signal do you trust more right now?

To see how this richer multiple compares in context, including peers and the fair ratio, take a closer look at the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment on Mastercard clearly split between opportunity and risk, it may be useful to move quickly to review the balance of 4 key rewards and 2 important warning signs

Looking for more investment ideas beyond Mastercard?

If Mastercard has you thinking harder about where to put your next dollar, this is a smart moment to broaden your watchlist with fresh opportunities.

- Target potential mispriced opportunities before the crowd by scanning the 44 high quality undervalued stocks.

- Build a steadier income stream by reviewing companies in the 9 dividend fortresses.

- Prioritise resilience by focusing on companies highlighted in the 76 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com